Agree broadly and understand where you are coming from. I guess it depends on the individual’s investment style. I have found it helpful to maintain a healthy skepticism and try to seek answers to the areas which are possibly early danger signs (e.g. promoters selling, capitalizing of expenses etc.).

Let’s see how this evolves.

1 Like

8k miles is a bet on leadership of Suresh Venketachari not of CFO or any other person.

We don’t know DSP BR strategy behind purchase. It might be momentum strategy, to catch up MF performance …if you look into its history they played many times such tricks …that’s why turnover is high !

Possible.

In any case, I am positive about this company and its earnings visibility till 2020. And so, I am fully invested!

1 Like

Q3 Results out Revenue up 58% on YoY basis

1 Like

This is an interesting development.

8 k miles is in technologies where the future is

1 Like

Q3 - Results link and PPT :

https://www.bseindia.com/xml-data/corpfiling/AttachLive/482df4c3-696a-4937-a4be-7abbd74ef743.pdf

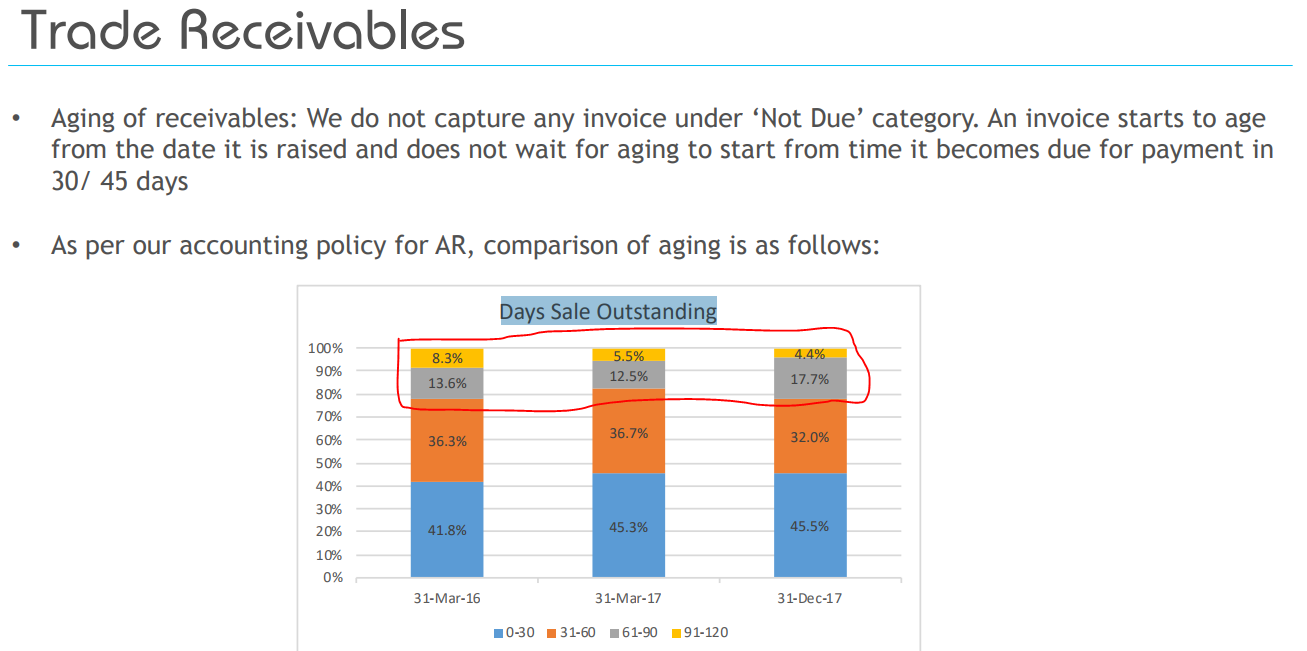

I was looking at trade receivables. It shows approx 20-21% DSO more than 60 days in last two years. Does that mean though they are growing but loosing the 20% of revenue in account receivables every year (assuming they will not be received if more than 60 days ). Should we value the company by reducing this 20% revenue loss from yearly PAT and then assign PE multiple on adjusted PAT.

Or in the past they have received the amount outstanding for more than 60 days.

Please share your views and correct me in case my understanding is wrong.

Disc : Invested (2% of my portfolio )

2 Likes

So - wanted to share a few things on questions about 8K miles:

-

Why raise debt in India @ 10.75% interest rate when they have cash at the US subsidiary.

I hear they did this because they are close to closing on a few acquisitions and therefore wanted access to Cash. Why from India? They want the holding company (Indian entity) to improve its shareholding. Nevertheless they indicated on recent con. call, that they are looking to pare this debt off in case the acquisitions do not pan out. -

Why is the CFO selling out his shares?

Per company, the CFO has some charitable commitments and hence selling…Not sure if this should be taken at face value, but if true - should allay our concerns. -

Buying by any large shareholder typically does indicate vote of confidence - especially they get access to senior management for several hours before they pull the trigger - suggesting they got their queries satisfactorily answered.

Disclosure: Started adding to my portfolio post recent correction at 650 levels…

Mr Suresh is also the CEO of 8kmilesmedia.

http://8kmilesmedia.com/about-page#sec-our-team

The portfolio page is very interesting.

http://8kmilesmedia.com/portfolio-page

Got to know of this info from a Glassdoor review (a negative one ) about 8kmiles.

2 Likes

Time to sell this stock probably?! First sign of something cooking is usually diversification in to a totally unrelated field!

And film production is probably the worst way (or best if the intention is to cheat) to diversify as you can cook the book anyway you like.

1 Like

I also found this some time back.

There’s no indication that these businesses are under the listed company. I’m from Bay area, where 8k Miles HQ is. Though these are not in listed company, India-focused media businesses should do very well in US/Bay area, if executed well. Also, understand that Suresh is a serial entrepreneur, and he is well-experienced in bringing in capable leadership, and execute another venture in parallel.

All in all, I’m not worried because of this.

Disc: Invested from lower levels, averaged up.

no wonder it does look interesting, but don’t you think it’s just too much, and considering that all is into developmental stage as of now, barring few things like 8k radio.

Actually for me this was a red flag.

Couple of other issues:

a)Recent stake sale by CFO

b)Bad reviews on glassdoor. Though the CTO does have nice recommendations on linkedin.

These all could be minor issues, but to my naive investor mind, these are all red flags.

Three reviews at Glassdoor. One from 2015, two from 2016. One +ve, two -ve. Doesn’t mean anything.

Suresh holds 54.5%, Ramani (CFO) reduced stake from 7% in Dec15, to 1.5% in Jan18. Ramani has been with company for long, may have genuine reasons for selling stake. But a valid question for next concall. On the flip side, Ramani’s stake was bought by DSP Blackrock, who were the first MF house that bought it in Aug14.

Don’t see these as red flags.

Apart from software , They are helping software people to get into US. For that they will collect money (H1B) and return it late if they didn’t go through with some deduction in the amount paid. If selected they will help you to stay in US for three months to get a job. By chance git the job, ppl need to pay commission for 1 yr under their payroll i think. I have personally been there to their head office for enquiring this long back in 2012. I didn’t process but my friend processed H1B through them. Don’t think this is job of a software firm. Just my 2 cents . Quite surprised to see a thread on this company here.

1 Like

What you explained was a model of small body-shopping IT firms a few years ago…, and even that was not a fraud. But i don’t expect 8KM to do it these days.

Yes, they still doing this. May be you can check with any of ur IT friends in Chennai. Btwn I’m not saying they are fraud. I’m just saying what i have experienced

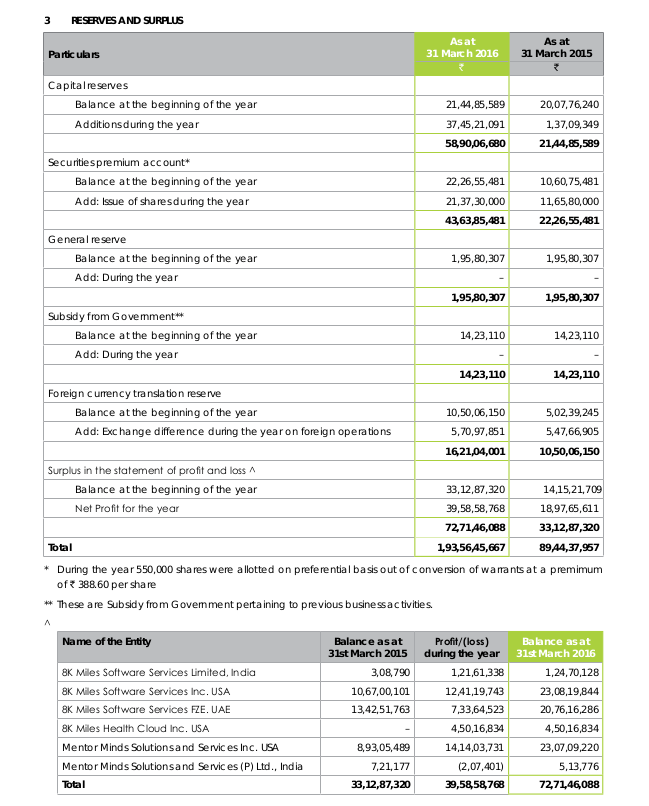

FY16, Reserves and Surplus nearly doubled… Total increase was around 104 Cr:

NetProfit contributes 39.6 Cr

5.5L shares contributed 21.37 Cr

Forex changes 5.7 Cr

Capital reserve increase 37.45

I don’t quite understand the last item (Capital Reserve), From where does this 37 Cr come? Did they revalue some of their assets or sell anything (for more that carrying value?)

Gaurav,

Thanks for your reply. However, I’m not quite able to follow your reasoning. I’m left with the same question: Where does the addition to capital reserves come from?

I’m aware of the acquisitions. Do you intend to convey that the addition to capital reserves is because they were acquired at below book value?