Are these IT searches a common practice ?

Also given the past track record of the promoter, having no CG issues, could this be more of a tax harassment case?

Disc- Invested

Are these IT searches a common practice ?

Also given the past track record of the promoter, having no CG issues, could this be more of a tax harassment case?

Disc- Invested

The promoters have a clean past , there is no denying that fact. Management interviews and annual report also hardly raises a eyebrow against any CG issue. Can there be a cockroach lurking , chances are pretty low. Can this be a case of year end target reaching exercise or drill by IT Dept…chances are high. How does this affect the business, not really.

I will be buying this on dips. In the long run fundamentals and results might dominate this one off event …though fingers crossed and expecting not.much to come out of it.

Disc : invested and will add on lower levels

"The buzz is that we are getting extra benefit in the global supply chain, because we do not import anything from China for our specialty chemicals business. We are totally backward integrated. Looking at overall macro factors and other sectors globally, we should be able to maintain this growth momentum next decade too,” Gogri said.

Which are the other backward integrated chemical stocks?

Find enclosed link for calculation of XIRR to shareholder since listing of Aarti Industries.

Results and dividend declared

nsider trading updates for 2020-02-20

| Company | Person | Person Category | Holding pre transaction | Num of Shares | Value (Lakhs) | Transaction type | Holding post transaction | Mode |

|---|---|---|---|---|---|---|---|---|

| AARTI INDUSTRIES LTD. | DILIP TEJSHI DEDHIA | Promoter Group | 132990 (0.08) | 10287 | 101.76 | Disposal | 122703 (0.07) | Market Sale |

| AARTI INDUSTRIES LTD. | RATANBEN PREMJI GOGRI | Promoter Group | 768098 (0.44) | 3323 | 33.61 | Disposal | 764775 (0.44) | Market Sale |

| AARTI INDUSTRIES LTD. | RATANBEN PREMJI GOGRI | Promoter Group | 764775 (0.44) | 2300 | 22.71 | Disposal | 762475 (0.44) | Market Sale |

| AARTI INDUSTRIES LTD. | CHANDRAKANT VALLABHAJI GOGRI | Promoter | 852005 (0.49) | 17752 | 177.34 | Disposal | 834253 (0.48) | Market Sale |

Promoter selling stock continues. What to make out of this ? Anyone tracking Aarti for long time would you please comment how to view this.

This is concerning for me as well…seniors please advise

These seem to be in smaller tranches, thus not impacting demand supply balance and price is holding okay.

Cummulative would be sizable. Selling during such downturn doesn’t sound good but again mkt seems unaffected with prices holding steady, says something about mkt trust.

Tracking position.

I think one has to be careful while investing in equity market. We need to control allocation in portfolio which provide peaceful sleep to us. In case we find, that promoter selling is not a good sign, please trim your holding to level that assist you regain peaceful sleep. The promoter has been selling constantly for 2-3 years in my limited understanding.

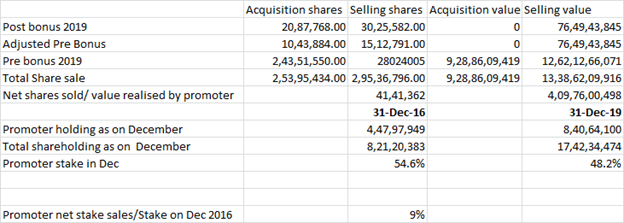

During Jan 2017 to March 2020, as per Data complied from BSE Disclosures under SEBI (Prohibition of Insider Trading) Regulations,2015 ([Regulation 7 (2) read with Regulation 6(2)] The company’s promoter have cumulatively sold 46.10 Lakhs (adjusted for Bonus 41.41 Lakhs shares) worth share value at Rs 409.76 Cr. During same period, share price increased from Rs 359 to Rs 945 (10:45 am 9 March 2020). Total stake sold is around 9% of total stake held by promoter on December 2016. Please note that this stake sale would also include two buyback which compnay announced during the period.

I am enclosing snap shot of working for everyone reference and detail excel file is also attached to provide my basis of my working.

It is difficult to say what to infer from this data. I personally apply the first level of principal when such difficuly arise for me i.e. At what level of allocation in my portfolio, I would sleep peacefully? Today, I sold around 22% of holding in Aarti Industries, just to creat cash in volatile market in days to come and also align my high allocation to Aarti Industries. I had been holding Aarti Industries since August 2014 and systematically selling same to get my portfolio balance alignment in order.

Please note that each individual requirment of return and risk profile are different. Hence, get working to decide your own peaceful sleep level in any company including Aarti Industries. Happy Investing.

Discl: My view may be biased. Even after today’s sale, Aarti Industries is my top holding . I am not SEBI registered advisor, I am not recommending anything on this stock. My interpretation of Data may be wrong.

Aarti Industries Insider_Trading Jan 2017-March 2020.xlsx (109.4 KB)

Thank you @dd1474 for detailed work to analyse last 3 years transactions by promoter and how the stock price behaved during this period where promoter holding went down from 55% to 48%. When we look only occasionally we miss the forest for the trees.

Do you know if these promoters investing these in to another group company as such - listed or unlisted ? This is especially interesting to know as Aarti Ind has large number of promoters (44 in total) with highest holding of any promoter individually is only 4.4% as of dec 2019 holding.

I have no access to information about promoter plan to deploy sale proceeds. And frankly, with my 20% allocation if I see so concern in turmoil, even Promoter family also deserve to have diversification in their income source if their almost 90% wealth (my assumption) is tied up in company. While I know the promoter run the business and has control while Minority sharheolder has no say in running of company, still even if promoter selling stake in company and investing in new business, I would not see prima facie negatively. Only if there are related business transactions which benefit new business at cost of old business or other similar issues, then I would consider negatively. This is my view and may be wrong. Only time will tell true story and for that we all need to wait.

I mailed the CS to get more details about the promoter selling. Please find below their reply

With respect to your enquiry for reasons on trading by the promoters, we like to clarify that there is no significant trading, however, in the recent past there have been frequent trading by a few of the promoters and the reasons are as under;

Based on first cut reading, I believe there would be high cost input cost which may have impacted performance in Q4FY20 in addition to Lockdown. Having said that, let us wait for management call to get insight. Overall, in the context of environment, I find result quite satisfactory except for profit margin which appear to be under pressure for obvious reason. Segmentwise results also showing good improment in Pharmaceutical segment relatively.

Discl: among my top 2 holding and sold nearly 40% of holding in last two months to increase cash level. View may be biased. Investor shall do own due diligence before any investment decision. Neither recommeding stock nor SEBI registered advisor.

The company has done great in terms of revenue both YoY (removing Homecare) & QoQ. Although the revenue is flat, its majorly because the pricing is based on crude.

In such situations the bottomline should be not be taken at face value because of the following reasons-

Also Pharma has done better compared to Spec Chem

CFO has increased by 50%, mostly due to WC management.

Also long term debt has been reduced by around 260 cr

Demand outlook is a key here as there is going to be a slowdown in Paints, automobile & Adhesives etc

So Aarti has formula based pricing , Management is clear in its view is that top line might keep fluctuating based on raw material cost. So better way to look at the result is EBITDA and EBIDTA margins because of late aarti is trying to focus on low volume and high margin value added products which reduces storage and transportation costs and increases EBITDA margins. As per management EBIDTA should sequentially increase and reach 40% in coming years. For this quarter EBITDA margin are reduced by 200 bps YoY and 300 bps QoQ which is bit disappointing.

Multi year contracts in pipeline, favorable product mix and diversified products makes Aarti industries a company to watch for and stay along. One big advantage is most of their revenues are scattered as well so it is not few clients heavy business. Most of their products are in top 3 globally.

Few of the things to watch for:

Personally i believe Aarti and Vinati are great companies in speciality chemical space who are market leaders in their respective line just that Aarti has more product range than Vinati which has around 4 products.

Disc: Invested and will be adding more in this downturn if it is available at fair price

Thanks for sharing Lokesh. Curious to know what you think would be a fair price considering the points outlined and the favorable tailwinds.

I did share a post with my calculations but i guess it got deleted.