Ah, that image is a post by one of the twitter handle. The content appears to be behind the paywall type. Thus would refrain naming the handle (have high regard for his/her tweets). Cheers.

Ajanta gets approval for 5mg/10mg gNamenda (Memantine Hydrochloride)

Source: http://www.accessdata.fda.gov/scripts/cder/ob/docs/obdetail.cfm?Appl_No=206528&TABLE1=OB_Rx

The patent of Namenda (Memantine Hydrochloride), owned by Forest Lab (wholly-owned subsidiary of Actavis), expired in April 2015. According to IMS Health, the Namenda tablets brand had U.S. sales of approximately USD 1.4 billion MAT for the TTM ending in May 2015.

Forest, Teva, Mylan, Sun, Lupin, Auro, DRL, Wockhardt, Torrent, Alembic, Ajanta, Jubilant, Amneal, MacLeods, Puracap, Unichem and Upsher have gNamenda approval.

6 Likes

Ajanta Pharma Announces the Launch of Montelukast IR Tablets and Montelukast Chewable Tablets. This launch extends the breadth of the Montelukast offerings from Ajanta Pharma into three dosage forms (Immediate-Release Tablets, Chewable Tablets, and Oral Granules [announcement on 16th Nov]).

1 Like

Guys, Ajanta pharma has fallen from a high of 1720 to 1260 .

This is not a normal correction.

Is there something that we are missing out there.

I think its the macros thats pulling the scrip down and it makes us to go shopping on this discount

spree

Over the past couple of years (even more in some cases) pharma companies have outperformed a strong market. If you notice it is not just Ajanta, but a whole host of names from the sector that have corrected significantly from their peaks.

This has more to do with the fact that FIIs/ funds/ HNIs are looking to take some of their profits off the table, which is but natural. These investors as others would have made significant returns over these past couple of years in a lot of these names and are now looking to lock in some of their gains -

Why now? In my opinion its because a lot of these names have gone from being undervalued to being fairly and in some cases over valued. This would mean that they may not be able to provide out-sized returns at least in the short to medium term.

If as an investor you have a long term view of the business/ industry I don’t think these corrections are anything to worry about. Whether or not this provides a buying opportunity though is very stock specific and is dependent on your understanding of the future potential of the business.

Personally, I would not blindly go out and buy the names that are falling - we tend to do that more out of a price anchoring bias.

Buy if you truly understand the business and its growth path and believe that the current price does not completely reflect current or future value.

Disc: Pharma companies > 60% of my PF

6 Likes

I think Ajanta unlike Alembic or Torrent is a fairly predictable business.

Management has indicated that co would grow between 15-20% for fy 16 and going by half yearly figures it seems on track. It could have eps figures between 42-46 by my estimates. (It has done 20.89 per share for half year ended sep 2015 on consolidated basis as per their results available on bse.)

Also looking at the balance sheet statement given with q2 results co is net cash. (no debt)

The good news could be recent spate of approvals in namenda, and monteleukast tablets. It earlier also had a couple of approvals (I think risperidone was there earlier). Now over next year or two I expect the US business to become the growth engine once the expanded capacities come into place and some more USFDA approvals come through. Till that time growth may remain in the 20% or thereabouts range.

What I like about Ajanta is its clean balance sheet, calibrated growth plans and management smarts.

I think as a great business it has proven itself over past few years.

disc: Had exited above 1600 plus (no problems with company as such but it seemed overvalued) levels to convert into torrent pharma and waiting to get into ajanta again. Currently no position.

23 Likes

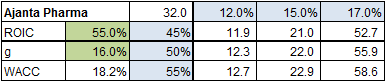

Using the formula: (1 - g/ROCE)/(WACC - g) from Valuation by McKinsey (page 66), I tried to find out a reasonable PE for Ajanta. Results are displayed in table below. Seems a lot depends on long term growth rate which the market is currently implying at 16% (PE of 32)

WACC picked up from Ajanta Pharma WACC % | NSE:AJANTPHARM - GuruFocus.com

Disclosure: Invested. Forms a significant part of portfolio

2 Likes

Hi Hitesh,

that is interesting. i always wonder how one manages to do that. for such high quality, secular growth companies, how do you decide when to get back in?. because you tend to wait for a better reentry price. moreover, if one has a fairly large position, it will be very difficult. (not for executing the transaction. but to renter with the same value or sitting on cash)

for lesser mortals like us, would you recommend stay invested and bear the time plus price correction for a while?

can you please share your views? thanks

disc: hold both ajantha and torrent

3 Likes

gautham1,

I have been tracking ajanta now for a long time and of late had been feeling that while the company’s growth esp the topline was likely to be lower than the earlier heady days mainly bcos of higher base effect, the valuations accorded to the company when it went up to 1600 plus levels were very high.

As I said before ajanta is a predictable business where one can put in a figure which one is comfortable with and then come out with expected figures. Though this might not be too accurate one can broadly get a ball park estimate.

I did not expect ajanta to grow its earnings more than 35% for fy 16 and putting that figure into context, I felt it was difficult for ajanta to sustain at above 1600 levels. And at the same time Torrent Pharma had the abilify opportunity and stock price was not going anywhere (still is going nowhere  ) and I felt that there was a better opportunity in torrent. I follow a concentrated approach and so it had to be an allout switch.

) and I felt that there was a better opportunity in torrent. I follow a concentrated approach and so it had to be an allout switch.

Till now the fundamentals of both companies have played out as I had expected and I remain hopeful in torrent. Till now I have been positively surprised by its results and the kind of juice they have squeezed out of their opportunity.

Even Peter Lynch in his book One Up mentions about some stocks taking time for their earnings to catch up. Ajanta seems to be doing exactly that.

Sitting on cash is still difficult for me.

Regarding bearing the pain and sitting tight with ajanta, let me tell you that at the current prices I am inclined to re enter ajanta but since I dont find a favorable switch, I am still in wait mode.

But if one reads Phil Fisher, he used to remain invested for decades and if one has his kind of mindset I dont see any harm in sticking around with ajanta.

Its always a tricky call of when to switch and what to switch into and you often get things right and sometimes wrong. If it doesnt cause too much regret and heartburn, one can try these switches. For those who keep pinching themselves when things dont work out, its better to buy and remain invested and sit tight even in obvious situations of overvaluations.

72 Likes

Hiteshbhai,

What an articulation! The way you have laid out why & how of switching from Ajanta to Torrent (which we may extend to many such opportunities), without an iota of exaggeration, I feel anybody else on VP could not have articulted in such a simple yet effective manner… Thanks for sharing your thought process for people like us who continue to learn from you time and again

8 Likes

thanks a ton hitesh. that was very well explained. i really appreciate it.

1 Like

Each word of HiteshBhai is worth gold. A beacon light for lesser mortals like us.

1 Like

I still remember some moons ago when you had switched from ajanta to unichem.

admire how you can shift through the noise, clarity of thought,quick reflexes, and unemotional investing style. Hat doff to you sir.

admire how you can shift through the noise, clarity of thought,quick reflexes, and unemotional investing style. Hat doff to you sir.

1 Like

Thanks hiteshbhai. Too good.

1 Like

No wonder we are in love with one of the smartest minds (not just in VP) that we come across in our investing journey.

I would request every passionate learner to visit the Man in Baroda :). He is a great host by the way. I still remember I sought out Hitesh in one of my journey to Mumbai in 2010 and asked to meet him in Baroda the next day. His house was getting renovated …and he still gave me undivided attention almost the whole day, among interruptions.

2 things stand out for us when we think of Hitesh in Team VP.

- Ability to cut through the clutter - very sharp - and he keeps sharpening the saw

We used to marvel at his ability to summarise in 2 minutes Pros and Cons and a good enough entry price band for the business - after say finishing off a Management Q&A of 2 hours

We used to do this with everyone asking everyone to take 2 mins to summarise. Almost all of us would take a week before things actually sunk in for us - and obviously our 2 min summaries wouldn’t be sharp, nor would it be able to present pros and cons in that level of simplicity, and 80%+ complete, just after a Marathon Q&A

2.Unemotional Investing (as Juzer has so aptly mentioned)

I haven’t seen a more ruthless and dispassionate examiner of facts/merits of a candidate in your portfolio (after you have held for a few years). Many of us can be really ruthless about a new prospect, but miss the mark when it comes to invested candidates - easy to get complacent - not this guy!

I have admired this trait much more and have tried to emulate as best as I could - still miles to go.

There is a saying - if you admire some quality in someone greatly, you will slowly start imbibing those qualities - it’s an universal thing - quoted in Bible and our Vedic scriptures as well.

CAUTION POINT: About switching. unless you can sleep peacefully with hits n misses after switching (as Hitesh mentions), do not try to emulate this aspect. Know yourself well - know what suits you. If we are not that sharp (which holds true for most of us) it’s far more easier holding on to a good story where we know the business well, hold management in great esteem, and know the business has a very decent competitive advantage period in front. I subscribe to the view more money is made more easily (read lazily) by holding on to great stories (thru swings of over and undervaluation) than by switching out trying to second guess how far say an Ajanta can go, or Astral or Mayur, or even Avanti, or Atul Auto, or PI industries, or many others can go.

if you belong to this camp, then a very effective way to resist any such temptation is to ensure some steady healthy cashflows coming in on a regular basis (then you can easily resist the temptation to do an all-out-switch and can still invest meaningfully in both). For salaried folks who are financially well-managed, this can work easily. For full-time folks like me, you can work hard at establishing a steady consulting cash flow.

35 Likes

Hitesh Ji

Each and every response from you is highly educative.

Thanks a lot

1 Like

Nice way to describe someone who has the great great ability to pick temporary top in his stocks. Wish to meet you all one day soon.

1 Like

very interesting views sir. goes on to show your understanding of nature of markets & more importantly your faith in it.

in cricket lingo, this is like seeing the new ball off or waiting for the slog overs knowing that theres definitely going to be one later

on the flip side, can you throw some ideas on how you manage thinking/emotion when a story doesnt play out as expected or takes too long?

say for ex, switching over to torrent pharma and torrent pharma not performing on expectations for say 6months. how do you assess the scenario then?

PS: there’s no like button for the photos probably, must add that the new photo looks perfect

Thanks for all the applause. I dont know how much I deserve it.

If there is a case where things dont work out as expected especially on the front of the company reporting numbers as expected or where some other expected triggers dont play out then after the stipulated time, it makes sense to accept that we made a mistake in our investment thesis and exit the position and move on without any recriminations.

And it has often happened that after waiting a long time for the tide to turn for the company and still no returns, once I have exited a company, the things start to improve and even stock price starts to rise. But one has to take it as a part of the game and accept the misses with the hits. As long as the hits provide outsized returns as compared to the quantum of losses in the misses its okay

And one has always to consider the portfolio approach. There will always be a couple of stocks in a portfolio of 8-12 stocks which will not move along expected lines sometimes inspite of the expected fundamentals results coming through, But if the whole PF is performing well then that should be okay. Many a times some investors get caught up with a particular stock in PF and keep worrying about it. So there the PF approach should be helpful.

23 Likes