Hi,

With great caution I am trying to take a stab at this for two eminent reasons.

a. The nudging came from someone whom I hold in high esteem for two qualities (hard and detailed work, eloquence). No flattery by the way.

b. Equally importantly, AP has proved to be best workhorse in my PF. As a result over a period this has become significant % of my total PF. Gotta behave circumspect.

@Donald – Always helps to challenge the trap called complacency. Glad that you still want to short of play devils advocate here.

In the true spirit of ensuring a productive outcome from this exercise (looking at some of the ration/metric to see how much steam is left), I am trying to firstly establish that all of us are looking at the numbers from same and correct vantage point.

So, here I go………at some places I am observing some ‘significant difference’ between your quoted numbers and what I have observed from Morningstar. I am concluding that you have taken the standalone numbers from screener, whereas Morningstar has consolidated numbers. Having said that, difference between the two should not be this wide (since consolidated is ~only 10% higher to standalone topline for FY’16).

Apologies the format is not perfect, posting from mobile and facing technical issues. but dont want to miss the important points for semantics hence just “jugaad-ed it”.

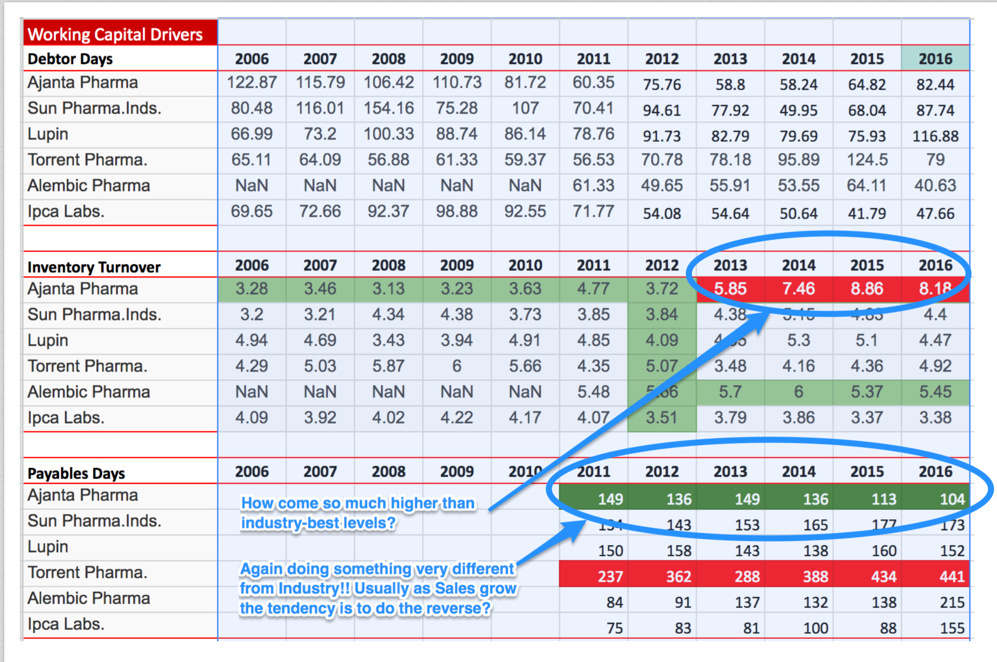

Somehow, it appears to me that Morningstar data is closer to reality. Cross verified the RONW and Inventory turnover numbers from the Q1FY17 investor presentation and both set of numbers are stacking up pretty smugly.

Now, to answer the direct question, will the investment be equally rewarding going forward?

To answer this, for a moment I am taking the liberty to consider Morningstar as my reference data:

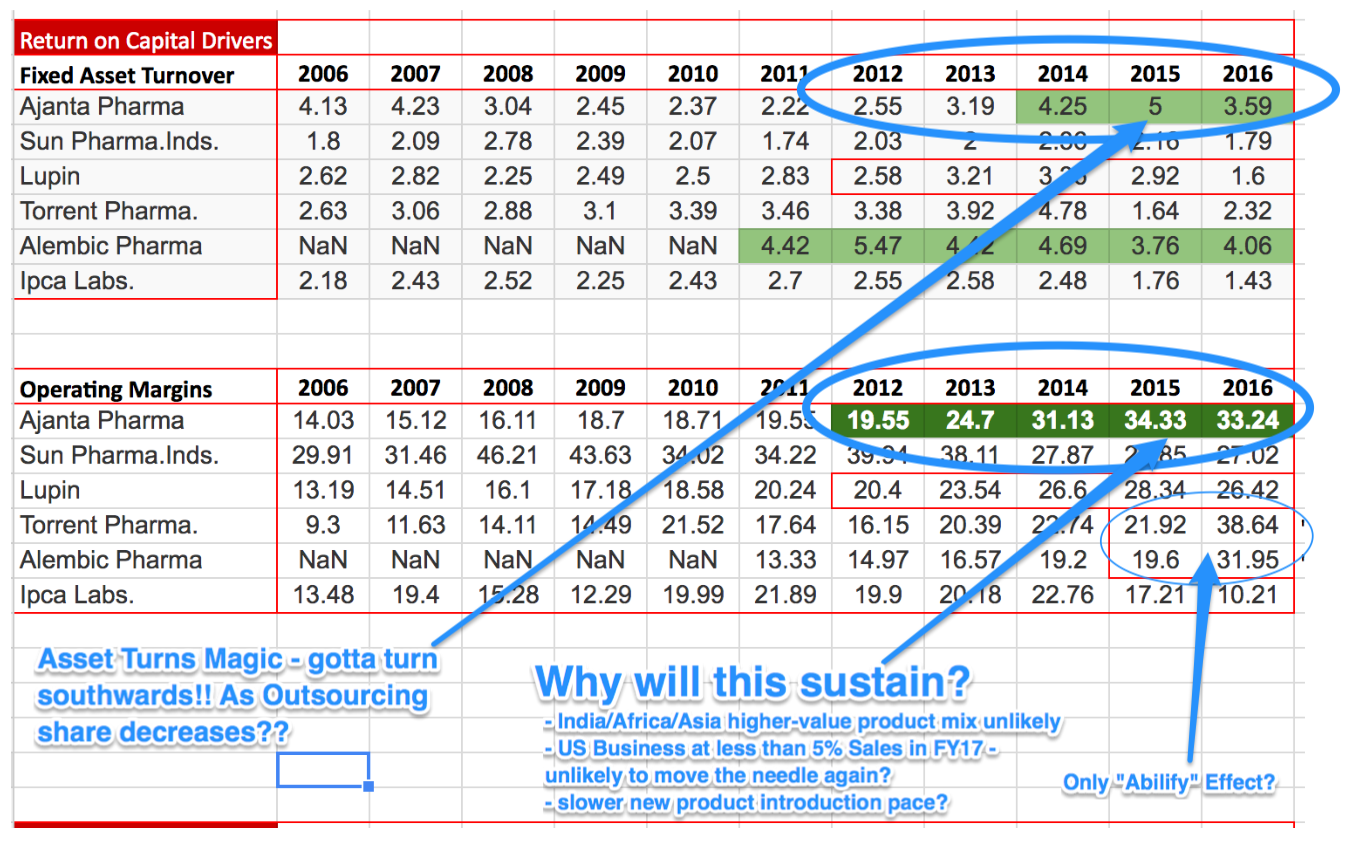

Bottom line: Looking closely at the numbers, AP has improved the margins at all levels consistently till this year. Gross margin from 63% to 73% between FY12-16. What does that means? To me, company ‘still has pricing power by virtue of first-to-market strategy’ Equally important, AP has gained significant operational efficiency across each of the possible steps (operating margin 14% to 32% and Net profit 12% to 24% between 2012 to 2016). By extension ROA/ROE/ROIC each followed a northward journey.

Now, at this juncture, and in context of Morningstar data, I tend to believe that any further squeezing/efficiency may be little difficult since they are mostly far superior to peers and industry best in some cases.

Top Line: On the other hand, FY’16 top line growth of 16.68% is on the lower side by AP benchmark. Even FY’15 was nowhere close to peak ~35%ish growth. Historical top line growth trend:

FY16: 16.68%

FY15: 22.53%

FY14: 29.81%

FY13: 37.41%

FY12: 34.17%

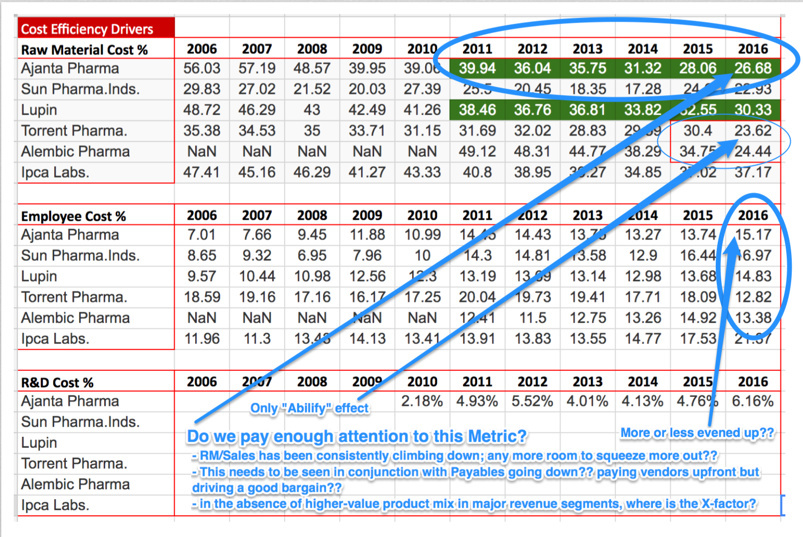

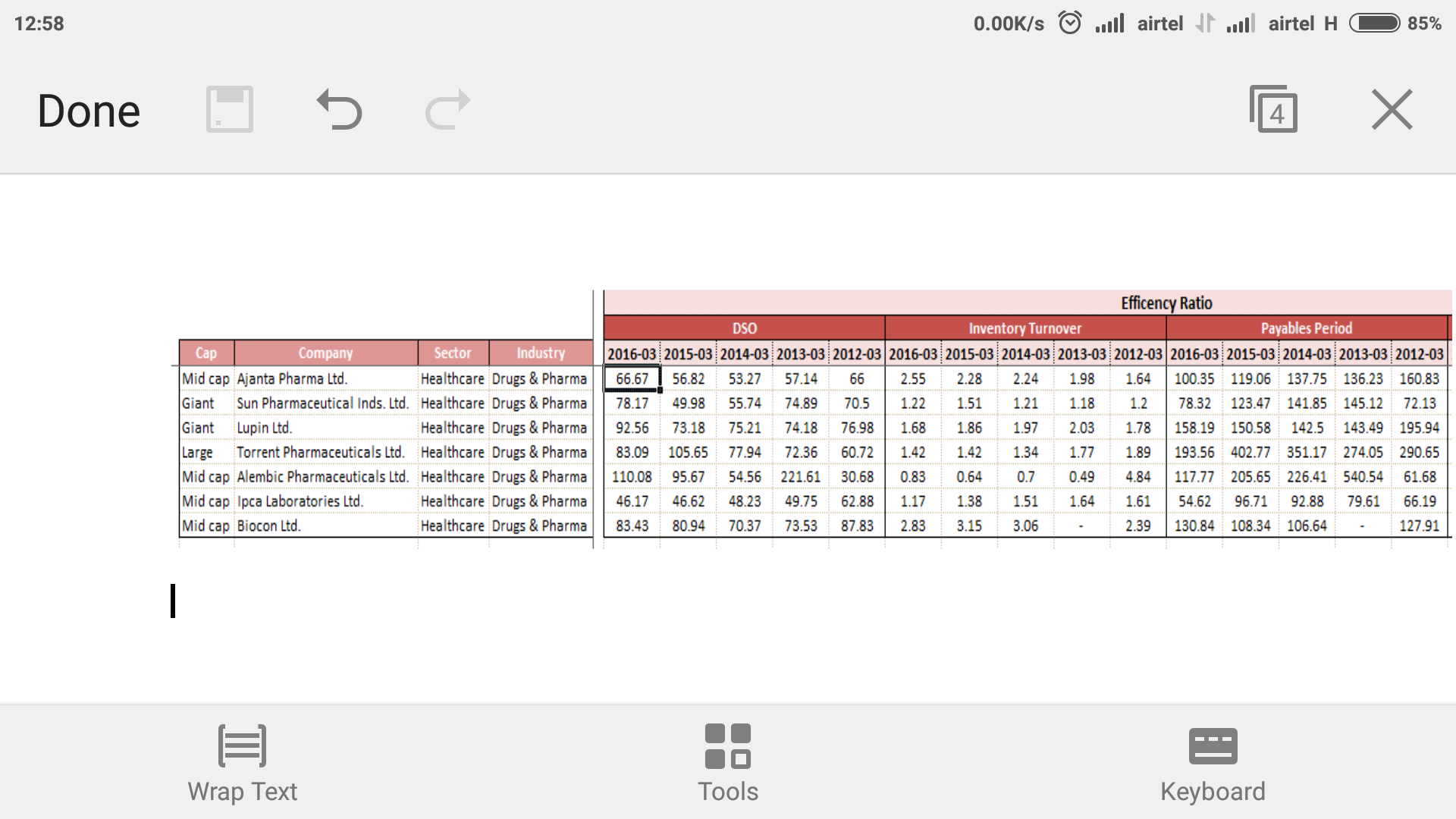

As expected, that’s why we have sign of stress on DSO, assets turn over, inventory turn over etc.

Coming to your well intentional questions (food for thought), after connecting the dots, IMHO for AP the question to be worked upon further is related to avenues for top line growth more than improving/sustaining the efficiency/margins.

Specifically on top line growth, Ajanta’s USP has always been:

a) Introducing first-to-market (approx. 70% of 190 branded formulation so far, if I recall correctly).

b) Targeted marketing effort (country/geography specific go to market approach).

What I have observed is that AP is ‘slightly’ moving away from its forte…i.e. the first-to-launch margin rich new formulations in the underdeveloped/developed markets (read Africa, Asia). Somewhere seems that company is now aspiring highly regulated, competition intensive USA market via ANDA route. Upcoming Dahej facility (coming to steam in FY17), already filed 18 odd ANDAs and stated aspiration to file ~8 ANDA per year for next 3 years etc. all are indication of STRETCHED FOUCS towards US market.

Though by management commentary and even by notes from AR, seems that management is still intends to play by strength (first to market products, below radar marketing, underdeveloped markets etc). However, will be interesting to see how much successful they will be in the fine balancing act.

Attached is a template that I use to evaluate any prospect (standalone and within sectors) thanks to Pat Dorsey.

My investment hypothesis for Ajanta is entirely based on the success/failure in getting top line traction. Do let me know if I am missing something in concluding that issue worth evaluating is top line growth NOT bottom line incremental improvement.(I.e raw material cost℅,employee cost℅ etc.)

MS Consolidation Sheet_Pharma.xlsx (25.6 KB)

Disc:

- AP is significant (~18%) of my PF. Averaged-up periodically since first position. No transaction in last 1.5 years.

- Still learning