The business is mainly divided into three different categories:

- Govt. Supply: They supply medicines to various state government institutions (Medical/health institutes). They prominently supply MP, Rajasthan, Gujarat, Telangana, Bihar, Haryana, etc.

- They also do 3rd party manufacturing i.e., contract manufacturing. They have clients like Micro Labs, Troicaa, etc.

- They sell their products in their brand name.

All the above categories are the various channels of sales. The actual products that they manufacture and supply under the categories mentioned above are

- ORS (Their Main product)

- Ointments (Medicinal Tube in layman’s terms)

- Syrups

- Capsules

The revenue share in the various categories mentioned in the first point is:

- Govt. - 50-55%

- 3rd Party - 20-25%

- Own brand - 20-25%

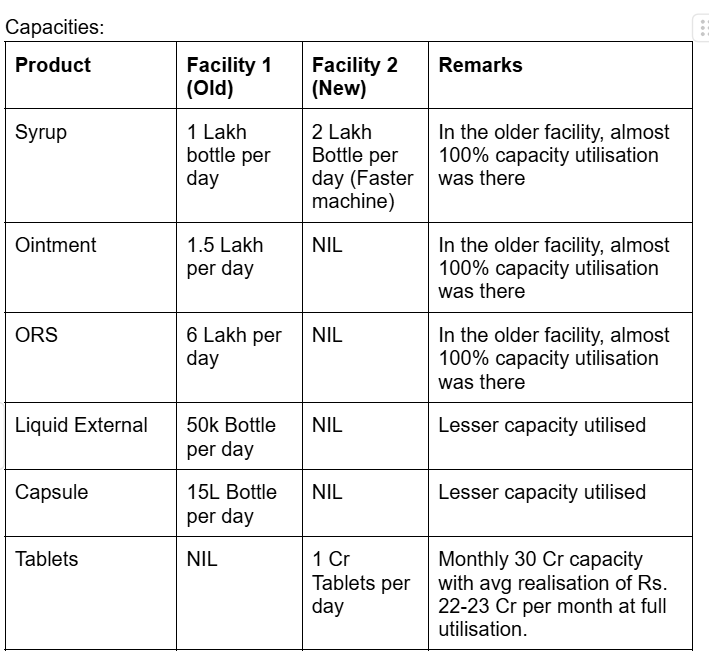

They have two manufacturing facilities and a third one is under progress which will get ready by December 2025/January 2026. Out of the two manufacturing facilities, one is old and the other is the latest manufacturing facility. The second facility started its commercial operations from December onwards. It took 2 months to start commercial production from October (Which was planned earlier). They are ramping up the capacities of the second facility gradually. Their capacities are as mentioned below:

Their 3rd manufacturing facility will be completely dedicated to Oncology. This facility will start contributing in FY27. It will get ready by late Q3 or by Q4 of FY26, and start contributing from FY27. They are planning to introduce injectables in that facility. So, they will have everything (Tablets, Injectables, Syrup, Ointment, Etc. to offer to clients). Oncology is a higher-margin business. So, FY27 is also expected to be a good story and good momentum for the company.

A listed company that is somewhat comparable to Zenith Drugs is Innova Captab Ltd.

A turnover of 150+ Cr is possible for FY25:

- From Facility 1 (Old): The old facility is running at almost full utilization levels. No volume growth is expected. So, they are going on a similar run rate of FY24. So, from this facility, a turnover of 150 Cr is expected

- The Tablet facility has the capacity to contribute 20 Cr in monthly revenues, but optimum utilization will be experienced from FY26. So, during this year, they will be able to manufacture 10 Cr, 15 Cr, and 20 Cr Tablets in Jan, Feb & March respectively (estimating nearly 30%/50%/60% utilization ramp up this year). Realization levels for each tablet are estimated at Rs. 0.75 per tablet, so by March, they can realize 33 Cr. But conservatively, since these are the initial few months, I am estimating 25 Cr to be achieved from Tablets alone.

- They will also be manufacturing Syrups in the New plant so, any production or development on that front may add up to our estimations.

At the minimum side, for this year, 150 Cr has been estimated.

For FY26, it looks like they can achieve a turnover of Rs. 260 Cr easily. The annual Revenue capacity from the tablet facility alone is Rs. 270 Cr (30 Cr Monthly Capacity x Rs. 0.75 per tablet x 12 Months). The entire new facility (2nd Facility) has the capacity to touch a revenue of 350 Cr. If we estimate 260 Cr, the revenue run rate is twice the current year’s run rate. This is due to the new facility started this year

Source for maximum potential: AGM Notes of company

It will be important to track the manufacturing of Tablets every month/Quarter, to get an idea about where they are heading.

Starting Exports is something where some development is expected.

For PAT margins, in FY25, they can manage an 8% PAT margin in line with last year’s trend. For the next year, i.e., for FY26, the PAT margins can see some operating leverage. It can be backed by stating that the exports will be higher margins, plus, the indirect cost (Marketing cost, accounts & HR salaries, Office expenditures, and other non-operational expenses will not add up due to added capacity (2nd Facility)) and thus, they will experience operating leverage. They will only incur a direct cost for generating revenues from the 2nd Facility, thus their margins would rise maybe by 2-3%.

Some Valuations matrics:

Company Trades at 160 Cr Market cap at expected Turnover & PAT of:

FY25E = 150 Cr & 12 Cr (Price to Sales & PE = 1.06 Times & 13.3 Times)

FY26E = 260 Cr & 26 Cr (Price to Sales & PE = 0.61 Times & 6.15 Times)

The comparable company i.e., Innova Captab has better margins, bigger capacities, and more manufacturing facilities & production. It will command a premium being a mainboard company to a SME but just see the valuations and find the difference.

LinkedIn says that they are hiring aggressively, the company’s promoters look like technocrats, and they are expanding very fast. These estimations do not count their third facility in the field of Oncology, which might start contributing in FY27. Oncology as a segment is much more margin accretive and has better export opportunities.

The company is worth tracking in the Pharma Industry.

Risks to be tracked:

-

Working Capital Requirement: They do a significant portion of their work with the Government. Thus, the challenge of high debtor days, stretching their working capital cycle, will remain unless they bring down that portion of the business against total revenues.

-

In line with the first point, the receivables in their books as of 31st March 2024 for more than 6 months were on the higher side at around 7 Cr out of a total of 67 Cr which stood as receivables.

-

They also do third-party manufacturing. Therefore, any negative remarks in the periodic audits that usually happen at their site might severely impact their revenues in the short term.

-

Any shortcoming in the ramping up of capacities can change the forecasts made. So, tracking the production levels becomes important in this case. The 2nd Facility is taping the Tablet space, and the majority of the FY26 revenues are expected from there so, tracking that will be crucial.

-

Liquidated Damages (part of other exp) - Generally these expenses are borne by the company when any delay in supply occurs from their side. This reflects an inefficient mechanism to handle the orders. Now, after they are listed, let’s see if they have improved on this.

Disclosure: Invested & Biased. Not a recommendation though. Everyone who is tracking this shall do his/her due diligence properly