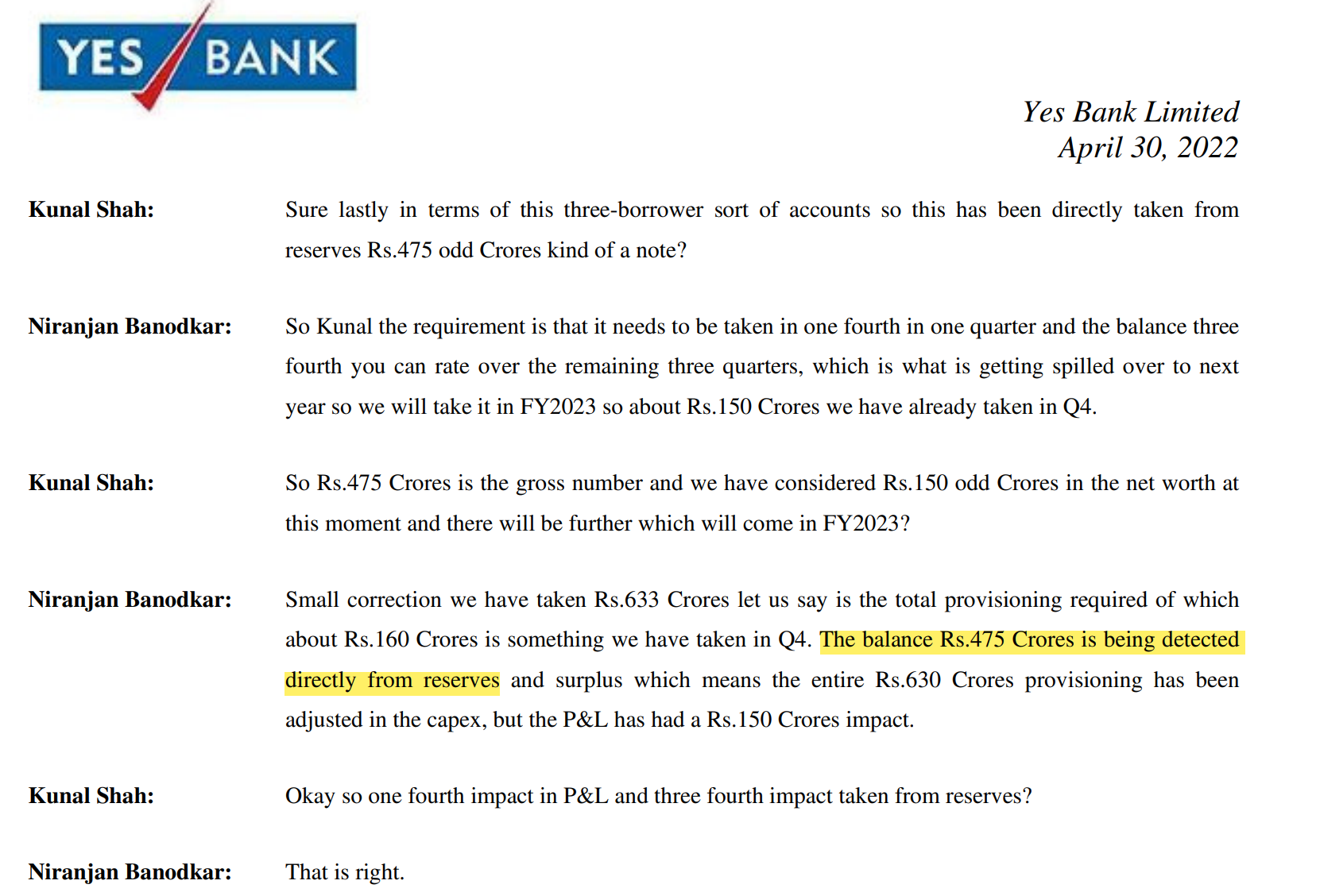

I was reading the Q4 con call and realized that Yes Bank has done equity write off 454cr. from reserves. @ISHWAR can you comment on this?

Thanks to @Worldlywiseinvestors and SOIC Course on Fraud Accounting

Hi myfirstmillions,

My name is Manhar, I am the one posting from ISHWAR account. So if you go through the previous post I( meaning ISHWAR) have already mentioned that it has done a provision after showing profit.

Now there are two ways you can see this thing.

1st way Q4 FY2022 was a loss of 110cr. Because they showed a profit of 365cr and did provision of 475cr from reserve after showing profit

2nd Yes they did a provision of 475cr which is bad but the way they did was smart. According to me their priority was showing profit which they did and meanwhile did provisioning as well. Now if you see there is no major issue in decreasing their BOOK value but it would have been an issue if profits were going to be reduced.

This year if the transferring of asset happens successfully then the ADD 2000-cr to book value. Then they are raising EQUITY which is again going to increase the reserve and surplus. They have 9200cr of DEFFERED TAX ASSET so provision for TAX adds to reserve and surplus again and at last next year NET PROFIT which I expect it to be 2200 to 2500cr again adds to book value. So I see lot of money coming into BOOKS so taking out 475cr is fine. But overall shareholder money has been reduce, which is BAD but the way they managed it good is what I am trying to emphasize.

Hi guys,

I have gone through the complete annual report and would like to point out my observation.

According to RBI macro stress test for credit risk the GNPA ratio of SCB may go up to 8.1% form 6.9% but if you see YESBANK is confident of having less slippage than FY2022. They had slippage of 5796cr in FY2022 and in FY2023 they have a target of less than 2% on entire advance. Next year their advance might be MAX at 210000cr so 2% of this comes out to be 4200cr.

There are two major reasons for this.

- They have a Retail and corporate mix of 60:40. So they have a granular loan book so, I don’t see any big default here. They have given a guidance of taking this MIX to 64:36. This is the reason they have 24000 employee because the more granular you do the more staff you need and this is also the reason last year they grew advances by 8% only. Because for disbursing 1000cr loan 1 corporate account is more than enough but you need 10000 to 100000 retail account to disburse same loan.

2 They are playing extremally safe. They are growing their advances slowly. Their 61 to 90 days overdue loan was at 4661cr on 31march 2021 and currently at 1264cr on 31march 2022.

My overall point here is last year they did provision of 1667cr from operational profit. this year I feel it is going to be not more than 1400cr from operational profit.

Their balance sheet is going to be above 3.4 lakh cr even after transferring its asset to ARC. So management target of 0.75% ROA comes out to be 2500cr NET profit. They had this target as 1% which they have reduced to 0.75%.

They have opened 52 branches last year and have an employee strength of 24346. They have Provision coverage of 72% but when i include technical write-off it is at 81%.

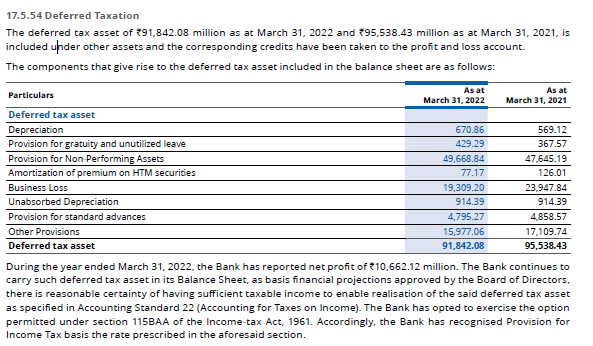

Now I saw an interesting thing. The bank considers its capital as 40397cr but on papers it is at 33730cr. This is because they have differed TAX asset of 9200cr.

The GUIDANCE FOR THIS YEAR IS

1 CASA more than 35%. They are going to achieve this. They are number 1 in UPI and NEFT. Now they don’t make a lot of money here but they get huge Customer DATA which can be converted into CASA. That is why despite having a bad image in market it grew its DEPOSIT by 21% last year.

2 Advance growth of 15%. 25% in retail and 10% in corporate. So this year I am expecting Advances to increase more than 20000cr which is going to Add close to 800 to 1000cr of NET INTREST income. I feel the cost of capital for this 20000cr is going to be low because they are raising equity that is why I took a NIM of 4% to 5%.

3 Recovery above 5000 cr in this cash recovery is going to be around 2500cr now this helps in setting off major part of slippages. and then 0.75% of ROA which is achievable so, EPS of around 0.85.

Overall I feel last year performance was better than expected and bank is on track in achieving all the targets set by management.

I have also posted an article on OPPORTUNITY IN BANKING which further increase my confidence in this stock because I feel it has huge sectoral tail winds. Opportunity in banking industary

Disclosure- Invested and is 85% of my portfolio

Based on the article below, can we say that banks with higher contingent liabilities would be more vulnerable in a volatile economic regime (now) ?

first rule of investing in not to put all eggs in one basket. and if you have 85% in yes bank !! then god help you… yes bank should be < 5% of anyone’s portfolio. it is very high risk with moderate returns. banks should not be analysed by same metrics like manufacturing companies. banks are the most levered entities as they borrow to lend keep only part of the borrowings as statutory deposits with RBI. CAR is 13 to 15% of banks - which means it is leverage is 6X - much higher than manufacturing and other companies.

Thankyou very much for your views.

My THINKING here is a bit different. I might be wrong but ready to learn from my mistake.

-

I am more focused on how much I loose than how much i make. I know when i have to exit if thing go wrong which according to me should not happen. I feel if you need to make big in stock market you need to make your own rules.

-

As time is passing my confidence in this counter is just increasing. This bank has litrealy been saved from being finished. It is backed by government of india. We have to see this bank in a little different way unlike others. I feel there is a lot of political angle here as well. I personally feel in banks measuring how much leveraged they are might not be appropriate because bank is build on back of liability.

-

My major reason to invest here is limited down side. IF YOU see dispite market fall it is still hovering at the same price

4 I see yesbank in a different way. To me it a 3.2l cr size bank ,6th largest private bank, backed by government, available at just 30000cr market cap. Major reason for lower market cap is huge NPA which is going to be cleared, huge loss,so last year was complete profit for yesbank and last heavy dilution which can be fixed with a reverse split.

I Feel by end of this financila year it should be touching 20 atleast once. I am no one to predict and i migh be wrong but i am pretty confident that it is not going to be below my average price. My aim in stock market is to just avoid losing money making will happen automatically if the first part is done properly.

@manhar Appreciate your conviction in the bank. It might suit you as you are still quite young (my assumption ![]() ) and the risk appetite could be high. Of course you stand to gain more reward if it plays out well.

) and the risk appetite could be high. Of course you stand to gain more reward if it plays out well.

Given that you had done in-depth research, I am very curious to understand your options / considerations on other investment opportunities before you went overweight on Yes Bank. Eg: how would you equate levering a position in ICICI equity comparing to buying plain Yes bank equity shares? Or, how about buying call options?

@Aarti What would make you change your mind about return prospects of Yes Bank? Shouldn’t the portfolio allocation be based on certain performance targets of Yes Bank?

For me, it is trend in GNPA, provisioning, contingent liabilities etc on one hand vs consumer growth, (digital) tech development, partnerships and other positive news on another. If above are taken care, would this still be considered moderate returns?

Or, is your view on financial sector as a whole to be within X% of one’s portfolio due to the inherent risks (we dont know what we dont know)?

Hi guys,

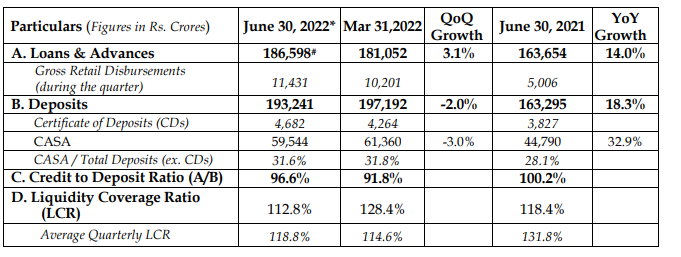

Yes bank Q1 update is out and to be very honest I am very happy with those updates.

If you see their advances have grown by 3.1% QoQ. If they continue such growth they can easily achieve 16 to 18% growth YoY. If they can do this growth without disturbing their mix it is going to be even better.

Now many of you might be thinking that the deposits have gone down and it is a bad sing. According to me this is their strategy. I have just gone through their balance sheet and found that they have close to 37000 cr at call and short notice and close to 17000cr with NABARD/ SIDBI/ NHB on account of shortfall in priority sector targets. This 54000 cr goes at repo rate which is 4.9% so this money is 20% of their asset and is a drain on bank. Secondly they are anticipating to raise money this year so they can build their deposit side slowly.

This year they will be trying to grow their advance and deposit by the same percentage unlike last year. Because they are not disbursing advances aggressively that is why I feel they don’t need deposits because these deposit increase their interest expense. They have a good amount of money available and also anticipating more to come so this year even if they grow their deposit by 10% is not going to be a problem.

I am going to share a broad level view on the profit I expecting this quarter.

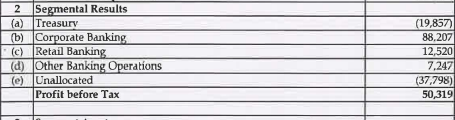

This is segment wise result of last quarter. If you see closely they did a loss of 200cr in treasury segment. So this quarter I am expecting this loss to be close to 400 to 500cr. Corporate segment can be 900 to 950cr. I am expecting retail segment to be close to 140 to 150cr. Retail segment can be a big surprise because they are doing very good in this segment from last few quarters ,this segment can be 200 to 250cr on the upside as well. Other banking operations close to 80cr.

All the figures I have given here can be completely wrong. I have gone very deep on each and every calculation which looks simple to read.

Now the last and most complicated is provisioning. I feel yes bank has an advantage here. The can manipulate their profit by showing provision according to their requirement. The reason they can do provisioning according to their requirement is that they have huge NPA which results into huge recovery every quarter. So the recovery which frees up their provisioning can be used according to their requirement.

https://economictimes.indiatimes.com/news/company/corporate-trends/carnival-cinemas-now-an-npa-yes-bank-to-recast-rs-800-crore-loan/articleshow/92582233

I am assuming provisioning to be at 350cr.

Overall expecting NET profit to be close to 200 to 250cr. This profit which I have projected is on the lower side. It can be way higher as well because of provisioning factor. Overall not expecting profit to be less than 200cr .

EDIT: Just wanted to mention one more thing this year I am expecting 2300 to 2500cr net profit from yes bank so 250cr in first quarter means close to 700cr in next 3 quarter. So I want to see a 400 to 450cr of net profit this quarter but as an Investor I cannot see it going below 200cr.

I am in the learning stage and all my figures can be wrong but if thing go the other way I am ready to learn and refine my analysis.

Thankyou

please have a look at brief financials submitted to exchanges for June quarter. on all metrics banks has underperformed QoQ. YoY is not correct in case of Yes bank.

2 major headwinds for the share price:

- locked in shares getting released in March 2023

- declining deposits

Key metrics to monitor - CASA ratio, operating profits and ROA.

i think that if bank has not been able to revive in 2 years under SBI then it cannot survive on its own. it needs new owners/ management or merged with another bank. there are many rumors about it being taken over by business house - if that happens then bank can revive !!

Hi maam,

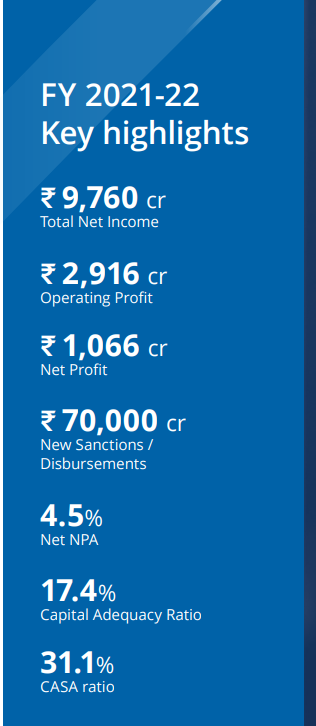

Actually I am in the learning stage and have a lot to learn about the banking industry but one think I can vouch for not as an investor but as a layman is Yes bank has done phenomenal in the last two years. I can say that Government of India and Prashanth Kumar/ Yes bank entire team has done extremely outstanding performance. To back the above statement let me put some numbers in place.

- We have to see that yes bank went under moratorium in 2020 and this bank was on a verge of being finished. Yes bank did a loss of 20000cr in 2 years and last year gave a net profit of 1000cr despite covid/ geopolitical situation/ Inflation.

2.I feel yesbank has almost stabilized and after this 1$ billion capital raise it creates a buffer and is completely stabilized will enter growth phase after this. Last 2 years they have done recovery and upgrades of 12000cr. They have changed their complete advance mix and made it granular. Their CASA ratio was at 23% and as of today is 31%. Last year their deposit have gone up by 21% this shows confidence of public on this bank.

-

There are close to 10 to 15 more parameters which I can highlight but I have highlighted the main one. This time their deposits have gone down , it is a bad sign but if the deposits go down again in the next quarter then there is need of cautioning not now. Inflation went up this time rates went up so there is some tightening moreover their deposits rates are not very attractive that is the reason the deposits have gone down but not to worry.

-

we have to see the positive development as well. Advances gone up by 3% now maam Yesbank is heavy on retails side and it is very difficult to disburse an amount of 11000cr to retail and MSME segment compared to corporate so this is an achievement in itself.

-

Most of the people don’t know clearly about the locking situation. How many shares are locked in? how many are there with retail and how many with instruction? what is roughly the average price of retail locked in shares? which institutions will be selling share? so maam my overall point here is most of the people are thinking that once the locked shares are release yes bank will go to 5rs

-

Yesbank share price will go down after lock in but what share price will yesbank be before lock in ? secondly is there any fundamental change in yes bank after lock in. Even if share price goes down just 1 good quarter and yes bank back to previous price.

7.One or two big FII entering yesbank. Entire NPA being transferred and a reverse split the entire story changes. The bank is completely different at that stage so we cannot rule out this situation.

If this quarter despite bond yield going up by 60bps if yes bank shows a NET profit of 350cr or more then I am 100% sure it is in the right direction and on track to achieve all it targets.

Just wanted to add one last thing please be aware of the fireworks in next two weeks on this counter.

Thankyou

Big news. There is no official confirmation yet but I feel that this time by September end they should be successful in transferring asset. Once asset transfer is done the entire game changes Immediately they will raise capital.

If you are interested in banking industry please go through this article. It will give you a fair idea as to how the trend is.

The bank has denied the news on ARC stake as speculative. The intimation to the stock exchanges can be accessed here

Hi.

Not only yes bank but any company will never accept to any news article reason being is companies have to intimate to SEBI first before doing any media interview. It was pretty sure they were going to deny this. Actually this news article is an indication that they have got approval or will be getting approval soon is what I feel. Now in a week or some days they are going to conduct the swiss auction. The swiss auction is roughly going to take 1 month and there after it might take another 1 month to transfer asset. I feel by September end books should be clean which is 2 and a half month from now. I might completely wrong not only me even it is difficult for the bank to project by when the asset transfer is likely to happen. we have to understand that this is the largest asset transfer in the country and it will take time.

Just see this news article of today. All these article are made to create excitement are generally before quarterly result. This is done to take the share price higher. Keeping all this aside I feel this time the transfer should happen.

most of the media reports are not correct so please do not post them. better to post when they do a press release or send to stock exchange.

media loves to write about yes bank as it is bein read by many many retail investors holding it - in fact it may be one of the stocks with largest retail holding - not sure though.

The Bank has reported to the exchanges on choosing JC Flowers bid as the base bid… Swiss Auction challenge process to follow

YES Bank_ARC Partner Selection_Intimation to Exchanges.pdf (177.7 KB)

Even after the much awaited announcement the stock was in red. managed to close at same price. it shows that the price is manipulated / controlled. There is no significant gain by creation of ARC it is just putting your bad assets in another company thats it - most of the benefits of recovery will go to the owner of ARC which is JC Flowers / Cerebrus.

Also when there were only two bidders then what is need for Swiss Challenge?? Doesn’t it indicate bad governance - just being projected as doing the right thing by calling in for Swiss Challenge.

I have already mentioned in my previous post about ARC. Let me just put across the broad level benifit from ARC.

- The entire management focus goes into banks growth rather that focusing on recovering asset.

2.Bank becomes cleaner. This helps them in raising money at a lower cost. Improves their image in the market and all the financial ratios improves.

3.Bank has played it very well. They are taking 20% stake in arc so any future recovery from any other bad asset will give bank straight away 20%.

- Their book value will go up by 80 paisa to 1rs. And any recovery made by Arc upto 12000cr yesbank pays only 15% of that recovery rest 85% is of yesbank.

We have to understand that they have just signed the term sheet the asset have not been transferred yet so how can we expect impact on share price. Every month there are 2 Arc news we cannot expect share price to go up because of those. They day asset gets transferred yesbank adds minimum 2 to 3 rs to form a new range according to me. I can be wrong by 1 or 2 months doest matter the more time yesbank trades at this level the faster it will go up.

Secondly maam all the articles i post here i always mention my take/ understanding on them. If you see my previous article i mentioned that they will be going for the swiss auction in one or two week and that is what exactly yesbank was trying too mention in AGM. So these articles i post after reading them 10 times but if you still feel it is misguiding then i won’t post them.

We have to understand the working of swiss auction. So yesbank approached 10 to 12 Arc in USA and selected 2 from them now there are many Arc in the entire world who are not aware of this. 50000cr is a dream amount for an Arc and there is nothing wrong in doing swiss auction. Actually this shows that yesbank is trying their best to get the best value if their asset instead of just finalizing and closing it. So maam anything above 10000cr adds to their book value so swiss makes lot of difference and is very important.

I have gone through Hdfc and federal bank result. They have done pretty good. Better than expected. So my expectation is 350cr or above from yes bank this quarter let’s see

Hi manhar

Your posts are really informative and I am impressed by your approach of calculated predictions. Please do keep sharing , as according to me there is lot of learning value here irrespective of one invests in yes bank or not.

Investment philosophy and approach is subjective and will always vary person to person. Nobody here is forcing to buy each other’s opinion, we are free to choose or reject whatever we like.

Coming to yes bank , can u please share your insights on there current book and cost of funds if possible , i would try and dig more.

Thanks in advance

Best

Divyansh

Disc : tracking posn