Looks like the rumour I had heard was somewhat true. From article below, looks like total PMS funds is at Rs. 11Lakh Cr + Rs. 22Lakh crore (mirror portfolio). Guess lot of this quick money will have to wasted away for small caps to recover. That is how the market works. No free lunch.

2 Likes

Numbers are way off here. 11 lakh+ Cr under PMS is way too high when the entire MF industry (fixed income included) is under 25 lakh Cr

A number of 80,000 - 90,000 Cr is more realistic for PMS. As usual the devil is in the definition of “portfolio manager” - check this article from the same ET Portfolio managers' assets swell to Rs 13 lakh crore in July-end - The Economic Times

As per this 10 lakh Cr is discretionary and only 79,000 Cr is non-discretionary PMS (the ones HNI’s invest in - Motilal Oswal, ASK, Alchemy, Kotak, ICICI etct). We really need more sensible people writing media articles - God knows what this 10 lakh Cr is all about and who are these portfolio managers, article also says EPFO contributed 9 lakh Cr of this!

8 Likes

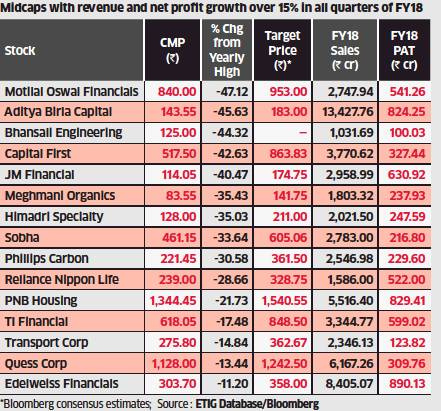

Ready to Roar? Battered Midcaps with 15%-plus Growth Could be Value Picks

CLOCK OVER 15% GROWTH IN ALL QUARTERS OF FY18, STOCK PRICES CORRECTED 10-50%

. — Rajesh Mascarenhas

Several midcap stocks, which saw a sharp price correction recently, have reported healthy growth in revenue and profitability. Companies such as Motilal Oswal Financial Services, Aditya Birla Capital, Bhansali Engineering, Capital First, JM Financials, Meghmani Organics and Himadri Speciality Chemicals are among those that clocked over 15% growth in revenue and net profit for all the four quarters of the previous financial year. Yet, their stock prices are trading 10-50% lower than their annual highs. Investors picking stocks on their own should take advantage of this correction to reposition their mid-cap portfolio, suggest market experts. Some of the quality midcap stocks were corrected not because of fundamental reasons but due to trade war, rising commodity prices, the prospects of hardening interest rates and the political concerns. “This is precisely the opportunity for buying into mid/small-cap space as a result of attractive valuations Vs their long term historical valuation multiples,” said Ajay Bodke, CEO-PMS, Prabhudas Lilladher

Economic Times , Mumbai Edition dt 27.7.2018

1 Like

In the long run, Market is slave of earnings. So If earning is in increasing trend, market may remain in uptrend. Looking at the Auto sells data(easy way to see earning growth), it is can be clearly seen that earnings are in upward trajectory.

So I don’t think waiting for market crash is prudent thinking…

I think this Carnage opportunity should be utilised maximum as some quality stock s are available at bargain price…

Hello all.i was looking at valuations of companies before bull run I.e before 2014 many good companies have pe multiple below 10 some of examples are wim lopala cera etc.it indirectly means that 1.only valuations are costly in relation to company performance of growth in sales and profits.2.are we paying blindly for growth in bull run? 3.can this companies return to their normal pe multiple?

1 Like

These companies were out of flavor over 2005-08 bull run which had sectors like infra, real estate, commodities and hence post 2009 when the flavor changed they have got affected by 1: cheap liquidity, 2: Consumption theme has been the favorite of this bull run.

To understand this concept better look at the prices of stocks in the consumption basket over 2003-08. These companies gave negative returns/sideways return over a period when the index returned more than 20% CAGR

1 Like

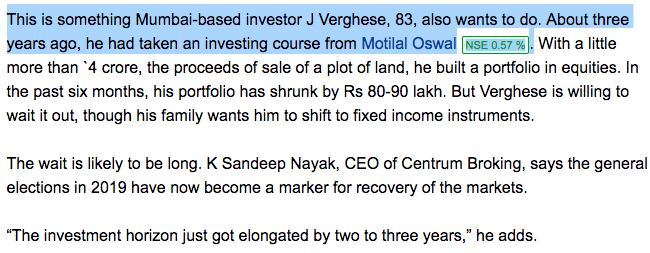

Someone at age of 83 took equities with all he had (Rs.4 Crs by selling land) and lost 25% (90Lakhs) and some so called advisor saying he has to wait 2-3yrs to recover his loses (at 83 !), while the family members want the remaining assets to be moved to fixed income instruments.

2 Likes

Thank you for reply can you please mention sectors which are out of flavour in this present bull market?

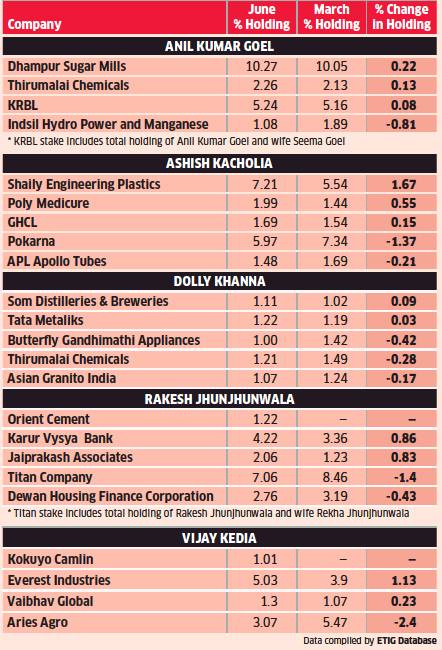

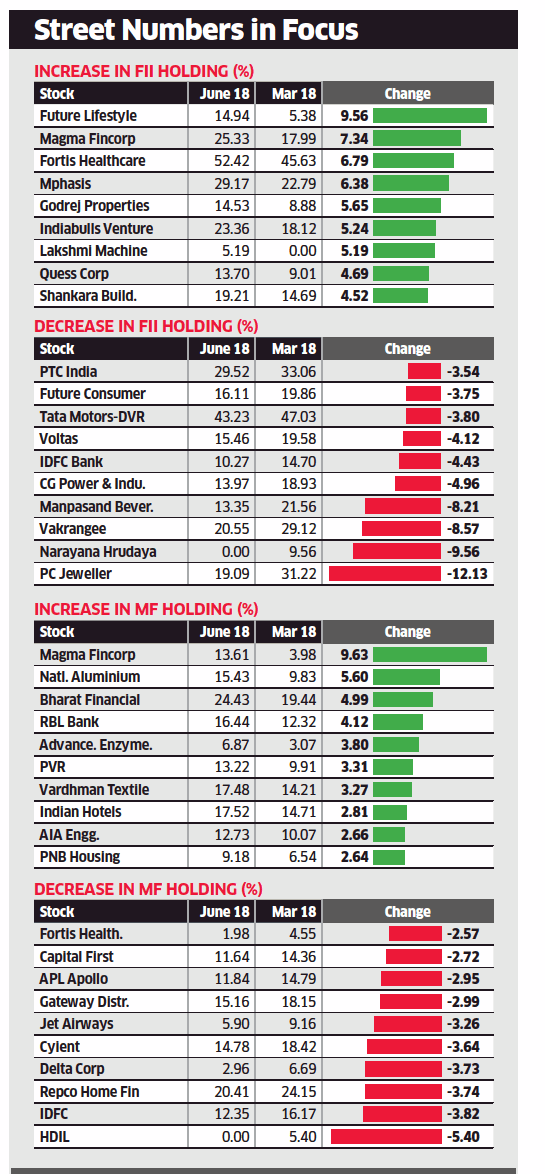

The buying and selling moves of well-known investors of Dalal Street are keenly watched every quarter. ET takes a look at the changes in holdings of investors such as Rakesh Jhunjhunwala, Dolly Khanna, Vijay Kedia, Ashish Kacholia and Anil Kumar Goel in the quarter ended June

The article merely mentions that he sold a piece of land for Rs 4 cr 3 yrs back and invested the proceeds in equity. It nowhere mentions or implies that that piece of land was all he had.

Again, the article nowhere mentions that 25% figure. In fact, it clearly implies that he lost Rs 80-90 lakh from his peak equity portfolio value. If we combine this with the fact that he constructed his mostly midcap portfolio 3 yrs back, the Rs 4 cr would have increased to about 6+ cr peak value sometime in Jan, 2018 (assuming the return equivalent to an average midcap fund over the period), and then declined about Rs 90 lakh from that Rs 6 cr + peak.

The article nowhere suggests that an external advisor is asking him to wait for 2-3 yrs. In fact, the language of the article clearly implies that it is his own decision to stay invested. In fact “2-3 years” is not mentioned anywhere.

Although my pointing out these discrepancies might appear to be nitpicking, I just wanted to emphasize that we should not color something we read of hear with our own prejudices. That way we end up interpreting something very different from what is actually being said.

10 Likes

He has taken the course, 4yrs ago, didn’t sell the land 4yrs ago. There’s a full stop you see !

“The investment horizon just got elongated by two to three years,” he adds.

May be you need to re-read multiple times, if he had made enough gains as you say (entered 3yrs back), their family members won’t be worried much for a mere 90lakhs loss from 2Crs gain. He is saying he want to wait it out, if someone made a healthy gain, why would he wait it out to recover that lost gains, when family members are worrying to protect the capital/investment sir ??

Anyway, I didn’t write anything of my own or didn’t try to color someone.

The whole point of sharing this is to not become greedy… to understand the age-risk reward, not to jump in with all someone has into equity at the age of 80.

People just jump in after seeing 2014,2017 kind of year and get caught after seeing the reality. Here’s an another example:

2 Likes

With respect to this thread,the midcaps and small caps have made some recovery of late and have recouped part of their losses pretty quickly.However from valuations perspective,still the sense of frothiness exists in the market and the stocks by no means have become as attractive as during 2011-2013 period.

There was a lot of money which was waiting to be deployed expecting further deep correction and most of it is still waiting.

This recovery seems to be due to the reason that domestic investors have continued pouring money into the market despite the sharp fall which is quite a new phenomena in India markets as usually domestic money was nervous money and it got pulled back fairly quickly at such corrections depressing the markets further.

Now its going to be interesting view till elections atleast whether the investors will return to the small and midcaps and drive it to past euphoric levels or the midcap/smallcap market will remain range bound waiting for earnings revival and political clarity.

1 Like

A Catch 22 Situation Unfolding

1 Like

Markets run a lot on sentiments and liquidity besides earnings. . I think till now we have had full doses of first two in the past 3-4 years. If one were to see a bit further down the line

Sentiments: Biggest sentiment booster/dampner for Indian markets is political stability. Since we have had political stability for past 4 years we seem to be taking it for granted going ahead also. But if one were to map mood of voters, it seems BJP definitely is not going to get the kind of seats it got in 2014. In fact it could struggle to make a clean majority of 272 and would have to depend upon allies to bail it out and these allies would demand their pound of flesh off and on. This could create a serious dent in sentiment factor.

Liquidity: We seem to be in a slow but steady rising interest rate scenario in India as well as the US system. We have had FII withdrawal since past few weeks and months but this time the domestic gush of liquidity has taken care of the bouts of FII selling. But I feel a lot of this MF schemes are mis sold as was the ULIP scheme. If and when returns start showing stark negative numbers in these MF schemes there could be redemption pressure which one has to bear in mind.

Earnings: After a long time earnings seem to be perking up for a lot of companies even in small and midcap space. This is a positive. The only problem seems that its difficult to find good quality companies with reasonable set of earnings at decent valuations.

Personally I keep looking out for companies which seem to be showing signs of consistent and predictable growth and which are free from govt interference and available at reasonable valuations. I remain cautiously optimistic but feel that the upcoming elections and their results could provide multiple entry points in well chosen companies.

40 Likes

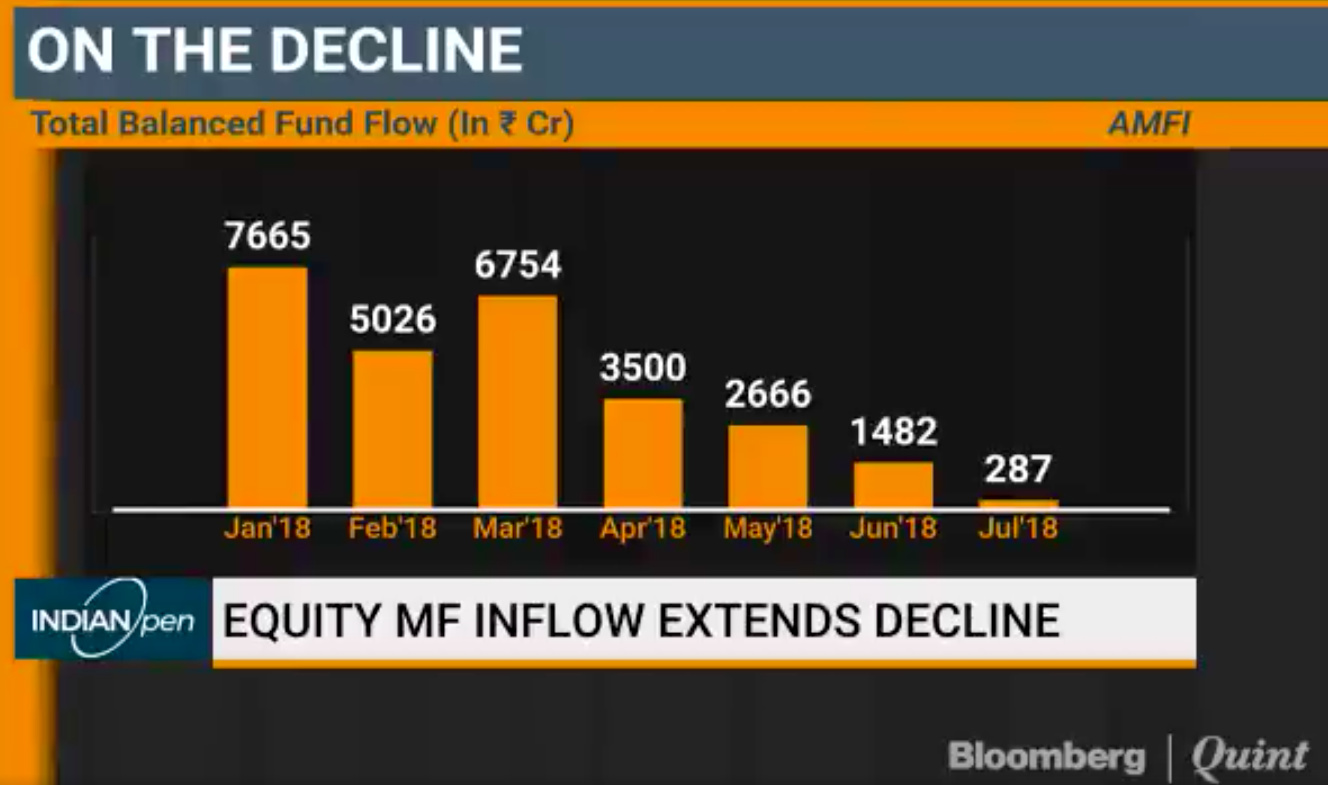

You need to see that the histogram represents balanced fund inflow. The real picture will be depicted by pure equity funds inflow.

1 Like

Hi

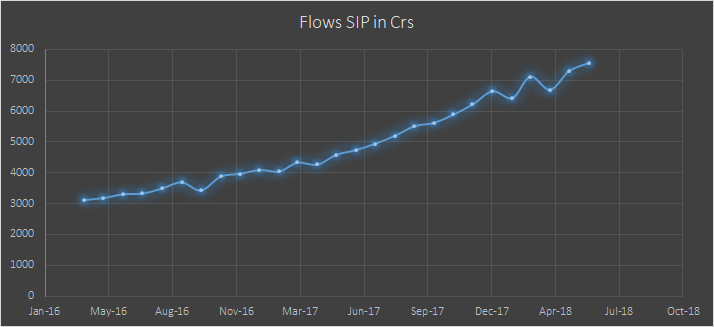

SIP flow data has not been released by AMFI for July. Current chart is as below.

Source: AMFI

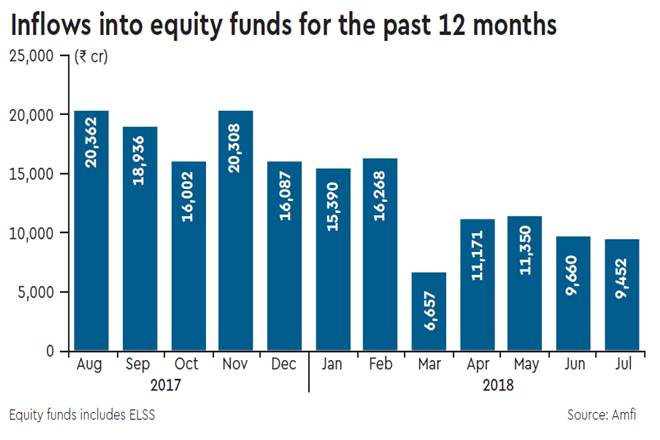

But Equity Inflows to MFs is available.

Source: Financial Express

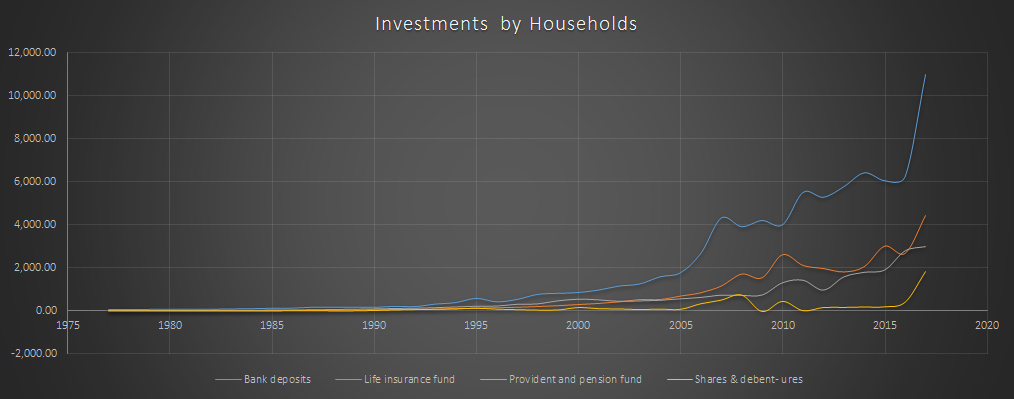

If we take a step back there has been a major shift in preferences to invest in capital markets.

Source: Annual RBI data release.

Rgds

Deepak

7 Likes

Dii Liquidity part

1 Like