They are not going to sell them any time soon. I feel that DIsh tv board will be changed and they will have board member favoring yesbank. The main agenda of yesbank is to take the price of dish tv to higher level and sell it. Their current value in dish tv is around 750cr and i fell that they will try to sell it at least close to 1400 to 1600cr which will take some time. They also have a bright chance to get money for ADAG group. Reliance infra has won a case against delhi metro in supreme court against an amount 7000cr which the have still not got. once reliance infra gets this money yesbank would some how want its dues to be cleared as well. There is also a big opportunity to recover form VI as well .

3 Likes

1 Like

Still restructured book having significant portion…

Q4 adds more restructured loans…

Yes Bank Q4 results snapshot

-Net profit increased by 37.9% to 367 crores

-Net interest income (NII) has grown by 84.4% YoY which is a positive sign

-Gross NPA provisions was at 13.93% (consistently reducing for the past 3 quarters) which is another positive sign

-Provisions are down by 27.7% which is 271 crores, another positive sign

Disc: invested and biased

2 Likes

Most of the people might not know this that yesbank has done a provision after showing profit of around 475 cr from Reserve and surplus. This has reduced their reserve and surplus by 105cr. They have done this for 4 fraud accounts. In realty this quarter they have done a 100cr loss. But still i am very positive on this stock because of various other points. I would share all the major points on this company and my view for FY23.

3 Likes

Sir, are you aware of this update?

This article gets me very interested in Yes Bank, for the same reason as you like the bank. There is lot of margin for safety at this price point.

Source : bloomberg quint

2 Likes

This question was asked by someone in con all and while the ARC plan is on (target July 2022), it may not rescue NNPA ratio for the bank.

Can someone knowledgeable add more light to above ?

Hi,

Yes i am aware about the ARC. Even after transferring their bad asset around 27976cr they are going to be left with around 15255cr of bad asset which includes restructured advances as well. They also have around 16302 cr of write-off. So i always consider it as around 32000cr of bad asset. But their gross NPA and NET NPA will be close to 0 or 0.

Next year I am expecting it to give a profit before provision and tax of around 6000cr for fy22 it is 4000cr.They are expecting slippages to be less than 2% of overall advances which is going to be 1.81 lakh cr, it comes out to be 3600cr. Half of this slippage is going to be covered by cash recovery and rest half will need to be provisioned. So around 1800cr is going to be provision. PBT is going to be 4200cr.They have paid an average tax of 25% last year, the tax will be around 1050cr.The next profit comes out to be 3150cr. Now this is just a back of the envelope calculation. I am sill expecting a net profit of 2500cr on safer side. EPS of around 0.85 post dilution.

Now a bank just like other private bank with 0 NPA and EPS of 0.85 at least deserves a PE of 25. Price comes out to be 21 and after fy23 they are planning to do inorganic growth. I wont be surprised if this company reaches a MCAP of 3 lakh cr in next 10yrs.

Still there is a problem of heavy dilution. If yes bank does a REVERSE SPLIT of 1:10 the outstanding shares are going to come down to 300 cr only.

coming to ARC it will be very important to see the valuation at which the stressed asset are going to be transferred. Suppose it is 30% of the total asset then it comes out to be 8392cr. The 27976 cr stressed asset has a provision of 19771 cr , so the net uncovered asset is 8205cr if they get a valuation of 30% they end up making almost 200cr of net profit.

6 Likes

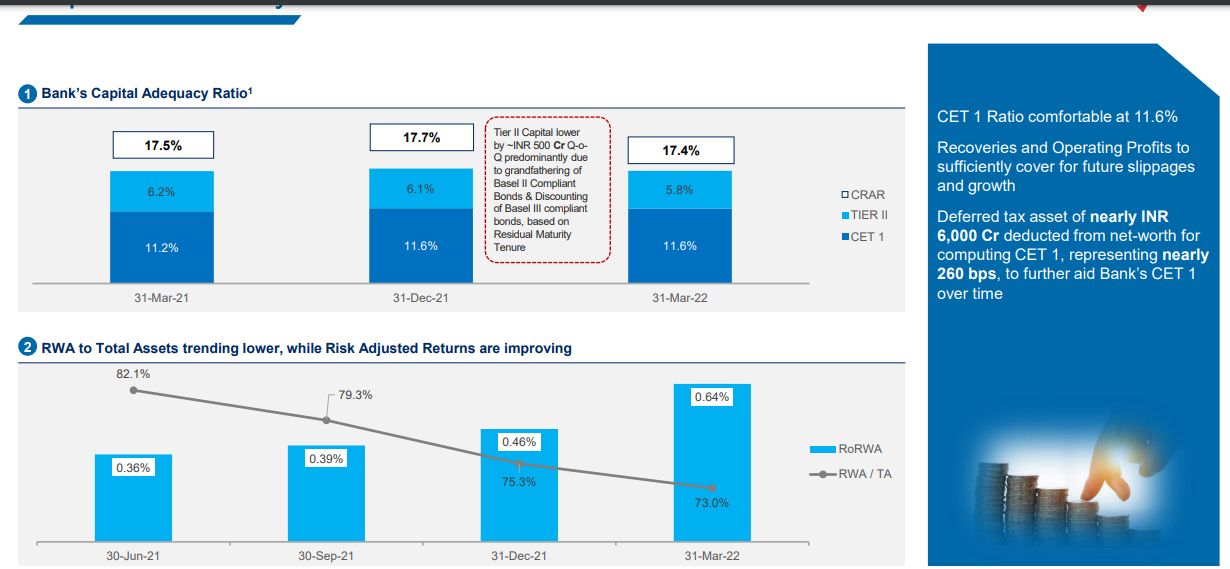

One very important point I have missed . This a screenshot from investor presentation. It states that yes bank has a deferred tax asset of 6000cr which is not included in their CET 1. This 6000cr is going to increase their net worth as they relies profit in next financial year Because they are not liable to pay tax.

2 Likes

RBI has announced a surprise repo rate increase by 40 basis points. While this is not a news specific to Yes bank, this will have cascading impact on the cost of borrowing, FD interest rates and so on.

Moderators: Please remove if this is post is not appropriate in this forum

1 Like

Yes bank has a CASA ratio of 31.1% and rest 68.9% is Fixed deposit. Because of rate hike their yield on advances are likely to go high which has a direct impact on asset quality but most of the advances of banks are Floating rate loan which means they keep on changing according to the economic condition. Current yield for yes bank is at 8.1% which might go up to 8.6% to 9% and their cost of deposit is 5.3% which might maximum go up to 5.6%. Reason being is their deposit rate is at 4.8% which is already quite high when compared to peers they will not increase it further. After this rate hike even after considering the increased bad asset they might end up making 10 to 20bps which is 200 to 400 cr

1 Like

The have started doing the rate hikes

2 Likes

Hi guys,

I just want to share something not related to yes bank please don’t mind.

People who don’t want big returns in market there is a very good opportunity for them I would like to share that with you.

Currently a 10 year government bond is trading at a yield of 7.3%. The par value is 100 Rs with a coupon rate of 6.8% and the value of the bond in secondary market 94.5rs so the yield comes out to be 7.3%

The bond prices are low because of high inflation resulting to high yield. Now the yield are bound to come down once inflation cools off it might take maximum 2 yrs.

So if you buy the bond at 94.5rs this price is bound to go back 100 in maximum 2yrs it can even be faster.

So if you take your interest of 6.8*2 Rs for 2 yrs and then sell the bond at 100 making a capital gain of 5.5rs you end up making 19.1rs on 94.5rs which comes out to be 20% in 2yrs with extremally low risk because it is government bond.

Now even if the bond price go down which over the next 2 yrs you need not worry because during redemption government is going to give you back your 100rs regardless of market price but in this case you will have to wait until redemption.

In case 1 you make 10% per year in case 2 you might make 7.5% or 8% per year.

Most of the working class who do not want to risk their their money in market and want to enter in next 2 or 3yrs but still want better returns than FD , this is a one time opportunity for them

6 Likes

How do we buy Government bonds? I am having some issues opening RBI Retail Direct account. Any other option?

1 Like

You should probably open a new thread on this with something like “GOI bonds and yields”

And expand a little more. Most people would not be follow the calculations you’ve done. Just a suggestion

4 Likes

If there is already a thread with the same topic i will not be creating a new thread if not then why not. I have not shared the negative side of bonds which i feel i should share because only the good side of bonds might misguide people

anjeshv4,

I think you should try to find out the problem with retail direct account because according to me that is the best way to purchase bonds. If you find it very difficult to open an account there then i think you can purchase it from zerodha COIN platform as well

1 Like

Hi guys,

Just wanted to tell you how the transaction between yes bank and ARC would happen.

I don’t have a great accounting knowledge .Please do correct me if you think I am wrong.

Yes bank is going to transfer 50000cr to ARC out of this 16302cr is written off. So when yes bank transferers its asset to ARC the asset side on the balance sheet will reduce by 36479cr.

Since there is a provision of 26419cr the liability side will also reduce by 26419cr. So if you see net-net the asset side has been reduced by 10000cr.

The ARC is valuing the asset of yes bank between 11000cr to 13000cr so let us assume it is 12000cr. Now this 12000cr will add to the asset side of the balance sheet.15% as cash and 85% as security receipt.

If you see the entire transaction, yes bank has given 10000cr and received 12000cr. So according to me this 2000cr access will go to the reserve and surplus, to balance the balance sheet. That means their book value will increase by 0.80 paisa.

Now the big question is that weather they can root this 2000cr through p&l or not. I feel they cannot root it through P&L and it will be directly added to Reserve & surplus.

Any recovery made by the ARC. lets assume 1000cr then 15% of the recovery will be given to ARC as their fees and rest 85% can be realized by yes bank.

Any recovery made after completing the recovery of 12000cr will not be given to yes bank. eg: if ARC recovers 20000cr then yes bank will receive only 85% of 12000cr.

So it think we can make a conclusion , anything received above 10000cr will go to their reserve and surplus.

All the calculation and figures have been taken for the above article.

4 Likes

Hi,

This article calls out Kotak Banks board approval to invest 500 crores into YB, which given the date of article implies that its an additional 500 Cr to their amount at the time of the rescue of the bank, 2 years back. Now while this is great news to read, I am unable to find a Kotak Board meeting summary that points this out this approval.

Has anyone else read this board meeting approval ?

Another point to consider is that if this 10000 crore raise happens via equity, then it leads to even further dilution as a downside, but then that also potentially strengthens the probability for a reverse stock split happening

1 Like