There is an article in BS on how the housing finance players share the market pie and how affordable housing could change this.

Another one from Bloomberg on affordable housing-

Main points -

- Demand outstrips supply

- Affordable housing still not lucrative for builders despite government’s policy changes and infra status.

- Interest subsidy benefit has been extended for another 15 months. Though, what this is doing is actually making investors come forward and exploit this scheme by loan prepayments. Loan prepayment by such buyers soon after availing interest subvention is making banks apprehensive about lending for affordable housing as foreclosures amount to lower interest earnings.

- Mahindra Lifespaces is yet to sign a memorandum of understanding with a state government for an affordable housing project.

Repco AR has clearly mentioned that Affordable housing is not picking up as there is not enough supply and also there are state specific issues

Purvankara believes that the affordable and value for money housing segment is expected to see improved sales across our markets

What do you think about playing affordable housing theme with Reliance Home Finance? The valuation seems very attractive at the moment. But the price seems to have not caught up yet. Maybe because it’s just been listed.

PE: 24

P/B: 2.1

GNPA/NNPA: 0.89 / 0.5

Tripled sales and net profit in last 3 years. Guidance of same in the next 3 to 5 years.

Low base and big opportunity size. Rs13,000cr AUM and Market cap of Rs4,200cr.

Superior NIM: 3.9% comparable to Indiabulls Housing Finance.

Good promoters: Reliance Capital owns 51% which could help in debt raising at low interest rates

20% portfolio in Affordable Housing.

About 50% portfolio in risky LAP and construction finance and hence superior margins.

Does this stock have good growth potential or am I missing something here?

Disclosure: Invested

How did you come up with PE of 24. It has one time exceptional items last year/quarters. Adjusting for those PE is around 40, which is not cheap. But it is cheap on P/B, the reason for this contrast is their very high cost/income ratio at 40%. Can fin home is at 15%!

And what you called good promoter is the real curse for the stock. No one is comfortable giving loans to Anil Ambani group companies.

Can you please elaborate further on one time adjustment making the PE 40. I am basing my views on very little publicly available information.

True, some Group companies are facing debt issues. But my understanding is Reliance Capital is relatively ring fenced from other Anil Ambani holding and has no debt issues.

Just checked the financials now. Absolutely no movement in PBT even as sales increased 40%. Only change was a Tax benefit of Rs30Cr which doubled PAT over last year. Shocked! Sold at a loss all my holding bought yesterday!

Hi Susindar,

Can you please provide following information if you are aware -

- How much of RHF loan book is in the affordable housing (AH) segment?

- What are the geographies in which they have AH loan book?

- Any other information like - AH loan book growth, AH projects are from private developers or state housing boards etc.?

Thanks,

Rupesh

It will be good if we can discuss the relevant points for Reliance Home Finance on the specific thread. If the thread is not initiated then one can open a new thread. Just a suggestion.

Sorry mate. I do not have those info. All I know is that they have an affordable housing portfolio of around 20%.

I thought their PAT was Rs170 cr last year and had an improvement of 100% over previous year. But the fact is the profit before tax did not change over last year even as the top line grew by 40%. Only reason PAT increased was because of a tax benefit of Rs35cr which doubled PAT over previous year. This is even as all other housing finance companies showed excellent growth. Imagine what would their performance be when competition is so high this year. I do not think it is a worthy stock at this level. May be one can look at this at Rs50-55.

To begin with my understanding of the segment is limited and is currently work in progress. If we look at the entire affordable housing landscape there are a few facts that one needs to look into:

a) Affordable housing or Housing for All or PMAY (PM Awas Yojana) is a Central Govt initiative which aims to provide a pucca house for everyone by 2022. The scheme is both for urban (PMAYUrban) and rural areas (PMAYRural).

b) There are multiple schemes which are currently being made a part of broader HFA. Some of these schemes are CLSS (Credit Linked Subsidy Scheme), PPP Model, Slum development, MukhyaMantri Awas Yojana in Combination with PMAY etc.

An example of Mukhyamtri Grah Yojana in Surat

https://www.suratmunicipal.gov.in/Departments/MukhyamantriGruhYojana

c) Under PMAY (U) demand survey is conducted by concerned ULBs, offline and online, free of cost. Online registration can also be made by eligible beneficiaries themselves through the Ministry’s website. These details can be found here:

http://pmaymis.gov.in/Open/Print_Application_By_applicationNo.aspx.

Now coming to the general pattern of how the scheme is unfolding overall in Urban areas:

Model 1:

a) Land is being provided by the Local Body.

b) There is a subsidy provided by GoI of 1 L and State Govt. of 1L.

c) Construction contracts are laid out.

An example is the recent construction by L&T in Surat.

Model 2: Land owned privately

a) The builder gets TDR rights over the prescribed FSI for his land.

b) There is a subsidy provided by GoI of 1 L and State Govt. of 1L.

Model 3: Slum redevelopment

Nila Infra did a few of Model 2 and Model 3 above.

In none of the above CLSS is applicable.

Model 4: CLSS

Now if one goes through the proposed housing projects and surveys done by the Govt. the total demand comes to around 2/3 crore houses and 90% of these being under the 10L bracket. This data can be accessed from the Ministry of Housing & Urban Affairs

http://mhupa.gov.in/User_Panel/UserView.aspx?TypeID=1570

The website has all details about demand/implementation status of projects in each state and each project. For example:

http://mhupa.gov.in/writereaddata/AndhraPradeshcsmc024.pdf

http://mhupa.gov.in/writereaddata/Maharashtra_csmc25.pdf

http://mhupa.gov.in/writereaddata/Gujarat_csmc25.pdf

The following links gives details for fund releases for various states:

http://mhupa.gov.in/User_Panel/SanctionOrdersView.aspx?TypeID=1486

And the following link gives details of progress in each state until August

http://mhupa.gov.in/writereaddata/PMAY_Progress_as_on_31072017.pdf

The key points to ponder:

a) The opportunity size is roughly 2/3 cr * 3/4 Lac = 6/12 L Cr

b) What role if any is there for the current set of builders since the demand creation is happening bottoms up by the Local Bodies. Is there any difference between an EPC Player (Construction firm) and a builder?

c) What will be the impact of CLSS?

d) Will it further push down the demand for homes from builders who are currently making houses in the range of 20L /50 L since a lot of new house owners will move towards the above schemes?

e) And finally who will be the key beneficiaries?

This is a work in progress and will love feedback and clarity from the forum members.

It may not push down the demand 4 affordable houses of builders as clss can be claimed on those houses too.don’t know whether there will be any gst impact difference between epc and builders.Builders who are having adequate land in metros and municipal areas would find it easy to monetise the land.but the major beneficiaries will be companies who are into building materials.

My two cents- I was going through AnantRaj AR and it could be a play on expansion by co.s esp. when it has a landbank around NCR. The company is also earns through renting which i feel is better than selling outright. Just a novice, would love to learn from seniors.

Disc. Invested.

Along with cement and steel, sand demand will pick up due to AH. I have noticed that few sites have to delay construction due to shortage of sand. Is there any listed player which supply sand?

A friend was meeting an Infrastructure player looking to focus on Tier 2 and Tier 3 Cities. So we hurriedly put together an initial query set on the whole Affordable Housing Opportunity.

Initial Queries on Affordable Housing Industry Opportunity - India

While the PMAY (Urban and Rural) Schemes (upto 60m2) point to sub 20Lakh segment mostly, there is this whole segment of 20-50 Lakh that organised Developers indicate as working on Affordable Housing. We have seen mixed projects – high-end + AH in existing private land being announced by leading developers. There exists a policy guideline dated Sep 2017 – PPP Models for Affordable Housing from MOUD that points to several models for incentivising private participation.

-

What is the current scope of participation by private developers in AH Opportunity? Phase 1 is govt-funded Urban local body/slum redevelopement only and that scope is only open to Construction companies. And that real participation by private entities will kick off only in Phase 2?

-

Or is this the real picture of private participation in AH Opportunity?

-

Housing for All – PMAY ( Urban & Rural). Rural PMAY has reportedly constructed 2.5 Mn Homes already in 2017 whereas PMAY Urban has been a slow starter, with pace starting to pick up across states now. How do you view this Social-Housing opportunity segment within the total Affordable Housing space?

-

How is money going to be made in the Affordable Housing Industry? Can we make a profit pool like above - Builders, Construction companies, Ancillary players (cement, steel TMT, tiles, roofs, pre-fabs, plywood, electrical cables & fittings, pipes, sanitaryware, adhesives & construction chemicals companies), Housing Finance.

-

One perspective says, if it has to be that big a Rs. 6 Trillion opportunity in the next 5 years – first houses need to be build at that volumes scale. Only if houses get built at that scale, will ancillaries make money, or Housing financiers be able to lend (potential/latent demand exists). So who will lead the charge here – the most efficient builders who have the necessary scale to build on (as it is a low-margin, hgh volume game)?

-

Is it a fair assessment that the most incentivised activity in above profit pool is the Builders – tax exemption (20% MAT for 5 years) and access to cheaper credit because of infrastructure status to Industry? The others like ancillary players (even Housing Finance not the real beneficiary), are not getting these additional benefits?

-

For PPP in Affordable Housing, is it true that the annuity and hybrid annuity models are finding favour with the Developers? What are the main issues here? Is Risk Mitigation the main issue that makes one PPP model more attractive over another?

-

Is it a fair assessment that in the initial one or two years, it is the Ancillary players who will be the first to take off - show faster/better financial performance, because a) the builders and the housing finance businesses will naturally show performance with a lag effect -post construction completion/sale? b) scope of opportunity is limited for the latter in Phase1

-

Which are the one or two main segments within the Ancilliary space (Other than Cement) – that is expected to get a big tailwind to existing growth rates?

For example, there are certain segments in Ancillaries like Paints where replacement demand to New Demand is high and the industry grows at a fair clip, so AH opportunity may not be the same tailwind for the Industry as say for Pipes or Plywood where the replacement rate is low? -

To be profitable in this kind of a low-margin, high volume industry, Sourcing becomes as important as Execution. How do you think Sourcing for ancillaries will evolve – will the top ancillary brands be able/willing to supply volumes at much lower rates? Or, will the 2nd rung brands be the major benefeciaries?

-

Among Builders – Is it a fair assessment that the top 10 builders with comparatively better nation-wide presence be the ones to make the most of the opportunity? Or, large number of smaller regional/local players will be the major contributors to the volumes?

-

What has been the impact of GST? We hear GST has dmapened the demand -for under construction flats there is 12% GST, but no such things for flats which are ready for occupation?? So buying is getting delayed as buyers prefer only ready-to-move-in flats?

-

What about approval rates, post RERA. Lot of changes to development rules, have things stabilised now? Are approvals coming on time?

Based on incremental learnings we can keep refining this initial query set with help from you all. Next time, some other member can use this to validate learnings from another builder/developer or construction player that he/she meets up with.

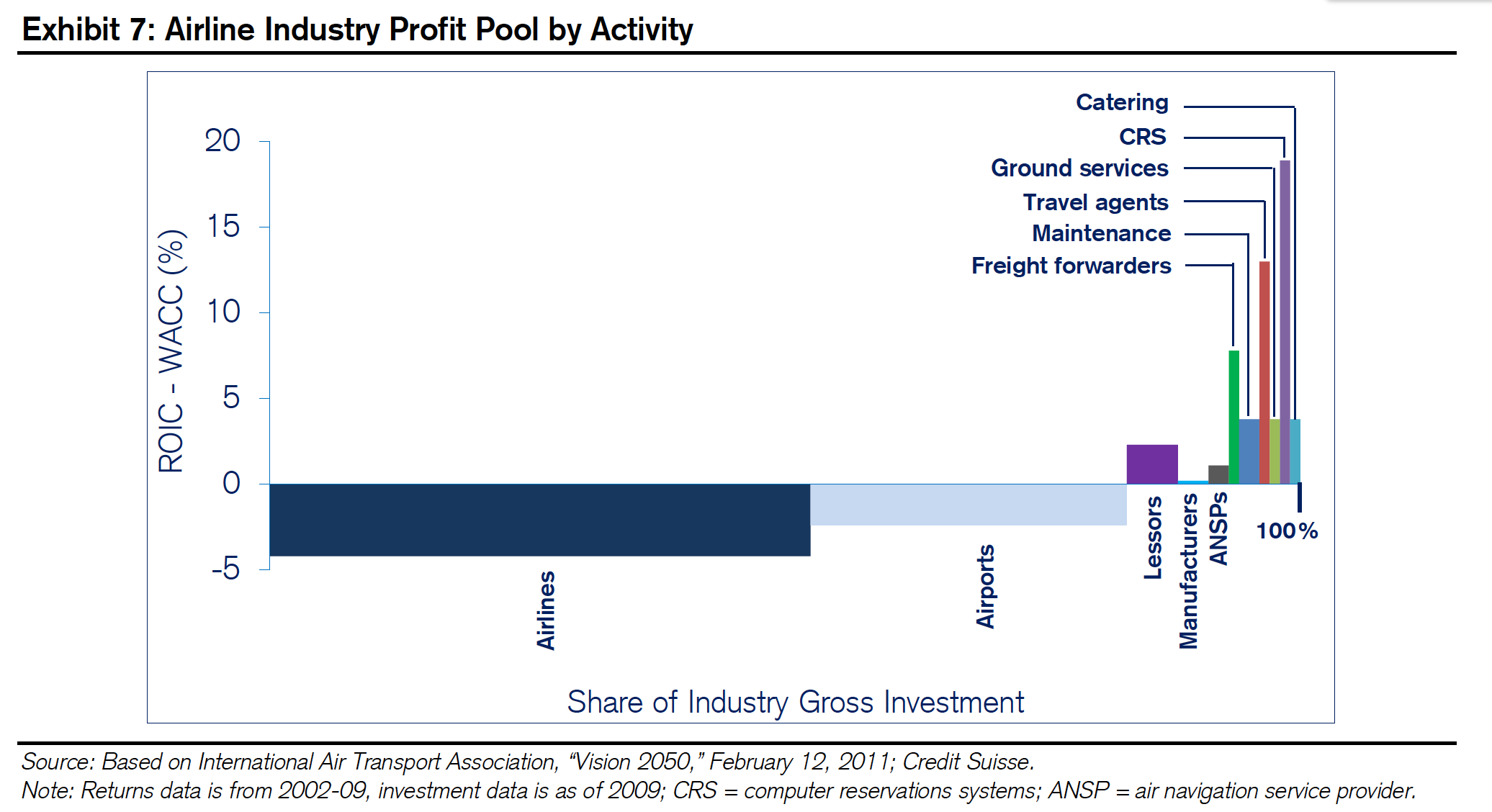

The next job is to create an Affordable Housing Industry Profit Pool by Activity. (On the lines of the Aviation Profit Pool example above)

I approached our friend @Yogesh_s for help on this - he is the best industry-data cruncher I have met  .

.

He suggested getting back to him first with data breakups for a typical affordable house of say 20L (and 35L and 50L) - how much is the pie for the ancillary set first - in the overall construction pie. just like for a typical ticket purchase of 5K - say Airline takes 2.5K, Govt takes away 1.5k perhaps in taxes and surcharges, Ticketing guy takes away 300, Catering takes away 100, and so on - how much goes in cement, how much for steel TMT, how much for paints, tiles, electric cables/fitting, plumbing pipes, plumbing fittings, and so on.

Similarly we might also attempt to extend this to the pie for construction, pie for land cost, pie for financing and the like. The purpose is NOT to do an exact numbers job (which may be impossible), but to arrive at mota-mota understanding of where and how Money gets made/will be made in AH at aggregate levels - the rough profit pool. The exercise is certainly not expected to lead to investment candidates - but alert/direct us better towards our usual bottoms up stock picking based on active field-level scuttlebutt.

Next, if we get back to Yogesh with a list of (lesser known?) names in Tiles, Roofing, electric cables, construction chemicals, steel TMT (able to supply in scale) - again based on fieldwork among builders/construction companies - he can give back to us a better sense where to focus on for bottoms-up stock picking. @Yogesh_s please correct/modify if I have mis-represented anything from our conversation - on how to go about this top-down exercise

We will revert back on this, with some initial data-set/model. Those among builder community like @bheeshma or @bobbyusd and others can certainly help us. Those who have recently got a house constructed/negotiated would also have a good grip on this. Together I am sure we can get back to Yogesh with what he needs

You are spot on @donald.

To build a profit pool we need to build the revenue pool first. This is simply an estimate/actual data on who gets what piece of the pie. When a house is sold, many businesses get a piece of the pie. If we can determine the size of each slice and do the ROIC-WACC analysis for each slice we can figure out which slices are attractive.

From what I know, following is a general list of businesses/entities/people get a piece of the pie when a house is sold. Not all entities will be applicable in each case but we can generalize it for a large pool of sales.

- Land Owner

- Land Developer, architect, lawyer and agents (deal makers, paperwork agents)

- Government fees, taxes etc (official)

- Speed money & other payments

- Public Utilities (road, water, electricity, sanitation etc)

- Construction Company (the one that actually builds the house)

We can cut last slice into smaller slices ( because this is where I think there will be some investible opportunities)

- 6.1 Construction Materials (Cement Steel etc)

- 6.2 Tiles & sanitaryware

- 6.3 Electrical

- 6.4 Plumbing

- 6.5 Paints

- 6.6 Appliances & furniture etc.

Add anything to the list if I have missed something. As Donald said, this will be an approximate exercise to get a high level view of who gets how much.

Once this is done a list of companies that provide these services is needed. These are the recipients of the opportunity. Once we have the list and and approximate size of the opportunity for each of the industry in the value chain, we can do our regular bottoms up analysis.

Found this presentation from Shankara BuildPro on this forum. Slides 15 and 16 will give basic info on the percentage of each type of material that will be consumed.

Disc: This is my first post. Not invested in Shankara.