In one con-call they mentioned acquisition of Span Across IT Solutions Private Limited, which again based on search on its key people, it looks like it is TaxSpanner (https://taxspanner.com/). Not sure about the intent of acquisition.

We should take a followup of all the partnerships, R&D (eg fleet loyalty Platform for Tirrent) and acquisitions

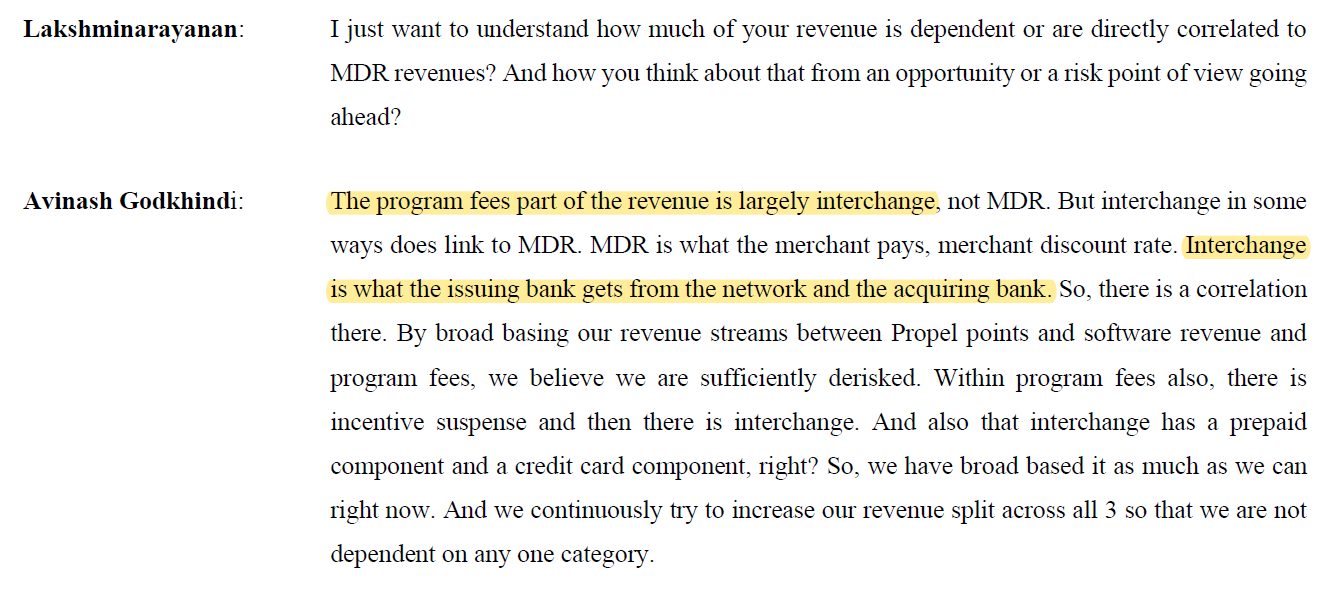

Hi, from what I understand your question is with respect to the programme fees earned by Zaggle and whether that they bear the CoF

I’m directly quoting the mgmt from this quarter concall on what they said wrt the programme fees

To your second question, what is the program fee and platform fee. Platform fees largely are

software fees that we charge as the SaaS fees. On the program fees, a very large component of

program fees is the interchange that is generated on every card swipe. It also includes some

incentives that we get from banks and networks like Visa, Rupay, Mastercard, etc., for the

volume of spends that we generate.

Since Zaggle is in the business of spend management they help the employer who is issuing the credit card to their employee for various kinds of spends be it food, travel, leisure etc the particular card issued by zaggle would help the employer to track the spends by each employee more intuitively and also catch any bogus transactions which is not the case with a non-zaggle credit card.

Earlier the management has clarified that they earn about 90% of the interchange that is generated on every card swipe.

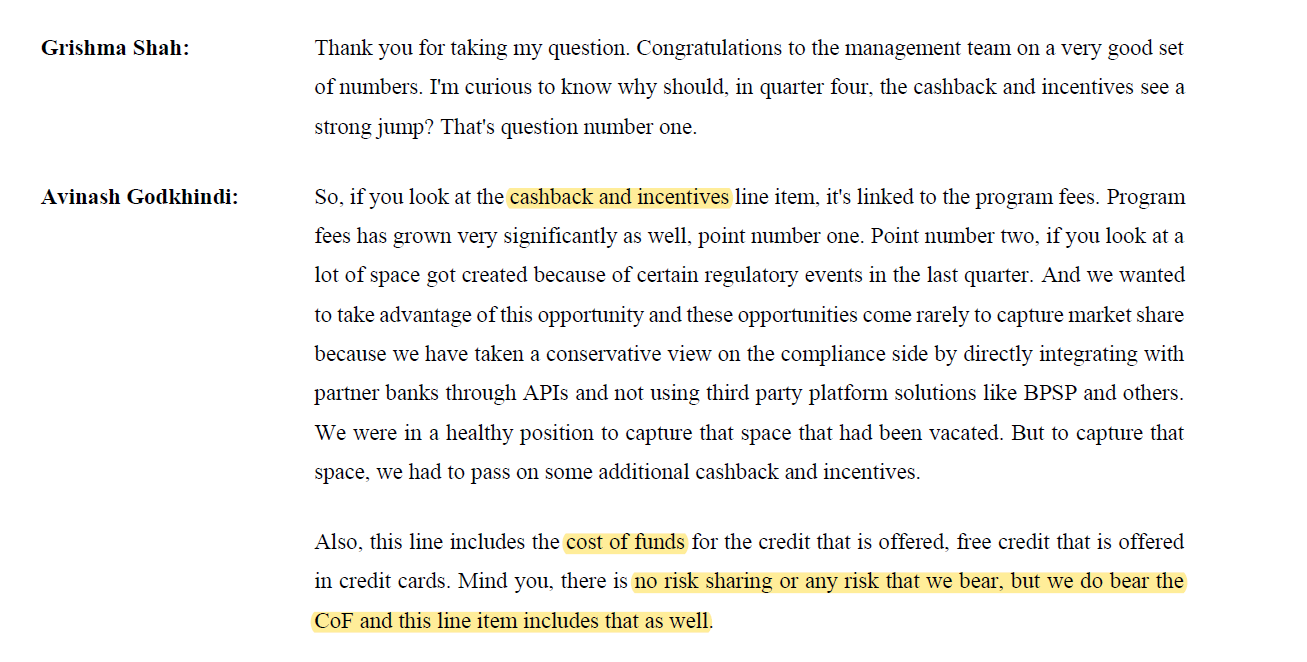

Now within this programme fees line they have a cashback & incentive line item as explained by mangement in the first screenshot that you have attached. This cashback line item is actually this prepaid component that they talked about earlier. So from what the management has said it is safe to deduce that zaggle bears the cost of these cashbacks and other incentives given to the employee on swiping of their cards, this encourages the card holder to spend more thus generating more programme fees for them.

Now, I don’t think this component is big enough to consider it as a NBFC so to say and since these cashbacks and incentives are I believe seasonal in nature and might as well be reduced in the future once the company has a bigger customer base.

I am following this company for some time. Kindly consider in this way.

You are a new employee joining in a MNC. Zaggle will provide a co branded card to you. At initially to encourage you to use that card frequently they will provide cashback and incentive kind of things. Once you regularly use this card they will stop the incentive. As of now company spending big chunk as incentives to increase the program fees revenue. Once this trend started to reverse we may see boost in margins. Hope it helps

Thanks for the reply Shankar, I watch your videos regularly and also read thru the article on Zaggle, helped re-assure some of my understanding of Zaggle’s business.

Thanks @VaibhavBhardwaj@hunter for inputs

While I agree with your points on what was explained by management regarding cashbacks and incentives.

My understanding is that there is a third comonent which is part of this line item, that is interest/cost of credit for the free credit given (usually 45 days) on credit cards

Personally to me, it doesnt look like pure Saas company. Their revenue from software is very marginal. It looks to me more like a payment processing company. I havent looked at how they recognise revenue of their different verticals. I prefer valuing it more like Route mobile or Twilio, transaction based revenue. So valuing it more like them may be more appropriate?

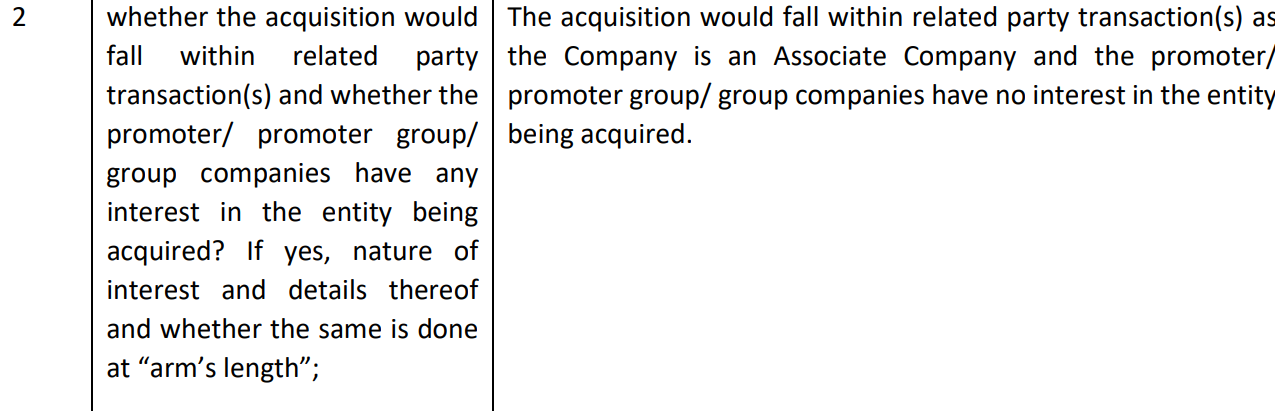

Paying 15.6 Cr for a 26% stake for a company with turnover of 17Cr. Valuation is about 4x. Seems about same valuation ratio of Zaggle, though we do not know about earnings of Mobileware.

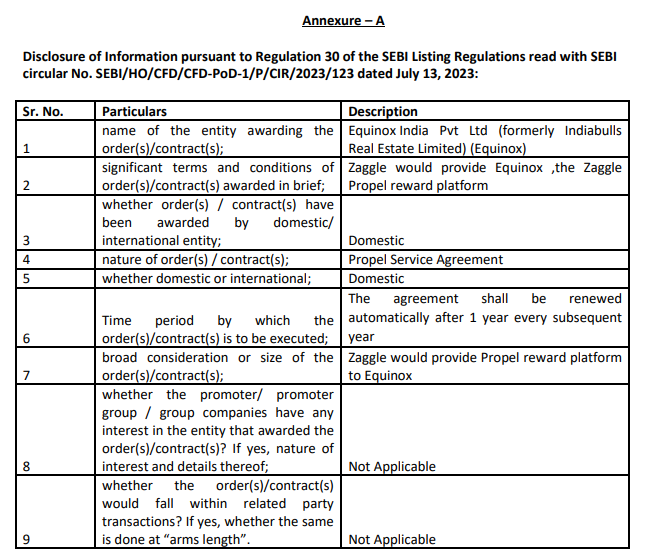

SpanAcross IT solutions

They are acquiring 98% stake for about Rs 30 Cr, for a company that has a turn over of Rs 4.73 Cr. Something doesn’t add up as it is an order of magnitude higher than expected… Please let me know if I am doing something wrong.

They’ve repeated in interviews that they’re tempted to up the guidance looking at the performance in the first 2 quarters, so it’s very likey that the 45% guidance is very conservative.

For a company with a size of 900 Cr topline, Zaggle’s 950 Crs Fund raise is a very big amount. It will be a key thing. They have hinted many times about their vision to enter the USA markets. I think they will try through an inorganic acquisition.

I think this is very conservative calculation, but I understand its always wise leave some room for margin of safety. I am expecting the management to formally up the growth guidance after Q2 result. I recall CEO in his recent interview has already indicated that they will up the growth guidance (from 45-55% to a higher number) for the full year. Usually only 35% of the full year revenue is contributed in H1 and since the H2 will have higher volumes, the realizations will be better as the revenue is the function of the take rate (for both Zoyer and co-branded credit card spending). Let’s see what the Q2 numbers look like.

Yeah, this came in as a surprise. The stock is already quite expensive and this QIP will mean the EPS will get further diluted by around 20%. Hopefully the management has some good inorganic plan up their sleeve, but we’ll have to wait and watch if this will go boom or bust.

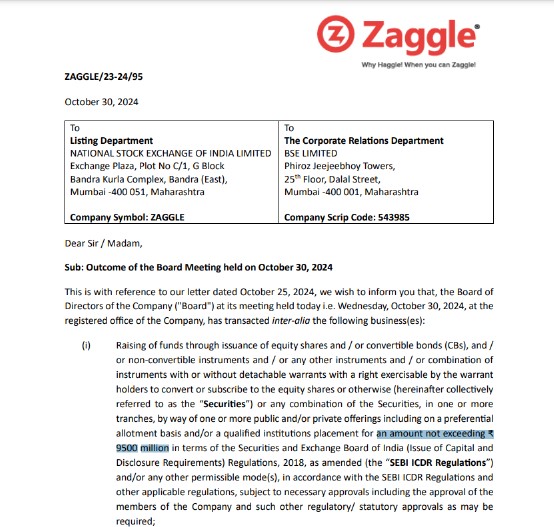

In line with our growth plans, we have taken approval from the board of directors for a fund raise of up to Rs. 9500 Mn. subject to shareholders approval.

Looking ahead, we are upping our guidance to 50-55% growth in our topline for FY 25. We are very confident of doubling our FY24 revenues in the next two years.”

Zaggle achieved its highest-ever quarterly revenue of INR 303 crores, reflecting 64% year-on-year (YoY) growth, exceeding its previously stated guidance.

Adjusted EBITDA for the quarter reached INR 29.5 crores, representing a 36% YoY growth.

PAT (Profit After Tax) more than doubled to INR 18.6 crores compared to INR 7.6 crores in the previous year.

Operational Performance

Zaggle’s focus on the SaaS product, “Zoer,” continues to be a key focus area, enabling the company to deeply integrate into its clients’ ecosystems.

Zoer has seen high acceptance, with a major use case emerging in petty cash expense management.

The company launched its first fleet solution for Torrent Gas, targeting the large addressable fleet solutions market in India.

Zaggle completed the strategic acquisition of Tax Banner, allowing the company to add comprehensive tax services to its product portfolio.

The company also received board approval for an investment in MobiKwik Technologies, a leading payment infrastructure development company in India.

Margin Guidance

Zaggle is committed to protecting and growing its margins over time.

Management believes the business has high operating leverage, which will naturally lead to margin expansion over time.

While a specific range was not provided, management indicated that they see significant potential for margin expansion in the coming years.

Future Prospects and Growth Strategy

Zaggle raised its FY25 top-line growth guidance to 50-55%.

The company is confident in doubling its FY24 revenues in the next two years.

Growth strategy includes focusing on strategic alliances and inorganic growth opportunities in the fintech sector.

Zaggle is actively looking to expand internationally, with a particular focus on the US market.

The company received board approval for a fundraise of up to INR 950 crores (subject to shareholder approval) to support its growth initiatives.

Key Risks and Competitive Intensity

Management noted that funding for the fintech industry has become tight, leading to some competitors abandoning growth plans and focusing on profitability, or even closing down. This could present both opportunities and challenges for Zaggle.

The global spend management market is expanding at 10.2% annually, while the Indian market is estimated to expand at a CAGR of 15.5%. This highlights the competitive nature of the industry and the need for Zaggle to continue innovating and delivering value to maintain its market position.

The regulatory landscape in India is constantly evolving. Changes in regulations could impact Zaggle’s business model and growth prospects. While the sources do not explicitly mention this, it is a general risk factor for companies operating in the financial services industry.

Management Actions and Acquisitions

Zaggle’s management team is actively seeking strategic alliances and inorganic growth opportunities, as evidenced by the acquisition of Tax Banner and investment in MobiKwik Technologies.

The company is focused on expanding its product portfolio and introducing new use cases to address the evolving needs of its customers.

Zaggle is also placing an emphasis on international expansion, particularly in the US market.

Industry Outlook

The global and Indian spend management markets are expected to grow at a healthy pace, driven by the increasing need for businesses to improve expense tracking, increase efficiency, improve compliance, enable decision-making, and boost productivity.

The evolving regulatory landscape in India is creating opportunities for companies like Zaggle that can provide innovative solutions to help businesses comply with new regulations.