Convinced look too strong word when every quarter promoter gives some reason n promises a great quarter next time. Reasons nay be genuine or cooked up but they have scored a big 0 on trust factor n ability to live up to words I believe based last 3 quarters of commentary . Disc : had a tracking position n exited few months back

4 Likes

Given the current valuation results doesn’t seem encouraging. With market at new highs its always better to stay sideways until clear picture emerge. I will re-look at the company post 1-2 quarter results or at Rs.200 whichever comes 1st. Seems overvalued at the current price.

Though I believe in their business but the behavior of the promoters has not been comforting to say the least. They felt the need to split the share, within one year from the listing date…tells their obsession with the stock price. They have at multiple occasions over promised and under delivered on operational performance, which confuses and irritates investors. Further, the poor attendance of 2/3 of the promoters on the board for last two years also raises concerns over the engagement of the management with the board.

Disclosure:

Invested in IPO

SJ

6 Likes

After reading multiple posts here, also managements delays for quarterly results, I am turning negative on this otherwise good company. Definitely, they have high entry barrier and tech-moat, but some points make me wonder:

- Why Sri Sri Ravishankar trust invested in this company?

- Why management delays results?

- I am not able to understand why there are so many subsidiaries and new acquisitions and restructuring this subsidiary chain.

I am waiting for Q2FY18 results and then decide.

Disclosure: Invested 2.5% of my pf.

1 Like

The Rathi’s are ardent Art of Living followers.

3 Likes

There is a lot of negative sentiment about the management’s guidance because one “major customer” who suddenly gave dwindling volumes.

Also, the fact that Novozymes is the undisputed leader. Coupled by the fact that when enzymes is a small fraction of the cost of making the product, why would anyone switch loyalties.

Both the above are fair arguments. Knowing the above, I have still went ahead and invested about 10% of my pf. Reasons:

Firstly, I love the fact that the promoters itself are the sceintists / technocrats. For this fact I give immense weightage, compared to “hired brains”, which might not stay long with the company.

Secondly, Enzymes are a natural catalyst, replacing chemicals. See the way the world is going, and one would realize this is the future!

Thirdly, they have multiple patents, a global player and no pricing pressure…an awesome combination!

But with all this, why arent they growing exponentially? Enzymes are now being commerciaIized in detergents, animal feed, nutraceuticals & health care…guess the whole enzyme market would need some time to penetrate into more products in a deeper way. Like how the palm oil enzyme is being developed by the company for 2018-19.

I wouldnt expect this to be a multibagger, but I have a lot of conviction that this would be a good compounder. Offcourse, management is not yet tested over time. Since they have increased stake this year, I would not be too worried on this count.

Disc: Invested.

11 Likes

Just to note: The merit of holding patents should be completely judged based on nature of the industry. Ex. getting patents in biochemical products, chemical products is easier than getting patents in hardware IC design.

1 Like

http://www.bseindia.com/corporates/ann.aspx?scrip=540025

Quarterly result.

If they screw up on this - Stock will tank for sure and if they achieve this then this is already discounted in the price today.

May be if they achieve 380 - 400 Cr topline and 100 Cr of net profits then may be 15% upside if stocks going to trade 35 times earnigs.

Can’t agree more

Regards

SJ

Any news or what ? Stock went up drastically with good volumes.

Hi.

A big chunk of cash/cash equivalents are in current account. They could add interest income by investing it in FD or other instruments. Any idea what the reason could be?

Dicl. Not invested. Tracking closely.

-Anand

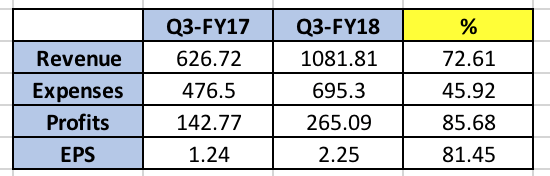

Decent results posted by the company

Results and Investor PPT:

http://www.bseindia.com/xml-data/corpfiling/AttachLive/f0c226c2-71d2-4d80-99d9-09521307e3f4.pdf

Disc : Invested and added more in this recent fall

2 Likes

1 Like

@paragasraj : This is VP Forum, you will be presented with facts about the company and decision to buy and sell will be entirely yours. I am sorry to disappoint you, but such questions may not be answered here. SEBI also doesn’t permit such recommendations on public forums.

2 Likes

Thanks Sarabjeet. Much appreciated. So my question is how is the present artifact about the company?

At this point market sentiment is bad in general, specially for companies directly/indirectly related to pharma. So Adv Enzy is also affected. Moreover valuations were on higher side hence fall was also higher.

I am accumulating this as a SIP. Because its quarterly numbers are not very consistent, hence we cant rely on last good quarter.Who knows we may get this at a even better price in next few weeks for long term holding. I will complete my buying over next few months depending on turn of events.

Disc: I m invested and views could be biased. Pls do ur own research before investing.

4 Likes

Very good blog on Adv Enzymes LTD, Seems like it was trading at very high valuation & now it seems to be at fair valuation .

https://dhruvapandey.wordpress.com/2018/03/31/advanced-enzymes-ltd-part2/

7 Likes

now it seems to be at fair valuation

for FY19 or FY20?