Was looking at results. Pretty good growth in topline and decent profitability…perhaps finally the outcome of the capex done over last couple of years.

Given the pref allotment by promoters at higher price…anyone has insights on same?

Was looking at results. Pretty good growth in topline and decent profitability…perhaps finally the outcome of the capex done over last couple of years.

Given the pref allotment by promoters at higher price…anyone has insights on same?

not sure what kind of insights you mean ? The company seems to be on the right path …first it successfully came out of BIFR and now growing without any debt… having met the management, my first impression was that they want to make it big but without taking too much risk (given the lost decade due to financial difficulties). The impression which was given to me is that there’s a lot of scope on OPM expansion going forward.

i meant as they were raising money…there might have been details around capex and expansion plans going forward?

Not much details were given as mentioned here. The objects of issue simply said its for capex…i think looking at the before and after balance sheet they roughly doubled their capacity.

@j2eeprofession_ and @ayushmit

Would you be able to tell why margins have been contracting.

I see Gross and Net Profit Margins were higher in 2017 (more than 10% odd) but in last two years they have been at 5-6% odd…

Is it due to crude?

I think the issue is the other income part in the last 2 quarters. If this other income is part of normal operations (maybe recognized as other income due to forex hedging etc) then the margins are inline with before. From what I could understand - a large part of turnover growth came from couple of products which were high in value but low on margins. But the company has been increasing the product portfolio.

Lets see if they can grow from here with better margins.

some part of OI is duty drawback and other export incentives which earlier got reported along with sales

Excellent result posted by Aimco.

Agree… amazing numbrrs

AIMCO PESTCIDES AR 18-19 NOTES

Revenue from operations at 197 cr vs 111 cr (77 % yoy growth)

EBITDA at 13.4 cr vs 9.20 cr ( 45 % yoy growth)

PAT at 7.71 cr vs 4.98 cr ( 56 % yoy growth)

Aimco Pesticides Limited is the leader in Chlorpyrifos, Triclopyr, Bifenthrin & its formulations.

Company will continue to add new molecules to its portfolio to further consolidate its position in the industry

Will upgrade the manufacturing technology and facilities as well as add new molecules in its product portfolio.

US – China trade war will offer promising prospects to company’s customer base in USA.

Dividend recommened of Rs.1.5

Promoter holding have risen over the year from 51.14 % to 51.32 %

Money spent on R&D – 2.07 cr , 1.05 % of total revenue .

R & D is for improving production efficiency , working on new molecules , commercializing new molecules

Contract R & D & Toll manufacturing for foreign & large local companies, new export market registrations are actively pursued and inventing cost efficient processes

160 cr was export revenue ( 80 % of total)

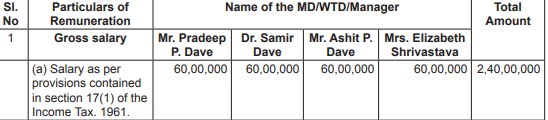

Remuneration for Key Management personnel is very high -

Total salary of KMP – 2.4 cr .( 21.6 % of PBT)

Future outlook by the company is very positive

Company is confident about upgrading its manufacturing facilities, investing in overseas product registrations, adding new molecules to its product portfolio.

Apart from loyal customer base, the Company is enjoying since last several years now, many more new domestic as well as overseas customers are added to the portfolio of the Company during the year and same is expecting to increase in near future due to Company’s commitment of supplying high quality product and competitive price.

The Company’s endeavor is to widen its presence in multiple segments continuously and to increase customer base to reduce the dependence on any specific customer / market

The company aims to be ZERO Liquid effluent discharge status in five years.

India is 4 th largest agrochemical manufacturer after USA, Japan and China.

Exports are expected to grow at a rate of 8.6 percent to reach $4.2 billion by 2025

China has seen significant reduction In exports in last couple of years.

This is owing to the implementation of stringent environmental norms by the Chinese government, crackdown on the polluting chemical industry and impending tariffs from US on Chinese products.

There has been a large scale shutdown of plants which are causing pollution, relocation of chemical plants to far off industrial areas as well as compulsory effluent treatment plants for every chemical plant

India is being seen as a manufacturing hub of agrochemicals , exciting opportunity lies ahead for companies in this sector.

The salaries of KMP is proposed to double from existing one in coming board meeting

is anyone planning to attend the AGM?

have they made any announcement of the same?

am not able to find it.

One thing u missed in the write-up is that promoters have pledged 50% of their holding …when I asked the CS why they pledged he said it’s for working capital …I’m confused as to why such huge working capital is required …can somebody enlighten me ? If I’m correct it’s about 35-40 crores …will we see exponential rise of revenues due to this ?

that wont come in the AR as the pledge was created after MAR 19.

Ok but since we are discussing the company and its prospects this would be important thing to be discussed as well

i wish somebody visiting the AGM asks them about this pledge… this is the only red flag in otherwise a wonderful story…

Agm is on Sept 9th as per mc

Can some one help me out here …the promoters have pledged their shares when the price was around 130 bucks …but they have written in the disclosure that they have gotten 13 crores for it …isn’t 13 crores a small amount to be raised at that price ?