Zota Health Care, incorporated in 2000, is a publicly listed pharmaceutical company engaged in manufacturing, marketing, and exporting pharmaceutical, ayurvedic, nutraceutical, and over-the-counter (OTC) products.

Business Model Analysis & Key Growth Drivers

youtube.com/watch?v=JjzzR6FYzb0

The company operates across four main business verticals, with Davaindia dominating the revenue mix in Q1 FY26:

-

Davaindia (73% of Q1 FY26 Revenue): This is India’s largest private-sector generic pharmacy retail chain, launched in 2017. The core model revolves around providing quality generic medicines at significantly affordable prices, typically offering 30% to 90% savings compared to branded counterparts.

-

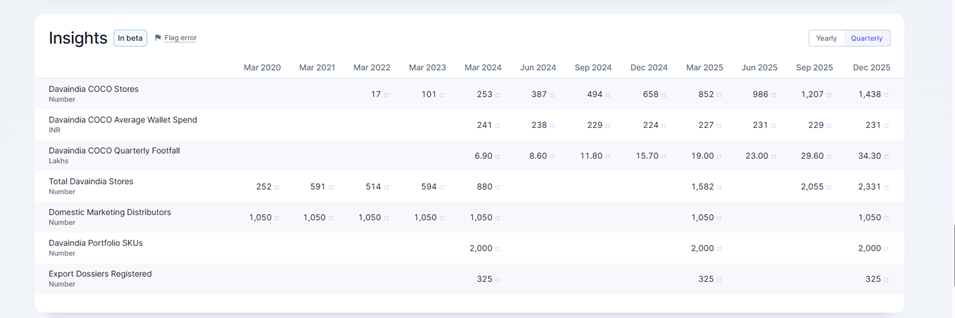

Operating Model: Davaindia operates through two formats: Company-Owned Company-Operated (COCO) stores (986 stores as of June 30, 2025) and Franchisee-Owned Franchisee-Operated (FOFO) stores (759 stores). The FOFO model is asset-light, contributing to scalability.

-

Product Focus: The chain focuses exclusively on private-label products across medicinal, OTC, ayurvedic, cosmetic, and nutraceutical categories, ensuring 100% exclusive sales. A key emphasis is placed on chronic therapies such as cardiac, diabetic, and thyroid, which typically lead to high retention rates.

-

-

Domestic Operations (15% of Q1 FY26 Revenue): This is the company’s oldest vertical. It markets over 4,000 products across major therapeutic segments, procuring finished dosage forms from WHO-GMP certified manufacturers and distributing them through 1,050+ distributors across India.

-

Exports (6% of Q1 FY26 Revenue): The company serves over 30 countries (mainly CIS, Latin America, Africa, and Asia) from its SEZ unit in Sachin, manufacturing 250+ formulations. They hold marketing authorizations (MAs) and registrations in these regions, with 325 product approvals received out of 586 dossiers filed.

-

Everyday Herbal Group (6% of Q1 FY26 Revenue): Zota holds a 56% stake in this group, which is licensed by the Khadi and Village Industrial Commission. This acquisition represents a strategic move toward backward integration and expands the portfolio in the OTC category.

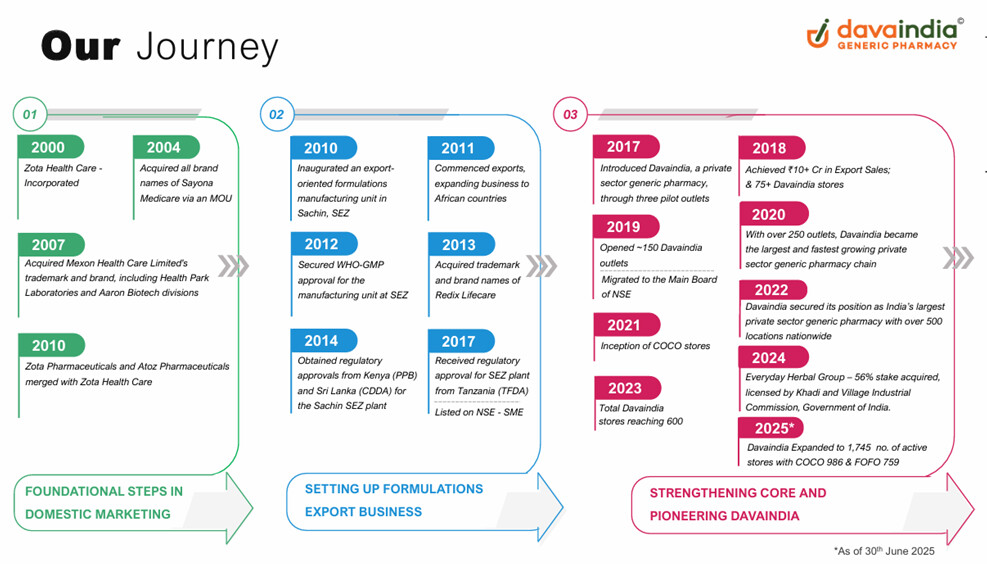

Journey:

Key Growth Drivers:

- Affordability Demand: The rising demand for affordable healthcare in India, where patients are turning to generic drugs as a cost-effective alternative, is a major tailwind. Generic medicines offer comparable efficacy and safety at a fraction of the cost, potentially saving patients from 60% to 90%. Example :

-

Store Network Expansion: Rapid expansion of the Davaindia network, reaching 1,745 stores by Q1 FY26. The COCO model growth is critical, as matured COCO stores (15+ months) show significantly higher average monthly sales (219% higher than stores <3 months).

-

High Customer Loyalty: Davaindia boasts an 80% repeat customer rate, demonstrating high customer satisfaction and loyalty driven by affordability and consistent quality.

-

Focus on Chronic Care: A high share (60% in Q1 FY26) of revenue comes from the chronic disease category, which signals high realization and retention rates crucial for long-term stability.

Competitor Landscape & Porter’s 5 Forces Analysis

The primary competitors fall into two categories:

-

Government-backed Generic Outlets, such as Jan Aushadhi, are identified as a key competitor backed by the government.

-

Private Players: Zota states that, apart from Jan Aushadhi, DavaIndia is the only player in 100% Private Label Generic medicine in India. Other private “generic pharmacies” often mix branded and generic products, diluting their pure generic focus.

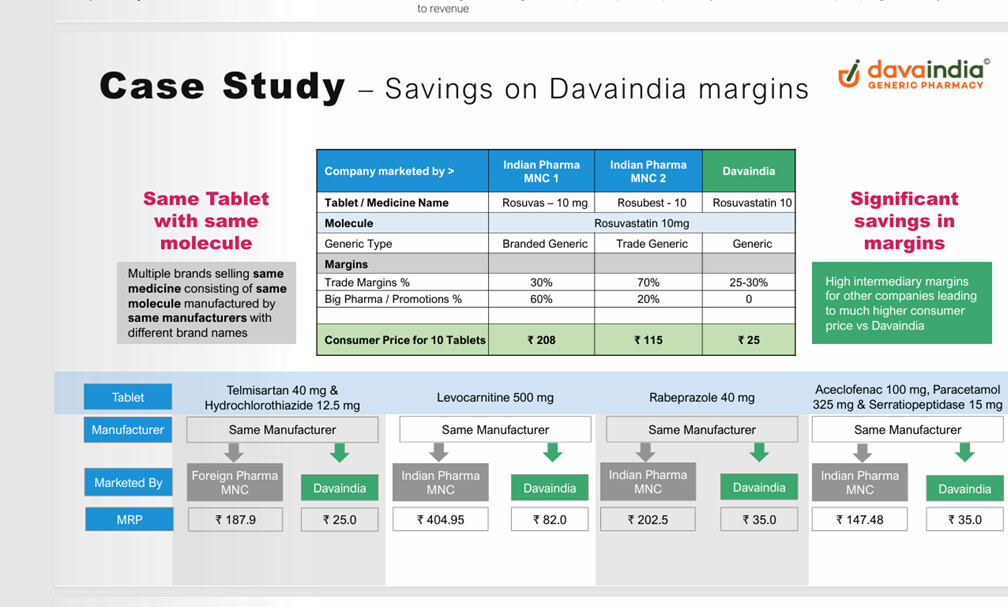

Zota’s model gains a competitive advantage by eliminating the traditional pharma supply chain (manufacturers, marketing companies, distributors, and retailers). This reduction in intermediaries allows DavaIndia to maintain modest margins of 25-30%, compared to up to ~90% margin incorporation by other companies and passing these benefits directly to customers.

Porter’s 5 Forces Analysis

-

Threat of New Entrants (Medium to High):

-

Barriers: Zota’s scale (1,745 stores) and integrated approach (private labeling, backward integration via Everyday Herbal Group) create barriers. The shift toward COCO stores, while enabling better control, requires significant capital investment.

-

Facilitators: The growing generic drugs market ($26.31 billion in 2024, expected 6.10% CAGR) and the rise of e-pharmacies could attract new players. Zota is addressing this by launching its own hyperlocal delivery app.

-

-

Bargaining Power of Suppliers (Medium to Low):

- Zota’s ability to procure finished dosage forms from multiple WHO-recognized domestic manufacturers and its manufacturing capability in SEZ for exports provides leverage. Furthermore, the 56% stake acquisition in Everyday Herbal Group strengthens its supply chain and moves toward backward integration.

-

Bargaining Power of Buyers (High, but Satisfied):

- Consumer price sensitivity in India is high, driving demand for affordable medicines. Zota proactively addresses this power by offering significant savings (30-90%). This strategy translates the high power of buyers into high customer loyalty (80% repeat customers).

-

Threat of Substitutes (Medium):

- Substitutes include traditional branded drugs and branded generics. However, DavaIndia mitigates this threat by ensuring that its private-label generic medicines are manufactured by the same producers as branded medicines, ensuring equivalent quality, while maintaining a massive price differential.

-

Rivalry Among Existing Competitors (High):

- The Indian pharmaceutical and retail market is highly competitive. Zota faces rivalry from traditional pharmacy chains, large branded pharma companies, and the governmental Jan Aushadhi program. Zota differentiates itself through its aggressive expansion of dedicated generic retail outlets and its unique 100% private-label strategy.

Profit Trend and Debt Profile

Profit Trend

The company is currently focused on an aggressive growth phase driven by store expansion.

-

Revenue Growth: Consolidated revenue increased by 84% year-on-year in Q1 FY26 (₹103.58 crores vs. ₹56.3 crores in Q1 FY25). Davaindia revenue grew 111% YoY.

-

EBITDA Turnaround: EBITDA has recently turned positive, moving from a loss of -₹124.0 lakhs in Q1 FY25 to a profit of ₹483.4 lakhs (4.7% margin) in Q1 FY26. Management noted that EBITDA has been consistently positive over the last two quarters (Q4 FY25 and Q1 FY26), reflecting scale benefits. The improved EBITDA is primarily driven by the maturation of older COCO stores.

-

PAT: Despite positive EBITDA, the company reported a Profit After Taxes (PAT) loss of -₹1,377.8 lakhs in Q1 FY26. This continued loss is attributable to high interest costs and significant depreciation, totalling ₹1,467.8 lakhs in Q1 FY26.

-

Path to PAT Breakeven: Management estimates that a meaningful shift toward strong profitability and expected breakeven will occur once approximately 600 to 700 stores enter the mature bracket (18 to 36 months old), a transition anticipated to take another 12 to 18 months.

Debt Profile

-

Borrowings: Consolidated Borrowings increased from ₹95 crores in March 2024 to ₹140 crores in March 2025.

-

Interest Cost: Interest expenses are substantial, totalling ₹323.9 lakhs (₹3.24 crores) in Q1 FY26 and ₹1,078.3 lakhs (₹10.78 crores) for the full FY25.

-

Debt Ratios: A potential concern highlighted by machine-generated pros/cons is that the company has a low interest coverage ratio.

Growth Strategy

Zota’s growth strategy centres on expanding its retail network rapidly and enhancing store economics while ensuring backward integration:

- Aggressive Store Rollout: The company is currently focused on aggressively scaling up its network, targeting the opening of approximately 800 COCO stores and 150-200 FOFO stores within FY26.

3 Digital Integration (Hyperlocal): Zota launched the Davaindia B2C Online Portal and mobile app to implement a hyperlocal model, where COCO retail outlets serve as fulfilment centres for swift order processing and delivery. This online integration is expected to enhance SCM efficiency.

4 Brand Visibility: To further boost brand visibility and footfall, Zota appointed renowned actor and entrepreneur Mr. Suniel Shetty as its Brand Ambassador during Q1 FY26.

5 Leveraging Maturity Curve: The financial strategy relies on the maturation of the large network of younger stores. Average monthly sales for stores ramp up significantly, increasing from ₹76,000 in Month 1 to ₹2,25,000 by Month 10. The expectation is that the strong performance of mature stores will exponentially multiply revenue as the young store network matures.

Risks:

a) Profitability Risk- Despite strong revenue growth, PAT is still negative, loss of ~₹13.7 Cr in Q1 FY26. EBITDA just turned positive recently

b) Dependence on Store Maturity Curve: The business is in the growth phase, meaning the company is focusing on rapid expansion, opening more stores. I am still finding out how the mature stores perform compared with the new store and how long it takes the new store to be profitable. The longer the time, the more the risk of turning the stir into a profitable one.

My View:

In my view, Zota Healthcare looks like a structural story for the next three to five years atleast. Basically the unorganized small medical stores are being converted into more organized space and this trend could be a multiyear trend where in companies like jota are eliminating the middleman and buying the medicines in bulk ohh some alternate generic solutions be the same impact additionally the business model looks like really easy to scale with a combination of company owned & company (CoCO) operated and franchise operated model and that makes the business asset light and passing maximum benefits to end customer. This will involve consolidating unorganised small medical stores/shops into an organised generic chain that provides cost advantages to end customers. The more Indian people are aware of substitution, the better the prospects of the ZOTA story to thrive.

What to track: I have been holding ZOTA for the last two quarters. Further change in my allocation will depend on turning into profitable and the performance of mature stores, and the rate at which new stores are turning into profitable mature stores.

Ace investor Mukul Mahavir Agrawal holds approx 7% of the shares, which gives me more confidence in ideal validation.

Sources: https://www.zotahealthcare.com/, youtube.com/watch?v=JjzzR6FYzb0, Zota Health Care Ltd share price | About Zota Health Care | Key Insights - Screener

Disc: Not qualified to advise, so please do your own due diligence.

This is my first blog, so I expect views/suggestions from experts. Part of this is written by AI but proofread & validated by a human.