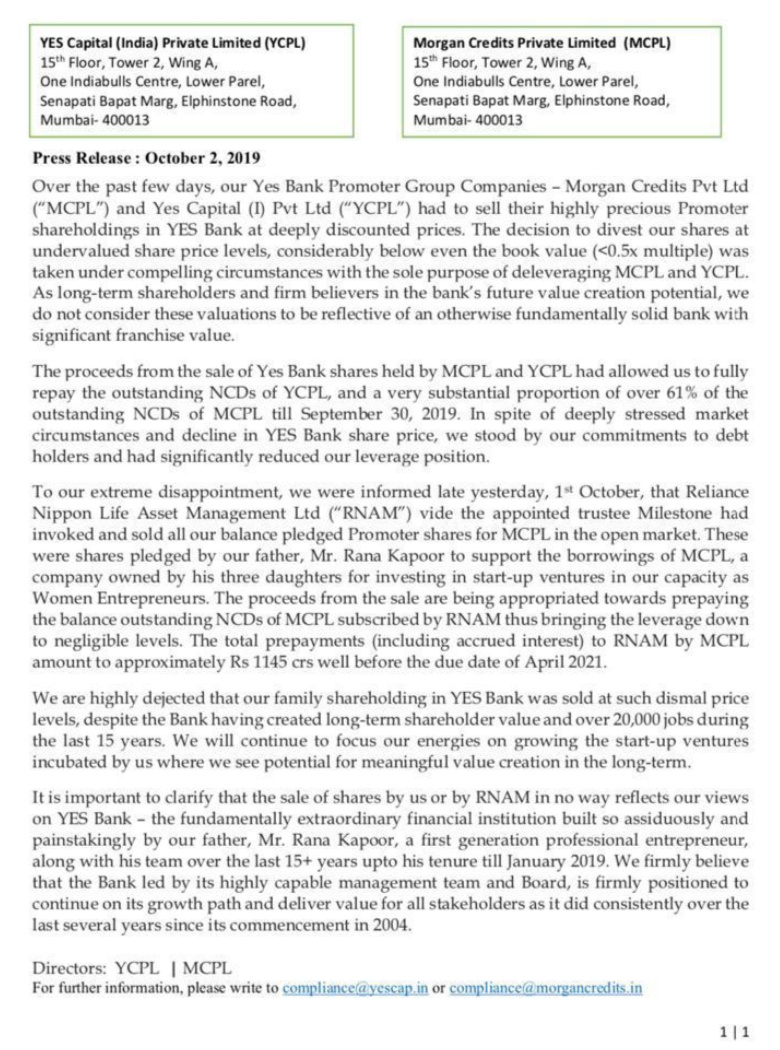

Look’s like RNAM’s trustee(Milestone) has sold all the holdings of Yes as per press release by Yes Capital/Morgan Credits…

At least he is one person who is advising not to panic.

P.S. I am also invested in yes bank and i am sure I am not selling below qip rate of 83, whatever time it takes.

The fall from 83 to below 40 looks to be orchestrated for the sole reason of pushing RK out. Someone shared on twitter that 40 is the cutoff price below which all the holdings of RK will not be sufficient as a collateral. Before this 60% fall from QIP price, YB was still not looking good but at least one could see that even some of the darling of value investors like Edelweiss were also down in a similar range despite being headed by a management which is considered very good if not gold standard. So while no one has anything good to say about RK - and rightly so - what is the current consensus about managements of Edelweiss (or even RBL)?

All of them suffer from potentially higher NPA going forward and there is lack of buyer interest as they themselves are not aware of depth of the issue. I think folks need to wait for Q2 to figure out way forward.

The other promoter family seems to be sticking around for some more time. I am very sure that they would make more money than RK and family who acted smart and denied their rights. This is called poetic justice.

“During 18-20 September, Monga, whose name was once pitched by the board as the chief executive officer candidate to succeed Rana Kapoor, divested his entire stake for ₹8.22 crore. Ashish Agarwal sold almost his entire Yes Bank stake for ₹5.64 crore.”

8 am tomorrow morning is the analyst call .

Does any one has concall details as they have not mentioned it in press release

Yes Bank ConCall update

• During this quarter Yes Bank has opened 180,000 new account in retail segment, up 18% QoQ

• Opening of new Fixed Deposit account up 39% QoQ

• SME business up 8% QoQ

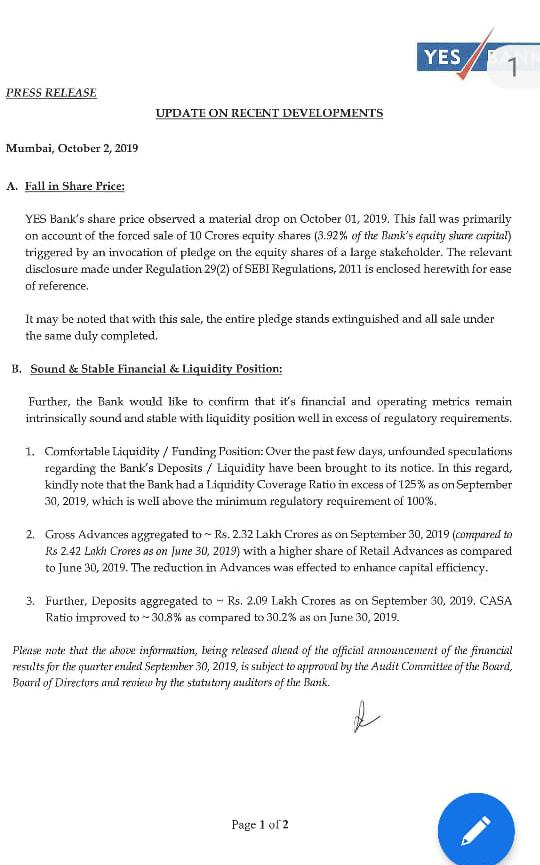

• Gross advances at Rs 2.32 lakh crore vs Rs 2.42 lakh crore QoQ; deposits at Rs 2.09 lakh crore

• CASA ratio improved to 30.8% from 30.2% QoQ

• Deposit and CASA book declined during this quarter in line with advances

• Cost of fund will gradually come down significantly going forward

• Liquidity position is well above regulatory threshold; liquidity coverage ratio is at 125%

• Many of the top level management have sold their share in last two weeks as they have taken leverage to exercise their ESOPs and now they are selling to payback their debt

• There is no such case that depositors withdrawing their money from the bank due to trust crisis

• Yes Bank is in talks with few PE players, strategic investor and family office to raise capital

• Pledge shares of another promoter group (co founder Late Mr. Ashok Kapurs’ family) is very less

• Yes Bank had a very detailed and clear talk with regulator and Ministry of Finance and they want to see Yes Bank as an independent organization. There is no plan for any merger

Anything about stressed assets ?

Management not discussed much about the financials as result is yet to come

When asked about raising required capital at current valuations and SEBI pricing formula, management said that they would raise it at a time when share price is reflective of the business’s value. They said they will not raise capital at any price. They also spoke of selling their loan book to generate capital organically if required.

Another point they said is that as per rules, if preferential allotment is only to QIBs and there are not more than 5 such buyers (along with some other requirements which they didn’t state in the concall), then the price can be calculated based on two weeks’ average price and not necessarily the 26week average price.

Yes bank dont need any more capital as if now, they created buffer of 10K by selling some loans, smart approach by Ravneet Gill, though he is bullish on growth capital, raising capital at this point will be huge negative, mantra should be preserve the capital and grow transaction banking, i see agressivness from yes in salary account, Credit cards, EMI schemes, focus is moved to retail as of now which is demand of an hour, once economy rebounds this will move faster, P/B of 3 should be a normal scenario in 12 months.

Hmmm…everything else can be discussed but when it comes to asset quality, they are in Silent Period. Not sure what to make of it.

Is 12k cr.loan given to ADAG group is secured? Gill has not clarify how will he recover this large NPA or a part of it.

I feel market has already priced in this worst case case. Entire ADAG of 12k is assumed to be gone. Any recovery from here will boost yes bank

A basic question: Why are they having a ConCall now and sharing such sensitive info with selected investors? Have they declared the Q2 results? Based on the posts, I believe that the call details were not shared with public. I will delete this post, if I’m wrong.

Are they currently adequately capitalised as per RBI norms?

Answers lot of questions on deposits, capital, merger etc.,: