With above data, ROE is reduced substantially due to increase in assets, which is due to Heinz India acquasition.

Can anyone shed light on how they are going to improve the Asset Turns? Or is it going to be in this same range? Any guidance from management?

In general what strategy company uses to improve asset turns when it acquires another company?

Has anyone observed tax rates paid by the company? In screener it appears to be less around 10% compared to other FMCG companies 20 to 25%

Anyone knows the reason for the same

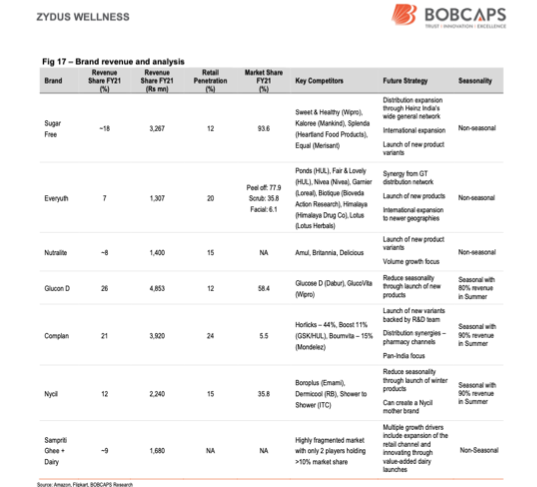

Taken from the concall in Feb . Mentions the market share of the various key products…

As per the MAT December ’21 report of Nielsen and IQVIA, Glucon-D has maintained its number one position with a market share of 58.1% in the glucose powder category.

Complan has a market share of 5.2% in the health food drink category.

Sugar Free has maintained its number one position with a market share of 96.0% in the sugar substitute category, which is an increase of 104 basis points over the same period last year.

Nycil has maintained its number one position with a market share of 34.0% in the prickly heat powder category.

Everyuth scrub has maintained its number one position with a market share of 39.2% in the facial scrub category, which is an increase of 448 basis points over the same period last year.

Everyuth peel off has maintained its number one position with the market share of 76.4% in the peel off category.

Everyuth brand is at number five with a market share of 6.5% in the overall facial cream segment as well

Results announced, ~6% revenue growth, PAT flat for Q4 YOY. Gross margin improvement of 264 basis points as per presentation, reduction of debt. Reduced APTID spends to partly compensate for higher COGs than last year.

This report was an excellent read, thanks for sharing. There were some points on Zydus which were never clear from prior investor presentations, and this report does an excellent job on bringing this out.

With complete credit to the original author, I would like to bring out an analysis on Page 8 of the report which helped me understand this company a lot better:-

Solid diversification between product categories now - though the acquisition Zydus has moved from a company very dependant on Sugar Free to a very healthy mix across high growth categories - Complan now contributes 21% of revenues, Glucon D is 26% and Nycil + Everyuth + Nutralite make another 27%

The business now has a strong level of seasonality involved with Complan, Nycil and Glucon D having a high percentage of revenues on the summer season

All categories still have scope for distribution expansion within the current network - be in the Heinz range in Zydus strong pharmacy distribution or the Zydus products in Heinz acquired General Trade network

I can’t understand how a health drink like Complan has seasonal sales. I find everyone in our circle consume health drinks (Complan, Horlicks, Bournvita, Ensure etc.) throughout the year.

Has anyone made an EPS projection taking into consideration the taxation change. As per my understanding FY24 EPS will be close to Rs.50.

Also had seen the previous article where management had guided 4500CR revenue by FY25 I believe, any chance of the company achieving this? Right now it seems very distant?

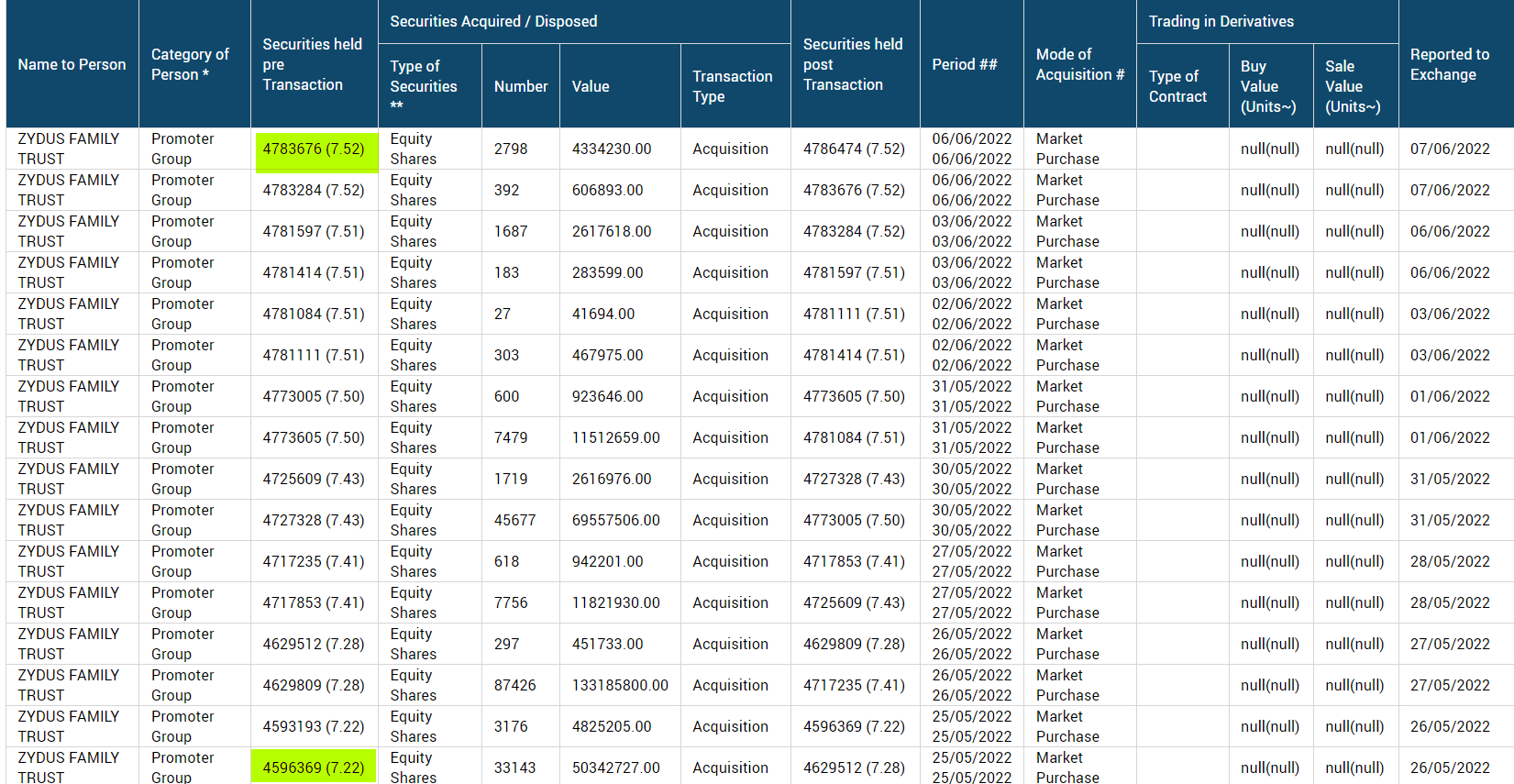

why is this stock languishing, they have more than few iconic brands? - agree with you, I am having a small position in this stock and planning to buy more if it dips further, like you feel this stock is indeed not performing as per what it holds. Market Cap/Sales its almost at covid levels - when they are having pricing power and monopoly products like Sugar Free. There was some small insider buying in september, lets see if further there is any insider buying - as that gives a bit of confidence to us minority shareholders.

Will you pick up this over Zydus life which owns it and what would be the rationale? We have many such situations where 2 companies are listed and one has majority stake in other…so whats the decision making process when you invest in one over the other? - Generally holding companies do well at fag end of bull market, when its time to switch to cash. Also, Zydus Life has US pharma exposure which is more uncertain and for me more complex to understand than selling Sugar Free, Nycil and Glucon D.

Actually, Zydus Life did a buyback when that stock was in the doldrums, if Zydus Wellness can do the same (considering same promoters), it will bring some upward trajectory to the stock.

Currently it is not paying tax, as per my understanding over the course of next 2 years they will exit from SEZ and be liable for full 25% corporate tax. I have not fully studied this but this is the reason I decided to hold back on my investment.

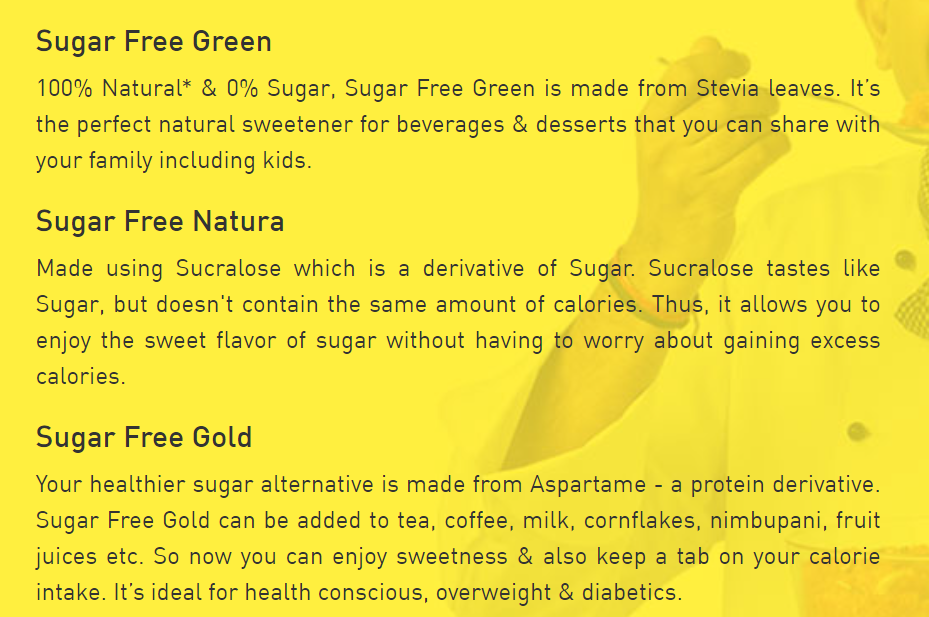

But yes, i have doubts on all these classes of artificial sweeteners and also so called zero calorie cholesterol ads, as they just induce you to consume more which is not a good thing…

Natural Sugar and Oil are both good if had in moderation…

Continued weakness on margins in Q4 (24% in Q4FY20, 22% in Q4FY21 and now 20% in FY22) and this WHO release in combination may have lead to the fall today!