Could you pls share the source of your image…

At current prices around Rs.230 and a market cap of 2500 Cr, if management’s guidance of 380-400 Cr topline is to believed (170 in first half achieved and 210 in second half - they have done 110 already so we can expect 100 Cr topline in Q4), a bottomline of 95-100 Cr looks possible and we are trading at around FY18E P/E of 25. Enough has been said about the moat and niche business but the valuations always kept me away. This may not be a great bargain but relatively based on the steep valuations it commanded last year, what it is trading right now at seems very reasonable.

Disc: Invested recently

6 Likes

I feel that the palm oil extraction plan, if executed properly could be a major game changer for the company. Malaysia and Indonesia together account for 90% of the world’s total palm oil production and AETL has been granted a patent in Indonesia. In addition, as we know, the company had also acquired a Malaysian company which should help with building the business in the local market.

A factor that could adversely affect the above is the world’s growing concerns regarding the environmental damages caused due to palm oil extraction. A mere google search for palm oil reveals how damaging it is to the forests. That being said, as of now palm oil is so deeply ingrained in everyday products that a sudden shift to other alternatives is all but impossible. What rather is quite likely to happen is that oil extraction process might need to change and become less damaging by following certain guidelines. How this might exactly end up affecting AETL’s plans I’m not too sure, but I feel that some more research into the future of palm oil extraction will be helpful to us as investors.

The below presentation sums up the company’s position and progress with regards to it’s palm oil endeavours quite well. What remains to be seen is whether they are able to monetize their plans efficiently and as stated by FY19/20.

8 Likes

Confused … as is visible from conf calls, promoter is super confident on the company future then why is he selling stake rather than increasing it.

At the same time a reputed MF buying reflects mkt confidence in the company.

1 Like

what % of MF portfolio ?

@AmitContrarian : If you consider AE shares as percentage of MF portfolio then it may not be significant due to the structure of MF schemes. They own plenty of companies and have their rules for % allocation.

However HDFC buying 2% stake in the company definitely reflects their confidence in the company.

As per AEs March update, 4 MFs held about 3,425,077 shares. Now HDFC added 2,330,535 alone. Which makes over all MFs stake around ~5 %. I would have been more happy if this stake would have been added from open market as that would have sucked liquidity further and free float for trade would have reduced giving strength to price.

FPIs has also increased their holding in Q1 from 2.42 to 3.74% in the company

2 Likes

There has been release of pledged shares today. Going by the BSE announcements, the pledging appears to have been reduced by around 5.32%.

Is it possible that the promoters reduced their stake in order to release some pledged shares?

Maybe with Money they received after selling stake to HDFC they got the pledge released.

Which is a gud sign and some indication where that money got used.

2 Likes

Why they will use personal money to pay the company loan ?

They are not paying company debt, they are releasing their own pledged shares.

Without paying Debt how the release will happen ?

A promoter can pledge shares for his personal needs as well and whenever he get access to Money then he can get them released. So its not necessary that pledging of shares is for company debt.

That is what we are assuming that money raised with stake sale to HDFC was used to get some of the pledge released.

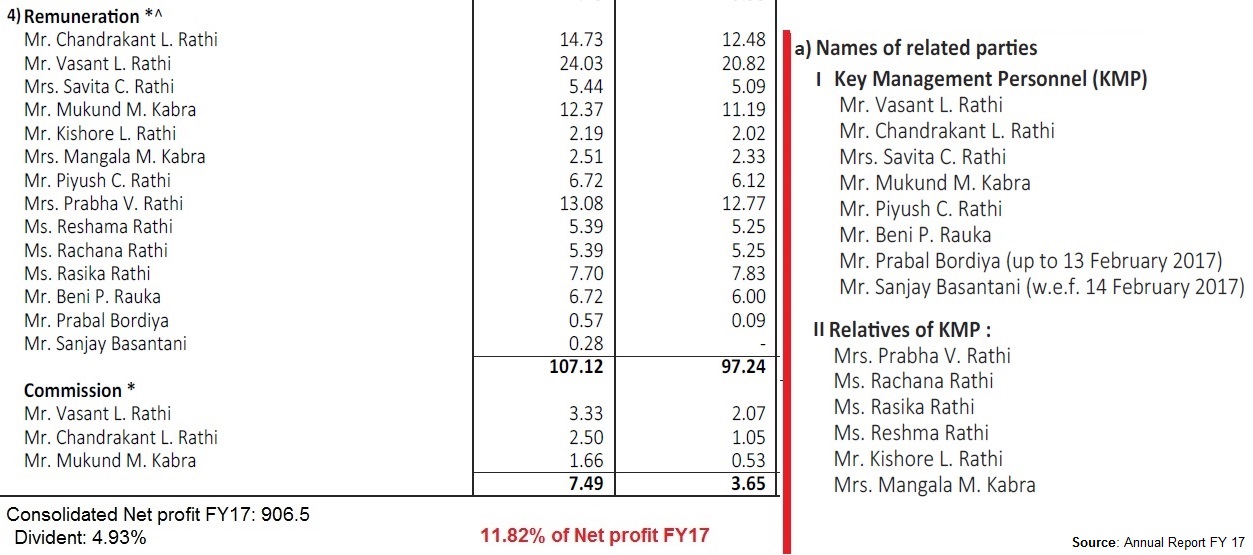

Good financials, cash flow and margins. But while reading the annual reports, I noticed a couple of potential risks.

1. Promoters’ Remuneration

All managerial personals, directors and their relatives are taking high remuneration with huge increase YoY, even if business doesn’t meet the expectations. During 2013-14, net profit decreased by 59% while average remuneration increased by 17%. I personally have no issues with management taking high pay as far as the cash flow is good, but on long term, it is definitely a red flag. I can’t be sure that any critical decision in future will be in best interest of minority shareholders.

2. Company’s Technical Proficiency

I have doubts about the business meeting its operational efficiency especially when after the operations scale up in future. The following notes are taken from annual reports.

(a) “Advanced Enzymes USA, Inc. had received written demands from clients for approximately USD 3.90 million, based on allegations that its products delivered to the clients did not conform to certain preagreed specifications. The company had been advised by the legal counsel that it is possible, but not probable that the claims would succeed and accordingly no provision for liability was recognised in the financial statements.” – Annual reports FY 2014-15 / FY 2015-16, Note 24.A Contingent liabilities.

(b) “During the second half of the year, some of the lots of products exported by the Company to USA, Japan and EU reported to have potential contamination with trace amounts of antibiotic Chloramphenicol. Accordingly, Specialty Enzymes and Biotechnologies (SEB), who has done, voluntarily recall of those specific lots of enzyme products and the company also got goods returned back from some its overseas customers in EU, Japan and USA” - Annual reports FY 2013-14, Review of Operations and Financial Performance.

Most of us must have heard the story of contamination, but I didn’t see the management taking responsibility and explaining the steps taken to make sure problems like that never happen in future. Of course company did a “voluntarily recall”, but this is a key risk, especially in a regulated industry like this.

DISCLOSURE:

I don’t own the shares.

My analysis is subjected to human errors, please do own analysis and make decisions.

6 Likes

1 Like

Receivables has gone up and indicates the price they had to pay for top/bottom line growth. Was anything mentioned about this in conf call?

Few notes from concall

Nominal growth projections. Company gave guidance of 440 to 450 Cr topline and EBITDA of 195–200 for FY-19

This is inspite of tax reduction in US from 38 to 28%. However in India they mentioned some SEZ benefits may not be available anymore. Consolidated tax rate around 29%.

Avendus debt was raised at promoter level and not for company.

Pledging maybe reduced this year but no targets given.

From recent EVOX acquisition they hope to get 25 cr topline.

In US they r planning to expand B2C business.

Whatever sector was not growing or shown degrowth, their answer was standard “we are going through consolidation phase and would grow going forward”

I was wondering if they will grow in every product segment (EVOX, JC Bio and core business) then why such a low forcast. One fellow asked same and they said they are being conservative.

3 Likes