"Also it was the first and last time of me ordering something so expensive from Blinkit as their customer support is pathetic, have to chat with AI bots,” he added.

He went on to say that he called up the delivery agent and “literally cried while talking to him.” However, the delivery person despite having the pictures of the delivery was helpless, he added.

In the above interview, Deepak Shenoy talks about how qcom companies have “side deals” with some other companies for inventory. Can someone shed some light on this? Here’s what I could gather and correct me if I’m wrong in my understanding:

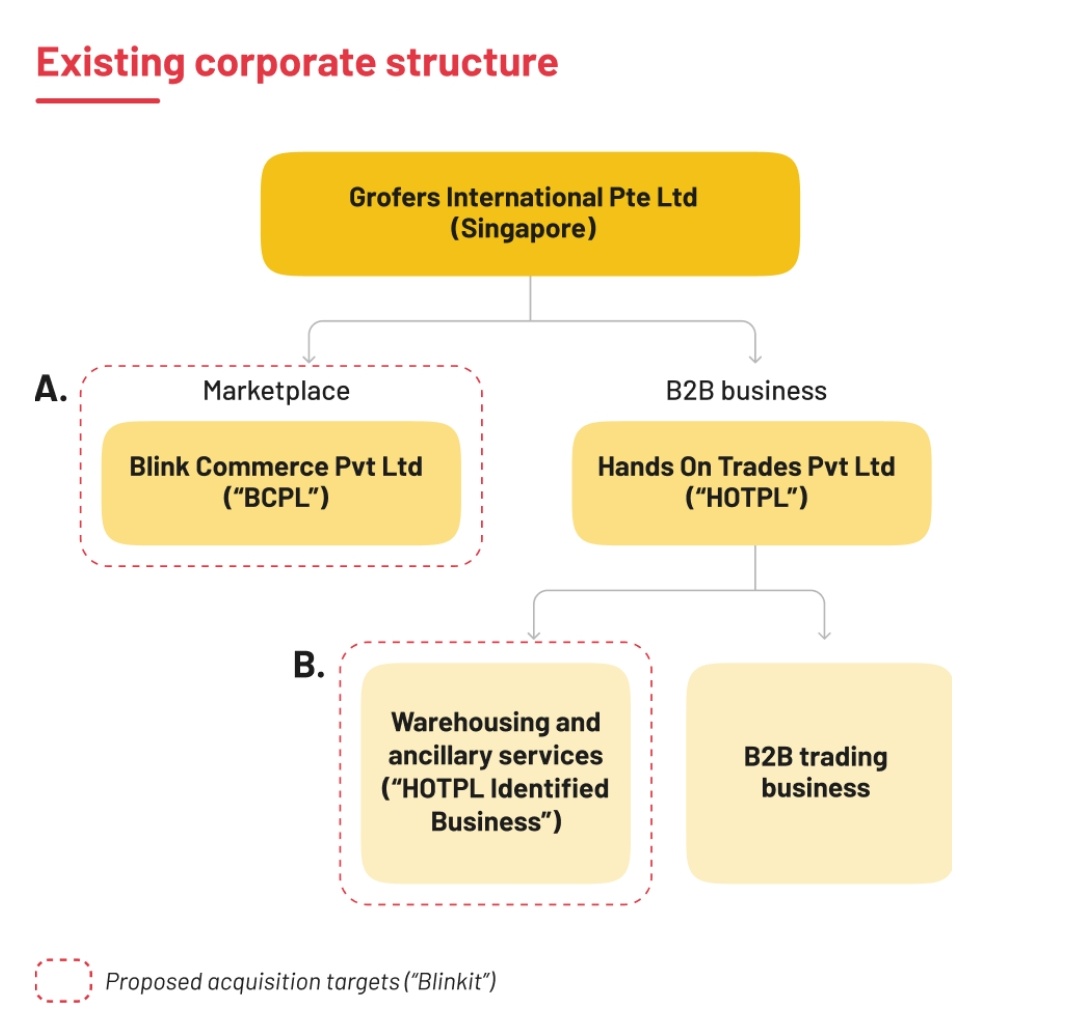

Zomato acquired Blink Commerce Pvt Ltd (aka Blinkit marketplace) in 2022. However, all the inventory is held on the books of a different company called Hands On Trades Pvt Ltd (HOTPL) which is not owned by Zomato. I think Zomato owns a small minority stake in HOTPL.

I concur that such an arrangement might be asking for regulatory trouble w.r.t. related party transactions and what not. Is this common in the retail industry?

@madhavojha pointed out a few days ago that the KMP of a few dominant vendors on Blinkit have connections with the KMP of Zomato. That might or might not be related to this “side deal” thing, but is equally interesting/concerning.

The revenue recognition from Blinkit in Zomato’s financial statements is only to the tune of take rates on the products sold to the end customers through the Blinkit marketplace. I think it’s similar for Swiggy Instamart too. But revenue recognition for Zepto and BigBasket seems to be money received from the customers for the products sold? Does this mean Zepto and BigBasket do not have such “side deals”?

I’m just trying to understand the supply chain and inventory side of things for Blinkit and retail companies in general.

Disclosure: Holding since before Blinkit was acquired and sold some around 280.

anybody noticing daily food delivery orders going down? I remember around June-July the average daily orders were 25-30 lakhs per day and lately they seem to be around 15 lakh orders per day (I usually end up ordering around 8-9pm, so that’s when I get their daily number from)

The valuation disparity between DoorDash and Zomato highlights a stark overvaluation of Zomato. DoorDash, the leader in the U.S. food delivery market, is valued at $72 billion. This is in the context of a U.S. per capita income of $82,000 and a GDP of $27.4 trillion.

In contrast, India’s Zomato is valued at $28 billion, despite operating in a market with a much lower per capita income of $2,700 and a GDP of $3.6 trillion. Given the significant differences in economic scale and consumer purchasing power between the two countries, Zomato’s valuation appears disproportionately high relative to DoorDash’s.

Are these investors oblivious to the basic math of market potential, or are they just hoping for a miracle? This kind of overvaluation defies common sense.

A bit of deep dive is required to understand Zomato. Zomato valuation is majorly driven by the massive potential TAM of Blinkit. So comparison of Zomato with DoorDash is like comparing Apples to Oranges.

Comparing Blinkit to Big Basket etc is also flawed since they are snatching business from Kirana stores and not from each other and all the organised players can actually win in such a scenario.

Disclosure - My top 3 holding with an average purchase price in double digits.

that would either mean the GDP per capita rises and/or the rider cost to also rise, which in my opinion would play out over a fairly longer period of time. The current unit economics exist because of a very cheap labor cost for the target consumer (stark difference between income levels of the Indian population).

Zomato’s share made a fresh all-time-high last week as it might be witnessing huge buying from foreign funds:

The company has plans to own the inventory at their quick commerce arm Blinkit, which they mentioned in their Q2 concall. For this to be allowed, they must bring down foreign ownership below 49% as per the Indian laws - confirmed by management.

As of Sep 2024, foreign ownership in the company stood at 52.53%. But the company in last 10 days has pursued 2 major corporate actions to bring it down:

QIP for domestic institutions: Company issued ~34 Crores fresh equity shares to domestic buyers and raised $1 Bn on 29th Nov 2024 which helped the company bring the foreign ownership to 50.23% as per BSE data.

Allotment of ESOPs to Foodie Bay Employees Trust: Company issued ~48 Crore equity shares under ESOPs Plans of 2018, 2021, 2022 and 2024 on 2nd Dec 2024 to its Trust which helped the company bring the foreign ownership down to 47.75% on that date. This happens because ESOP shares allotted to an Indian trust would add to the domestic ownership.

So while the ownership is already below 49%, the issue is, RBI has something known as ‘cut-off points’ for ceiling limits of foreign investments in Indian companies which they check on daily basis and is fixed at 2% lower than the actual ceiling i.e. 47% in case of Zomato. Once such ceiling is breached, all new trades by foreigners to buy pass through RBI’s approval. So incase they get the approval, foreign money buying Zomato’s share would immediately come to an halt as their ownership is already nearing 49%.

This is exactly what could be prompting multiple foreign fund houses to immediately buy the shares from the market - else they might not get a chance to do so in upcoming months.

And even if RBI’s capping doesn’t take place, decrease in foreign ownership % implies company might get higher weight in global index including MSCI & FTSE which would could again bring big foreign buying in the stock.

Incase you have another school of thoughts, shall be eager to known about the same!

This foriegn holding issue will always remain a overhang on Zomato since Zomato’s proprietor’s holding is very low. All shareholding remains with DII, FII and Individual investors and they will not take Buy/Sell call based on Zomato’s plan. They will simply look for returns/valuation etc.