Zuari Industries Ltd: A Multi-Segment Conglomerate with Value Unlocking Potential

Thesis

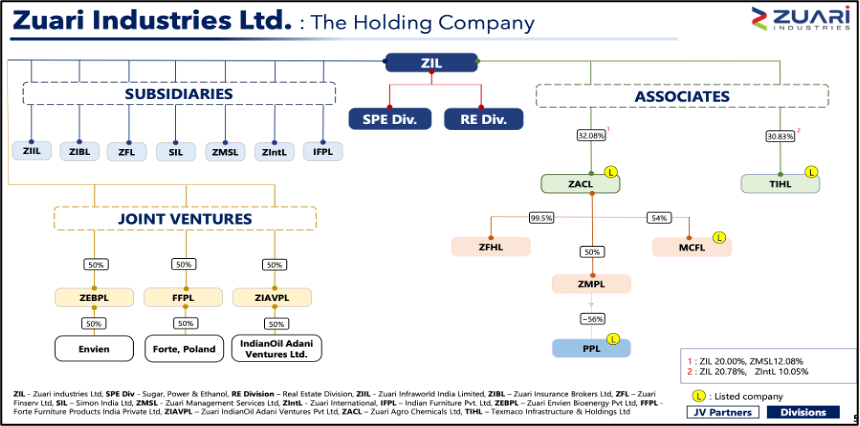

Zuari Industries Limited (ZIL) is the apex company of the Adventz Group, a diversified conglomerate with a legacy spanning close to six decades, founded by the visionary late Dr. K.K. Birla. Today, it is run by the Adventz Group, led by Saroj Kumar Poddar (Gillette India fame). The company functions through its divisions, wholly-owned subsidiaries, and strategic joint ventures. ZIL has been trading at a deep discount to its underlying quoted and unquoted investments. Historically, the stock has seen fluctuations, bouncing back from the 100-150 range to 400 and currently consolidating between 250-300, which is significantly below its intrinsic value. This situation presents a potential for substantial value unlocking, driven by strategic land divestments, real estate income, and potential share allotment or share swaps of listed associates like Texmaco and Zuari Agro Chemicals.

Zuari can become a 4X bet from the current prices.

Brands/Business of Zuari

Zuari Industries operates a diversified portfolio across several key sectors:

- Sugar, Power, and Ethanol (SPE) Division: This core division is based in Lakhimpur, Uttar Pradesh, with a sugarcane crushing capacity of 10,000 TCD, a 125 KLPD distillery (molasses/syrup based), and 22 MW of power export capability under a long-term PPA

- Real Estate: Primarily operated through its subsidiary, Zuari Infraworld India Limited (ZIIL), which undertakes property development. ZIL also holds substantial land banks in Goa. Key projects include Zuari Rainforest (Goa), Zuari Garden City (Mysore), and the premium St. Regis Financial Centre Road project (Dubai).

- Strategic Investments: ZIL holds significant investments in listed entities within the agrochemicals, infrastructure, and engineering sectors. These include Chambal Fertilisers & Chemicals Ltd (CFCL), Zuari Agro Chemicals Ltd (ZACL), Mangalore Chemicals & Fertilizers Ltd (MCFL), Paradeep Phosphates Ltd (PPL) (held through ZACL), Texmaco Infrastructure & Holdings Ltd (TIHL), and Texmaco Rail & Engineering Ltd (TREL).

- Engineering & Construction: Simon India Limited (SIL) provides engineering and construction services, particularly in the fertilizer, chemical, and oil & gas sectors.

- Financial Services: Zuari Finserv Ltd (ZFL) and Zuari Insurance Brokers Ltd (ZIBL) (wholly-owned subsidiary) operate in financial product distribution, stockbroking, and insurance broking.

- Management Services: Zuari Management Services Ltd (ZMSL) offers HR and business consultancy services to group companies.

- Trading: Zuari International Ltd (ZIntL) engages in trading activities for commodities like sugar, salt, and healthy snacks.

- Furniture: Indian Furniture Products Limited (IFPL) is involved in furniture. Forte Furniture Products India Private Limited (FFIPL) is a majority-owned subsidiary of Zuari Industries (acquired 50.85% stake in February 2025)

- Joint Ventures:

- Bioethanol: Zuari Envien Bioenergy Pvt Ltd (ZEBPL), a 50:50 JV with Envien International, Slovakia, is establishing a grain-based distillery.

- Oil Tanking Services: Zuari IndianOil Adani Ventures Pvt Ltd (ZIAVPL), a 50:50 JV with Adani Ventures, provides common user terminal services for petroleum products.

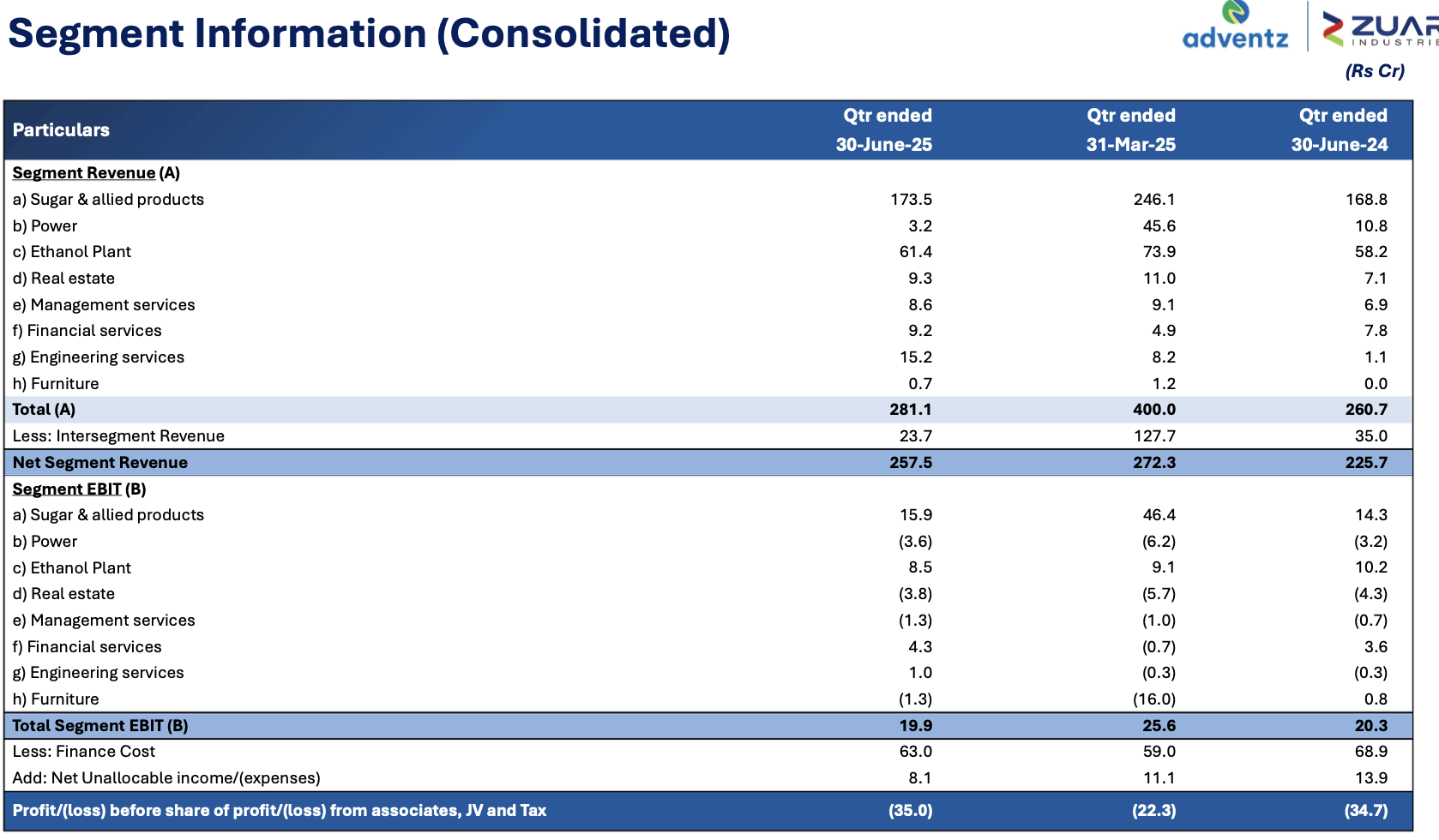

Segmental Performance of last few years

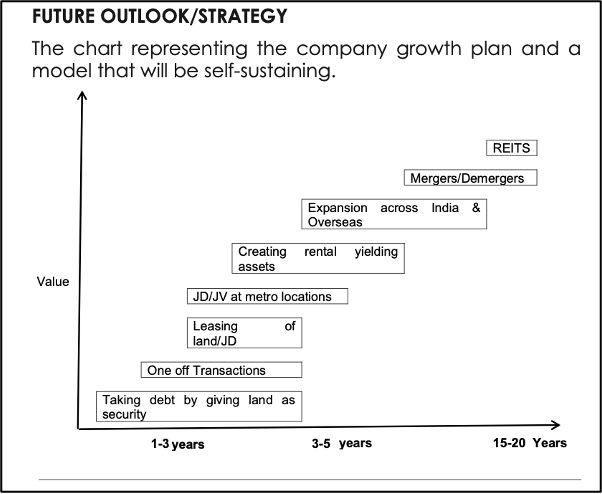

Long Term Strategy - “transform, nurture, and achieve sustainable growth.”

- Driving business and operational excellence in core segments like SPE.

- Deleveraging through strategic asset monetization.

- Investing in high-growth areas with discipline (e.g., Bioethanol, asset-light real estate).

- Leveraging digital technologies across businesses, e.g. Saksham

- Attracting, retaining, and nurturing high-quality talent.

My Attempt at Valuing the Sum of The Parts of Zuari Industries

Easiest Part: Value of Listed Entities as per Mcap of Mar 2025 – INR 4,701 Cr

Based on the company’s investor presentation, the value of quoted investments held by ZIL and its wholly-owned subsidiaries as of March 31, 2025, is indeed INR 4,701 crore. This includes significant holdings in Chambal Fertilizers & Chemicals Ltd (3,177 Cr), Texmaco Rail & Engineering Ltd (871 Cr), and Texmaco Infrastructure and Holdings Ltd (401 Cr)

Value of Core Business of Sugar, Power and Ethanol (SPE) – 425 Cr

This business is set for revival. For the first time, it has clocked an EBIT of INR 54.5 crore (Sugar), (19.8) crore (Power), and 27 crore (Ethanol) in FY25. Put together, an EBIT of 61.7 crore for the integrated SPE division. Accounting for a 20% cut due to sugar cyclicity, government regulations, and other external factors, I am assuming a normalized NOPAT of INR 38 crore. At RoCE just above WACC of 12 % should give a valuation of approximately INR 425 crore for the SPE division.

Operational Parameters for Conviction on SPE Turnaround:

- Highest ever cane crushed: 157 lakh quintals in FY25 (vs. 141 lakh quintals in FY24).

- Higher recovery: 10.61% in FY25 (vs. 10.41% in FY24) due to better cane quality and varietal replacement.

- Higher ethanol production: 3.4 crore liters in FY25 (vs. 2.7 crore liters in FY24), supported by 288 operating days (vs. 248 days in FY24). This has been the highest ever ethanol production.

- Higher power production: 1651.6 LU in FY25 (vs. 1291.3 LU in FY24), also due to higher operating days.

Valuation of the Real Estate Business

This is a crucial component, also the Catalyst in the thesis, primarily involving land banks in Goa, the St. Regis (premium project) in Dubai, and ongoing villa/apartment developments in Goa and Mysore.

- St. Regis Dubai Project: This flagship project is fully sold out and expected to be completed by January 2026. Management expects to repatriate approximately 750-800 crore of their investment and anticipates a profit of ~400 crore from this project. This profit is expected to be reflected in their books and repatriated before the end of FY26.

- Goa Land Parcels: Zuari Industries holds substantial land, precisely 381 acres, in Goa, earmarked for monetization.

- For FY26, I have assumed they will sell 81 acres @ 1.5 crore per acre, contributing to revenue and profit.

- For FY27, I have assumed they will sell 300 acres @ 1.5 crore per acre. This land parcel is going through some Circle Rate issues in Goa; however, these sales are projected to be pure profit as the lands were recorded at insignificant historical purchase prices.

- Other Developments (Goa and Mysore): Zuari Rainforest Phase 1 (95 units) in Goa is completed with Phase 2 underway. Mysore Garden City has developed 629 units, and Phase 4 (156 plotted units) is under construction (54% sold).

- FY26 & FY27 Profit Projections: Combining the St. Regis Dubai project, I project 1400-1500 crore revenue and ~INR 1000 crore of profit

All in all, for FY26 & FY27, approximately ~1000 crore of profit is anticipated from the real estate segment. Management has indicated a strategic pivot to an asset-light “development management (DM) model” for future real estate projects, where they earn fees for managing developments rather than investing in land.

Debt and Interest Cost:

Zuari Industries had a consolidated finance cost of 262.0 crore in FY25. My thesis assumes existing high debt of ~INR 2500 crore, which management aims to “par” (repay) as much as possible using real estate income.

Summary

As per my above tabletop exercise, the total Sum of the Parts Valuation would be:

- INR 4,701 crore (Quoted Investments)

- INR 425 crore (Core SPE Business)

- INR 1,000 crore (One-time profit from Real Estate anticipated in FY26 & FY27)

- Less ~INR 2,500 crore (Consolidated Debt)

This implies a ~3,600 crore valuation, compared to the current market capitalization of ~850 crore, suggesting a >4X opportunity with additional optionality from new consumer snack/food businesses, broking/insurance verticals, and future asset-light real estate ventures.

Risks

The primary caveat and risk are:-

- management speed and execution in relation to debt repayment, althought ZIL shares arent pledged but Chambal and Manglore ferti shares are pledged by management to back the debt

- improving the core business of Sugar, Power, and Ethanol, and divestment initiatives.

- While the company has shown strong operational excellence in SPE and moved towards an asset-light real estate model, the realization of land monetization in Goa faces regulatory uncertainties.

- The group also has a history of repeated investments in ventures which may not have yielded expected returns (e.g., furniture business impairment), which might be a concern for a prudent value investor seeking consistent RoCE and sound capital allocation practices. However, corporate governance, as per my limited study, does not appear to be an issue.

*Quoted value of investment flowing back to Investors through Dividends or Share Swap or spin off (preferably); group has given ~1 Rs per share dividend in the past; nor it has hinted of a buyback

Disc - Biased and Holding since 220 levels