Nice to see Management not ignore or “push under the carpet” the news around Aspartame, they in-fact address it in their latest quarterly ppt. Wage hike in Sikkim plant by 64%!! Even Ahmedabad plant has increased wage by 24%! They mention some statutory wage rate increase! also some legal fees related to the now closed Sitarganj plant, dented profits. Nycil seems to be doing good while both Complan and Glucon-D have lost market share YoY.

3 Likes

How is their tax rate negative and what is SEZ ?

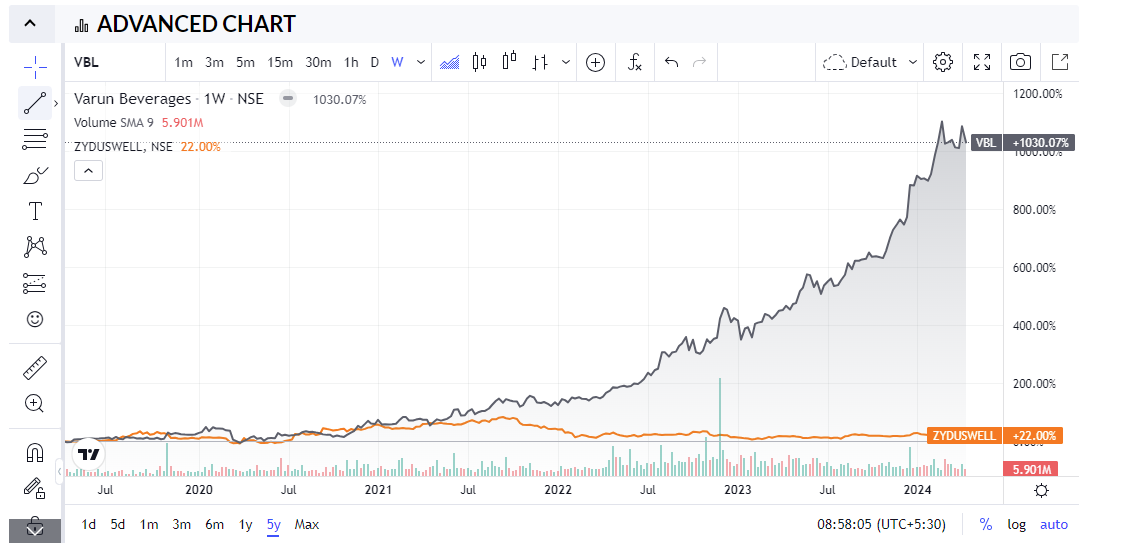

Their sales have gone 5 times since 2018 and profits have more than doubled in the same time period but the stock price hasn’t moved much.

Promoters and retailers both have started accumulating this stock as per tijori data but won’t the tax rate inevitably increase to 25% levels in near future leading to flat profit margins ?

What am I missing ?

2 Likes

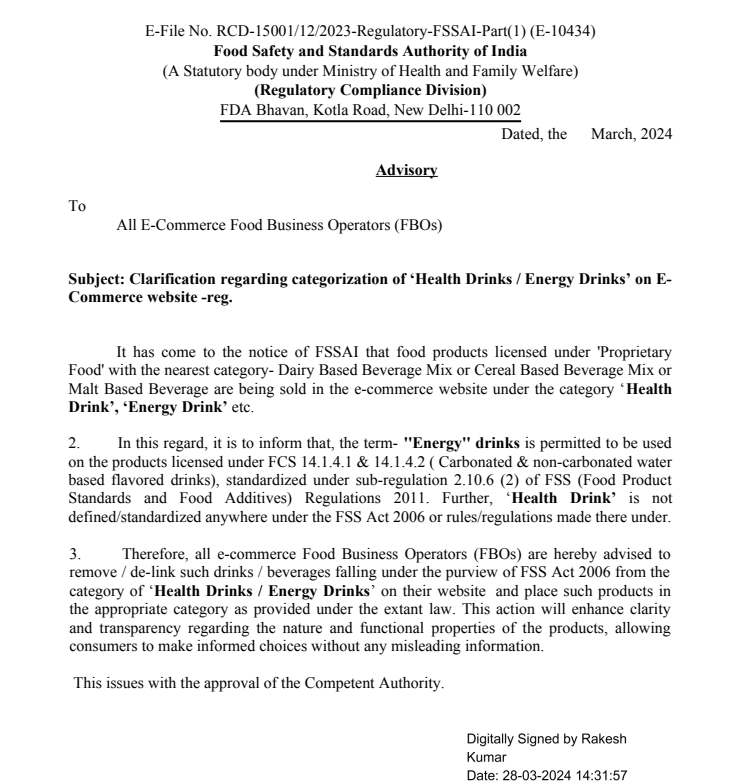

Energy drink Vs Health drink category slugfest

Varun Beverages (Sting - Energy Drink) Vs Zydus (Complan)

Zydus Wellness | Management Interview

- Management is committed to getting margin back to 17-18% in the next 2-3 years’

- Company is on the path to scale Rite Bite to ₹500 cr in the next few years

2 Likes

Zydus Wellness -

Q3 FY 25 results and concall highlights -

Q3 outcomes -

Revenues - 450 vs 400 cr, up 13 pc

Gross margins @ 47.7 vs 47.7 pc - flat YoY

EBITDA - 14.8 vs 12.7 cr ( margins @ 3.2 vs 3.1 pc )

PAT - 6.4 vs 0.3 cr

In Q3, Company acquired Naturell India ( healthy snacking company ) for a cash consideration of 390 cr. Q3 results include 1M revenues from Naturell India

9M FY 25 results -

Revenues - 1780 vs 1537 cr, up 16 pc

Gross Margins @ 51.3 vs 49 pc

EBITDA - 190 vs 146 cr, up 30 pc ( margins @ 10.6 vs 9.4 pc )

PAT - 175 vs 116 cr, up 50 pc

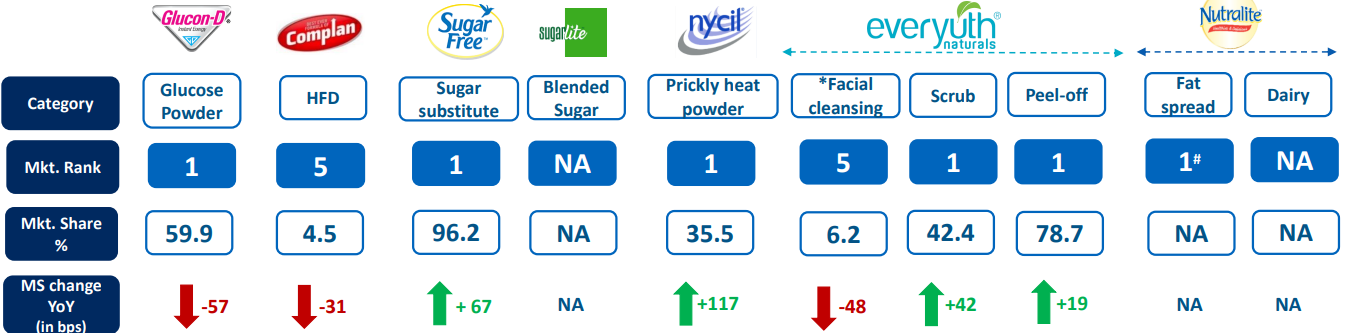

Company’s EverYouth Peel Offs and Scrubs have gained 2.24 and 3.18 pc mkt share respectively ( over last 2 yrs ). EverYouth continues to be ranked no 1 in peel offs and scrubs mkt. EverYouth is ranked no 5 in facial cleaning mkt

Nutralite brand of products have grown in double digits consecutively for last 4 yrs

Complan has gained aprox 0.7 pc mkt share over last 4 yrs ( Mkt Share @ 4.1 pc )

GluconD continues to be the mkt leader and the fastest growing player in its addressable mkt ( Mkt Share @ 59 pc )

Nycil has gained 4.55 pc mkt share in last 4 yrs

Sugar Free continues to be mkt leader in sugar substitutes with 95.4 pc mkt share. Sugar Free green continues to grow in double digits - consecutively for last 7 Qtrs

Launched Sugar Free D’Lite cookies in Indian Mkts in Q2. Seeing good consumer response

ImLite - Sugar ( Stevia + normal Sugar ) also continues to receive positive feedback from the mkt

Urban demand remained sluggish in Q3. Rural demand was much better

Q3 volume growth @ 5 pc

Naturell’s business is currently operating at break even EBITDA levels

Foods and Nutrition business - comprising of - Glucon D + SugarFree + Nutralite + Complan + ImLite + MaxProtien + RiteBite - grew by 9 pc in Q3 ( RiteBite and MaxProtien are Naturell India’s brands )

Personal care business comprising of EverYouth + Nycil grew strongly @ 50 pc YoY in Q3

Nutralite DoodhShakti launched Cheese in Q3

GMs held steady despite inflationary pressures

Company intends to reach 17 pc kind of EBITDA margins ( on an annualised basis ). Company intends to achieve the same within next 2 yrs. One obvious lever that the company has is to temper its advertisement spends which were elevated post the acquisition of Heinz’s brands (ie FY 22 onwards)

Guiding for a double digit topline growth for FY 26 with EBITDA growth > topline growth

Naturell India’s brands should be able to clock double digit EBITDA levels wef FY 26 ( as their brands get integrated and their distribution expands under Zydus Wellness )

Nutralite is doing well in fat spreads + Mayonese - in the HoReCa segments ( basically a B2B business ). Additionally, Nutralite is doing well in CSD channel

Launch of Amul Delicious is the proof that Nutralite is able to develop a descent mkt for fat spreads ( having lower fat content, higher veg oil content ) away from normal dairy fat spreads

5-7 yrs back, Nutralite was only a fat spreads brand. Over the years, company has also launched Mayonnaise, Chocolate spreads, Ghee and Butter under the Nutralite brand

SugarFree chocolates and cookies are another area where the company can capture large mkt share - if the category clicks

Complan is present in a low growth / mature mkt. It’s also a big brand for the company. Because of this, the overall growth of Foods and Nutrition business of the company is not able to grow at faster rates

Company is planning to take up price hikes in all categories where they r seeing RM inflation

About 10-11 pc of company’s revenues come from EComm + QuickComm spaces. These 2 channels are growing @ much faster rates

Company has shifted its focus from normal advertising channels to digital advertising channels

Disc: holding, biased, added recently, not SEBI registered, not a buy/sell recommendation

3 Likes

Zydus Wellness -

Q4 and FY 25 results and concall highlights -

Q4 outcomes -

Revenues - 910 vs 778 cr, up 17 pc ( driven by a volume growth of 17 pc )

Gross Margins @ 54.8 vs 54.4 pc

EBITDA - 190 vs 162 cr, up 17 pc ( margins @ 20.8 vs 20.7 pc )

PAT - 171 vs 150 cr, up 14.4 pc

Foods and Nutrition ( Complan + SugarFree + GluconD + ImLite + Nutralite + RiteBite + MaxProtien ) - grew by 15.4 pc

Personal Care ( Everyouth + Nycil ) - grew by 22.5 pc

FY 25 outcomes -

Revenues - 2691 vs 2315 cr, up 16 pc ( volume growth @ 12.4 pc )

Gross Margins @ 52.5 vs 50.8 pc

EBITDA - 380 vs 308 cr, up 23.2 pc ( margins @ 14 vs 13.2 pc )

PAT - 341 vs 262 cr, up 30 pc

Foods and nutrition grew by 12.4 pc

Personal care grew by 33.4 pc

Brand wise commentary -

Nycil - Mkt share @ 35.4 in Mar 25 vs 32.7 pc in Mar 21

Everyouth - continues to grow in double digits for last 5 yrs. Mkt share in Scrubs improved 420 bps in last 2 yrs, in Peel Offs improved by 163 bps in last 2 yrs. Launched sheet masks in FY 25 under the EverYouth brand. Current Mkt share -

Everyouth Scrubs - 48.5 pc

Everyouth Peel Offs - 77.7 pc

Everyouth Facewash - 7.7 pc

SugarFree - mkt share @ 95.9 pc. Sugar free green continues to grow in double digits in last 4 yrs. Company upgraded SugarFree Gold to Gold+ with changed formulation of - Sucralose + Chromium. Also launched SugarFree D’Lite cookies in domestic mkts

Glucon D - current mkt share @ 58.8 pc

Complan - has gained 56 bps of mkt share in last 3 yrs. Current mkt share @ 4 pc

Nutralite - growing in double digits in last 5 yrs led by a continuously expanding product basket

Organised trade now contributes to 21 pc of company sales vs 15 pc in Mar 21

Have recommended a stock split of 1:5, dividend of Rs 6 / share

Organic business ( ie Ex - RiteBite + MaxProtien ) grew in low double digits in Q4 - led by high single digit volume growth

Company aspires to move their annualised EBITDA margins into 16-18 pc band over next 3-4 yrs

Quick commerce is helping them reach new consumers with more premium products. Nutralite spreads and Complan are doing quite well in the Quick Commerce channel

RiteBite has been with Zydus for 4 months now. Have grown 50 pc YoY. Margins are in low single digits. Hop to build on these as operating leverage kicks in with scale

In Q4, onset of summer in South India was late. Despite that, company was able to grow in double digits. Western Parts of India have also seen delayed onset of summer wef late Q4, early Q1. Company is again aiming to clock double digit growth in Q1

Company paid 3X the sales of FY 24 while acquiring Naturell Pvt ltd ( owner of RiteBite and Max Protein bars). Company paid Rs 390 cr for the said acquisition. That means, these two brands clocked 130 cr of sales in FY 24

Have launched GluconD Activors in FY 25. Its a tetra pack based electrolyte drink

ImLite was launched in FY 23. Doing well. Company hopes that 20 pc of their sweeteners sale should eventually start coming from ImLite ( over medium to long term )

Company is spending 13 pc of sales on advertising and sales promotions !!! If they reduce this ( theoretically, say after 2-3 yrs ), it can lead to significant bump up in the EBITDA margins

5-7 yrs back, Nutralite was only a fat spreads brand. Over the years, company has also launched Mayonnaise, Chocolate spreads, Ghee and Butter under the Nutralite brand

Company’s tax liability is going to remain low ( in similar band as in FY 25 ) till FY 27

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

4 Likes