The situation at Yes Bank seems really dire. So many bad loans, no wonder it is getting hammered daily. And there is no price low enough for short sellers. I have mentally given up on ever recovering my investment in this scrip. ![]()

Capital raising is approved by RBI. Though who will invest at this level is a debate for many.

The way Yes Bank stock price is falling, I too have lost all hope of recovering the capital. In my view taking a decision to invest in Yes Bank has become very simple: If one trusts Ravneet Gill and the numbers the bank puts out in its press releases, just go ahead and buy truck loads. Else stay away.

It looks as if today’s fall of 25% has more to do with further promoter selling.

Excerpts of today’s CNBC interview with Ravneet Gill:

Whats ailing YB stock?

When a sector is in trouble and a certain stock falls, at times correlation between operating performance of the company and stock performance breaks down. YB is in better shape than 6 months back. Granular business, cost of funding is down, asset book stabilized, shoring up liabilities etc good. Difficult to explain why the stock has moved the way it has.

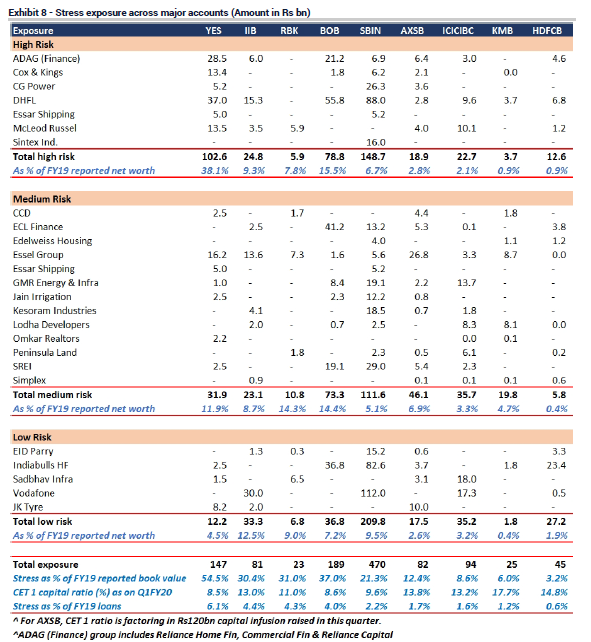

Of standard stressed (ADAG, Essel and DHFL) adds up to 85% of banks net worth- 24200cr total exposure to these groups. Should we expect more NPA in coming quarters?

Agreed that NPA resolution is slower than expected. However, the progress is satisfactory. So these should not be dragging the stock down. Managing these exposures satisfactorily. Everything going in the direction we wanted. They are not weighing on our assets.

IDFC Securities expects GNPA to rise to 9% by FY20?

It is an exaggeration. Asset book, deposit accretion and all they talk about is unfounded. Would have been better if they reached out to the bank before writing. All this is undermining investor and depositor confidence. Authorities should look into this.

Will greater provisioning be needed compared to Q1 nos?

We don’t have exposure to any other NBFCs than already told. Exposure to IBHF is not a large no and has come down 30% in last 2 quarters. Going well. Never faced any delays. When we look at large financial institutions, we should look at the runway that business has in future. We had a large technology company yesterday and YB is the best among all the banks. YB has lot of advantages. Business as usual, look at the path forward. Capital will come in.

How about capital?

Good traction than what the market is giving us credit for. 3 types of investors are showing great interest- traditional equity funds, traditional funds and highly regarded Indian family offices. Confident.

Dilution?

We should raise as much capital as it needs. Huge opportunity for growth. Capital is critical. There are restrictions on what individual share holders can hold, but we will get it from the mix of three buckets of investors.

Tell us more about stressed book. BB and below book? At 9.4% last time you spoke to investors. Has it increased?

Govt came out dispensation w.r.t. MSME loans. YB didn’t have a single exposure. Asset quality stabilized. Underwriting standards, businesses we want to grow etc is being done. We are growing.

How is growth?

Over the last 2 quarters there has been consolidation. We want to grow granular businesses. We were able to shrink wholesale and grow retail. This quarter also the same. We were able conserve capital and stabilize asset quality this quarter.

Indiabulls exposure? What is the exact exposure and percentage of net worth?

Can’t say in public forum. Absolutely manageable exposure. No liquidity issues. Last week also there was a payment that was made on time.

Is it true that 22% of your net worth is Indiabulls group?

No, it is false.

When can we expect more capital? This calendar year?

It is much more advanced than what the market anticipates. The quality of investors/franchise coming in is very high quality and that will really cheer the market and boost sentiments. Potentially the single largest investment thesis in the decade.

Rana Kapoor also selling?

Whatever stake the promoter has sold is to deleverage his personal debt. The decision he has taken is enlightened one. I think it is done and there isn’t more to come. It is in the interest of the bank. Investors that we are talking to are seeing promoter sale in that light and not negatively.

Current promoter stake (between both Kapoors)?

It is closer to 13%.

Are you finding it hard to raise deposits and borrowing due to NPAs, weak financials? RBI oversight wil increase due to PMC?

Agreed that the high seas are choppy. Just because a boat capsizes doesn’t mean ship will capsize. Not to be able to make the distinction between a small boat and large is not just naive but motivated.

What is the worst GNPA can become?

I won’t want to look forward with respect to that. Asset quality has stabilized. Even sternest critics are saying we have done a stellar job with respect to liability profile. From retail liability, we have opened 39% new FDs above last quarter. So even the comparison with PMC is very irresponsible.

Stressed book is 50,000cr? Equity value is 10000cr?

How was this 50,000cr arrived at? We had put out BB and below 29000cr. Culled out of it was 10000cr watchlist, a derivate of the 29k. People look at it as 29+10k. These are the numbers I am familiar with and unless someone knows better about the bank than I do, I don’t know where the 50k no comes from.

Rumors about you leaving the bank?

No, not at all. Really happy to work with the team. Absolute privilege. Last week the head of a Asia Pacific team who was doing due diligence, who expected the team to be down and introspective said that he was blown away with the energy of the team.

Though even I have incurred heavy loss in YES BANK, I think it is too cheap. Mr Gill appears to be a genuine person and I am trusting every word he says. I have used the down fall yesterday and today to buy more shares to average downwards.

Let us see what is in store in fate. Based upon information available in public domain,

I am hopeful it can double in two years to about Rs 80-100, in which case it will turn out to be better investment than many of the blue chips.

If bank collapses- it is a different issue. But, if it survives, it can be a great investment at current price.

Disc: invested heavily and increased holding in the present downturn.

So is RK finally out?

Looks like RK is out now, all downfall from 88 to 32 was created to make RK exit from Yes Bank, he paid for his sins badly here, kotak will have a laugh at end of day. Founder of a bank is kicked out and his all holdings snatched.

Fall below 50 could have triggered the remaining stake sale as loan pending is still 300 cr if i am not mistaken.

Investors need to remember that this Gill guy is just a hired gun who is talking his book moreover he is from Deutsche which is an investment bank so he likely has no clue about NPAs and their resolution process.

As per Rana Kapur’s letter to exchanges, the family had paid back all the loan, along with interest, to Reliance Nippon. !! Therefore could this news item be just a rumour to support shorting the stock?

Looks like Diamond Merchant is finally forced out by the way of pledged shares encashment by RNAM. the crash from 80+ to 30 is purely because of Promoter and Top level oldie bank directors sellings followed by PMC bank crisis that happened in last few days. As an Investor almost getting to lose capital in full as not much is left anyways, Hoping no more selling left with this counter now, other wise the next stop seems 10 and below. The sentiment with weak banks is already bad in the market due to PMC saga and depositors already spreading the message in all possible social platforms. RBI assurance press release of banks being strong wouldn’t help much now. They have to scrutinize each and every doubtful bank including co-operatives and take a stand on each one of them. If they can’t regulate a bank then at least take a stand like what our FM did by saying “Multi state cooperative institutions do not come under Finance Ministry”. Was this some kind of indirect messaging to public? at least seems so from the public’s interpretation!

Latest Interview by Mr Gill to CNBC-TV18.

Exactly my thoughts. He jumped from another sinking ship to here. Some folks here are thinking that he has a magic wand which will fix all the issues…

The job of management is try to save the ship until it really capsized. Even RK said diamonds etc and now diamonds became Peanuts. Business from investments perspective will be different than business as usual. The last leg of shutting down will happen when retail depositors get panic and queue up for withdrawal. But will govt will allow that to happen ? Or will be a merger or take over before that ??

It seems even merger or take over should give more than CMP (in case of any share swap etc…).

Disc: Large part of my PF and mentally marked this notional loss as permanent loss.

I have been extremely bearish on YB right since 2015 and now feel vindicated. The promoter and his cronies have sold or forced to sell their holding completely. The next logical step would be changes in the organisation and the board. I think Mr. Gill was indicating interest of some big investors but it is clear that no one would write a big cheque to a troubled promoter. Mr. RK was supposed to be out in due course but he went out after gross humiliation. I don’t think one has to be excessively bearish anymore once this issue is over. Everyone including the regulator would be more comfortable dealing with a clean slate. One needs to understand that banking is a trust business and the new promoter and management can bring trust back. The other Kapoor family may be less flamboyant but appears committed and will create less negative newsflow. I think from now on it will be a high risk and high return game. Only worry is that RBI might force it to merge with any other bank if it poses any systemic risk to the system.

Disc: No holding

Mr Gill mentions - “Well respected,highly regarded family houses” as one of the a potential investor and indicates this capital raising going to be very big, most likely combining all three type of investors (PE,strategic investors and this family houses)

What’s more curious is the third one, which is that family business house which has pan india wide presence ?

Bajaj , Tata and Reliance(??)

My gut feeling is the TATA might venture into banking space.

PS: Invested in YES bank and not-selling optimism here, just curious on the “family house”

Plase do not trust this person…he is useless…i remember 3-4 years back he was suggeting to buy Suzlon at 30/-. Based on his crap view I sold VIP indistries at 60/-.

PS: Stuck in Yes Bank with one of my large hodling and not sure what to do with it ![]()