I have been an anonymus reader of this great forum for few years now and learnign from other people here. My direct equity investing journey is fairly new but i have been debt investor for years . I have realised i have been too defensive given my age. I am in my high 30s. Now i seek defense with some offence in my investing journey i have decided to add direct equity to the mix. My portfolio size of investments in fairly large. So to preserve it is just as important as growing it.

I am followig a

35 (stocks) /

20 (precious metals) /

35 (debt) /

10 (cash equivalents) as of now like an All weather investing statergy.

I intend my equity investment to be concentrated ie less than 10 stocks at a time with 10-15 year holding period. I am not averse to playing commodity cycles. some thing like a 2000 to 2011 commodity cycle is always on my mind.

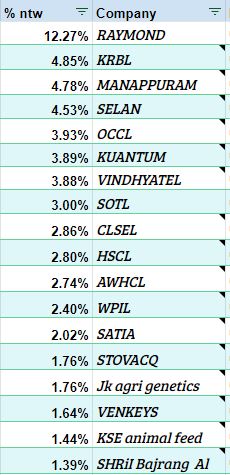

Holding : |Vedanta|39.90%| buy price: 110

pro: Deep value | growth | improving propects | reducing debt | logevity | prmoter aquisitions

con: Promotor deperation at group level debt but cyclical upturn seems to be fixing it | delisting risk |ITC|25.92%| buy price : 175

pro: optionality | potential unlocking of value | future growth propects | logevity

con: sin business | capital allocation efficiancy risk |ICICI loambard|7.29%| buy price: 1590

pro: brand| growth| secular growth in sector

con: competetion from new age players |Indus Tower|6.00%| buy: 236

pro: beaten down sector | consolidation | revival | gobally a sucessfull business | asset rich

con: uncertanity on one stakeholder survival due to AGR |Hathaway cable|5.45%| buy: 26

pro: turn around story | debt reduction | consolidation | beaten down sector

con: possibility of disruption |Gillet|4.84%| buy: : 5750

pro: stagnation might be presenting value | brand | improving profits

con: stagnation | it might be too big already | poor gowth propect visibility |Escorts|4.04%| buy: 1189

pro: growth | logevity | growing sector | brand

con: competetion from bigger players |Asain Granito|3.83%| buy: 177

pro: might be a deep value play

con: promoter group actions are questionable

i might kick this out shortly |Kinross Gold|2.84%| buy 6.5

pro: betting on gold price growth| deep value

con: mining is risky

As you see mejority of my assets are defensive debt/precious metals i thought my equity portion will be better served being concentrated and agressive.

Hi YSR, Thanks for sharing the details. Your portfolio is purely metals and consumer cyclic(~56%). You need to diversify your allocation towards other sectors as well - Like IT, Banking, Auto which will grown in next 4-5 years.

Metals and mining are value buy since they are cyclic in nature.Itc and gilette are not showing good fundamentals.You can check chemical,pharma,fmgc,nbfc and banking sector for good diversification

tq Ashu … my direct equity experience in only 3-4 years, i had mutual funds before. Even in those years i was just a passive watcher. Doing very little in direct equity. I go in after march crash big time and basically doubled my money and then i took the principle and diversified it .

what do you think is the right price to get into ICICI lombard? i did a simple DCF valuation assuming a growth rate of 18% for next 5 years and 10% from there and with an expected return of 14% it came out undervalued . I know DCF is not great way to value insurance, but i found it adequate. Any feedback is welcome.

Gillette: looks pricy but i thought the brand value it commands might be worth the premium. Plus i beleive there might be secular growth in home shavers in india who before went to barbers due to raising costs for such services.

tq Amrita

I have delibarately avoided finacials as i see them as being very opaque. After seeing yes bank fiasco and lehman brothers in usa. I dont feel i can really know what goes on inside a bank. But i am open to any sugesstion that i can look into in that space. Pharma and chemicals have had huge phenominal run. I could not find them as being value at these prices. I am open to any ideas there.

Changes to portfolio… views welcome…

I took some profit from vedanta,ITC,ICICI loambard and invested in the new businesses… and replaced some companies …

buy

company

allocation

reason

110

VEDL

25.17%

reducing debt in the goup, metals doing well with inflation so holding on, hope for more div to clear off parent group debt

175

ITC

13.78%

showing signs of improvement in fmcg margins , hotels business might do well along with agri and IT division

447

Raymond

13.01%

special situation of potential value unlocking and debt reduction due to raymond thane RE project, trading below sales

225

INDUSTOWER

10.28%

with vodafone overhang solved due to gov package looks like there is potential for improvement in cashflows going forward

368

AWHCL

6.52%

new position , only listed company in waste management

590

GULFOILLUB

6.35%

dispite slow auto secotor this company has been able to growth at a moderate pace compared to castrol with good roce

2076

RELIANCE

6.08%

potential value unlock, and retail segment looks to be growing fast, telecom arpu improvement

1288

ESCORTS

5.24%

fast growing company with good balance sheet , kubota JV might open up more potential, along with construction and railways equipemnt both having tailwinds due to potential gov spending…

698

Adaniports

2.77%

many year sof export stagnation seems to have boroken to the upside , port infrastructure might benefit from increased volumes, leverage can prove to be advantage in high inflation times

550

KSCL kavery seeds

2.44%

seed theme to beat inflation…many years of underperformace, raising cotton prices diversification into other hybrid seeds segments, buybacks …hoping for earning growth to pick up next year

679

Jk agri genetics

1.40%

cotton seed exports potential

starter position

135

GICRE

1.32%

seems market is not valuing the monopoly PSU reinsurance gaint , set to benefit from infrastructure projects and price hikes in insurance premiums

a starter position

78407

MRF

1.26%

auto sector revival play, new plant near auto makers in Dahej might give them advantage going forward

starter position

639

RAJESHEXPO

0.32%

largest gold refiner in world, expanding into jewellry retail

starter position

exited ;

asian granito | promoters look like crooks gillette | in hunt for some thing better with more growth potential Hathway cable | for some thing better