Company raised additional ~25 Cr of long term debt at Indian entity level to fund the acquisition (probably additional payout for cornerstone advisory acquisition done in May-17). I am not sure why the company would borrwo at 8K Miles India and give loan to US subsidiary (8K Miles Inc.) to acquire Cornerstone Advisory, given the fact that 8K Miles Inc. is only ~65% owned by 8K Miles India. This is like giving the benefits of acquisition to the remaining 35% minority shareholders of 8K Miles US (erstwhile promoters of previously acquired companies) at the cost of 8K Miles India shareholders (as 8K Miles India shareholders will be bearing the cost of debt)

Extending the first point, consolidated accounts have Rs. 120 Cr of Cash (mostly in the US subsidiary) and still company is raising debt at parent Indian company to fund the acquisition at US subsidiary company. This looks quite strange.

Although not material, standalone Trade Receivables are now at Rs. 36 Cr which is ~3 times their quarterly revenue run rate (Rs. 13 Cr revenue in Sept-17 quarter). Not sure what is going on receivable side.

@Gaurav_Agarwal, @rvetri@phreakv6 and others: did you get a chance to look at the quarterly financials/presentation. Would be helpful to get your thoughts.

I think the debt could be for dividend payment. They should not have payed the dividend at the first place, companies growing at this rate need all the possible cash to grow and that is where the management focus should be.

I do not think this small debt is any cause of worry. They can bring back some cash from US subsidiary and square it off.

Trade receivable has to be seen as percentage of revenue. Absolute numbers are not useful.

Also assuming Trade receivable remain at this level. Trade receivable as percentage of revenue are 24% which is in line with historical average of the company.

Dividend of ~ Rs. 3 Cr seems to have been paid through additional short term borrowings.

So, raising additional long term debt of Rs. 24 Cr to fund acquisition by US subsidiary while showing Rs. 120 Cr Cash on the books of US subsidiary looks alarming to me as it raises doubts over their true cash position in the subsidiaries. (agree that they can bring it back from US subsidiary and pay off)

Also, I was talking about the trade receivables of the standalone entity (although small):

I suggest we should not jump to the conclusion that debt has been raised to fund the acquisition. Instead write to Investor relations, I think they will respond. They may need to raise cash in India for variety of reasons like office expenses etc. since they did not brought any cash from US subsidiary to India.

Also, no point looking at this company on standalone basis because most of their business is in US.

This is a good answer Gaurav Agarwal… If there is anything not looking OK,

investors should first write to IR dept and seek answers…and if they do

not receive answers or they are not convinced with the answers, they are

free to claim whatever about the company… Many a times i have found in

concalls, when the questions raised in several forums are asked to the

management, they have a very convincing answer to why such a thing has

happened…

Had written to IR already - hopefully they will respond soon.

Also, while not jumping to the conclusion, Q2-2018 standalone & consol BS both are showing an incremental long term borrowing of ~Rs. 24 Cr of (liability side) and only standalone BS is showing incremental loans (asset side) of ~Rs. 25 Cr over last half yearly financials.

so the Indian entity indeed seems to have lent Rs. 25 Cr to one/more subsidiaries in H1-2018.

Also, since Cornerstone acquisition happened in May-2017, it’s highly likely that the borrowed money was used by US subsidiary for cash payout to cornerstone’s owners on closing of the transaction.

US President Donald Trump’s administration is set to propose revoking a rule that makes spouses of thousands of H1-B visa holders eligible to work while in the US, potentially complicating a major driver of technology jobs, the media reported.

At market open today (22nd Jan 2017) close to 7 lakh shares of 8K Miles got traded today at price of 755 odd levels. Looks like bulk deal of some sort. Any information regarding the same will be appreciated.

Would it be possible for you to share the source which gives real-time bulk deal data. I notice you were able to figure out the bulk deal amount and price early in the morning. As far as I know, these data points get updated on NSE and BSE after 5 pm - so would be helpful to know if there is a separate source (paid/unpaid) which provides these real time updates of bulk deal data.

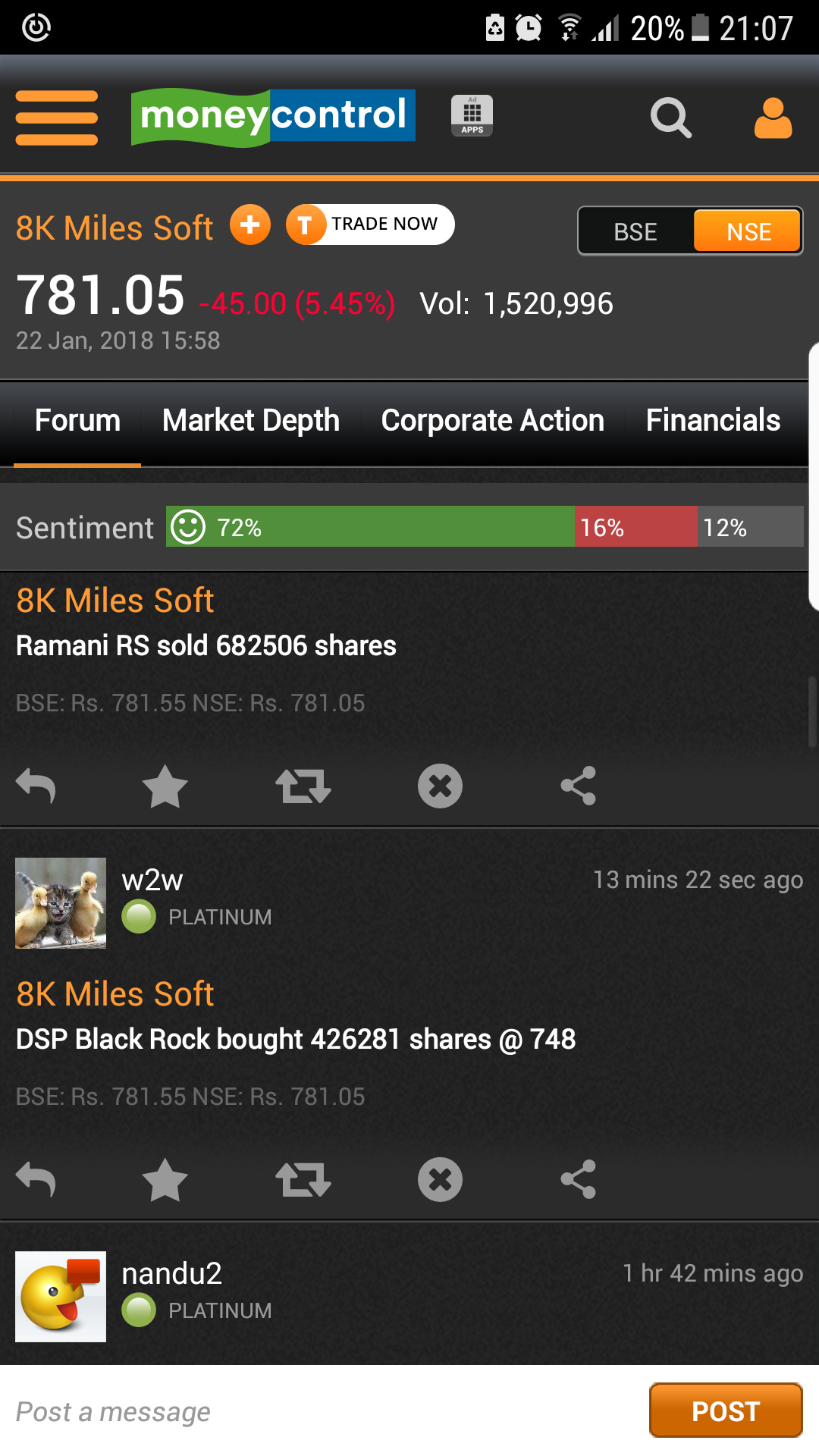

Also, looks like the promoter RS Ramani has sold about 60% of his holdings (6.8 lakh shares out of a total of 11.6 lakhs)

When I saw the sharp drop in stock price immediately after market open, I went to Google Finance and saw “tall” volume bar at 9:20am. Volumes were normal before and after that tall bar, which told me that this was not systematic selling but rather a block deal of some sort. And that is the reason my estimates were a bit off from actual numbers, as I just did a quick ball park calculation of stock price and volume.

DSP blackrock fund increased holding through block deal.Also hearing one big investor who bought Rain Industries and Emkay at its early stage entered in 8k miles.Good days to come

Wonder if promoter cum CFO of the company (R S Ramani) is aware of the coming good days. He was the one who sold his stake to DSP blackrock (and most probably the other big investor as well).

He is consistently reducing his stake:

RS Ramani

Mar-17

Jun-17

Sep-17

Dec-17

Jan-18

# of Shares

2,157,506

1,157,506

1,157,506

1,157,506

475,000

# of shares sold

1,000,000

682,506

Worth of Shares (approx)

Rs. 60 Cr

Rs. 51 Cr

Not really sure if this should be interpreted as a good news.

May be that’s a good enough reason.

But concern is, why would a CFO sell 70% of his shareholding in less than a year if he is bullish on company’s prospects. Adding to this, another promoter MV Bhaskar also sold out most of his stake in the last quarter, Dec-2017 (agree that he was probably promoter only on paper).

So technically, two out of three promoters(read “persons having best knowledge about company’s prospects”) have sold out most of their shareholding in the last one year.