Will this be good for minority share holders and for Bank if they can raise 1.2 billion dollars. What impact it will have on valuations. At current price , its trading on book value , I assume raising funds will dilute equity and decrease EPS but it might increase Book value , as net worth will increase due to infusion of capital. So , will this be positive or negative for minority shareholders. I am not an expert in financial analysis , can any one please answer my query.

EPS needs to be compared to Book Value per share. Both will fall, and hence price will fall accordingly to maintain P/E and P/BV

I am surprised, can QIP happen at such premium with a current state of Yes bank?

Unless it falls another 50% then yes. Institutional investors know that they cannot buy 15% of Yes bank from open market without raising price. Plus I am not sure buying from open market would entitle you to a board seat. So if QIP happens that will happen at a premium to market price.

@pkk123, The last time Yes bank tried QIP, the price was 3 % less than prevailing market price in 2016, and had to cancel it due to drop in the share price below the issue price.

Fund managers have to justify their purchases, so without any incentives in QIP vis-a-vis share price, they wouldn’t invest. So thinking of raising fund at 150 when current price is 110 is wishful thinking.

9 Likes

Hi Ashish,

I am aware of what happened then. Please refer to the following:

On the back of a near-100% appreciation in the past year, Kapoor wanted aggressive pricing, leveraging on the premium that had already accumulated on the stock. But investors were not convinced it deserved to be bought at more than four times last year’s book value.

Read more at:

//economictimes.indiatimes.com/articleshow/54283780.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

Valuations are no longer in the range they were last time. Plus management is aware that they may not get the desired valuation now and hence have indicated that they may be doing the QIP in two tranches - some money now (of course at lower valuation) to tide over the troubles in near term and a second tranche later (at a better valuation). Let’s see how it plays out.

1 Like

@pkk123, have a look at the large deal for last few days, if some fund managers want they can buy large quantities without influencing the price. In 2016, yes bank was the most sought after bank for investors/ fund managers still couldn’t get premium, now its in complete shambles so raising equity at premium to share price looks far fetched. Also fund managers would like to carry due diligence before committing to invest. Whatever may be the price of QIP the existing investors are going to lose in short to medium term with the huge dilution coming at lower valuation.

7 Likes

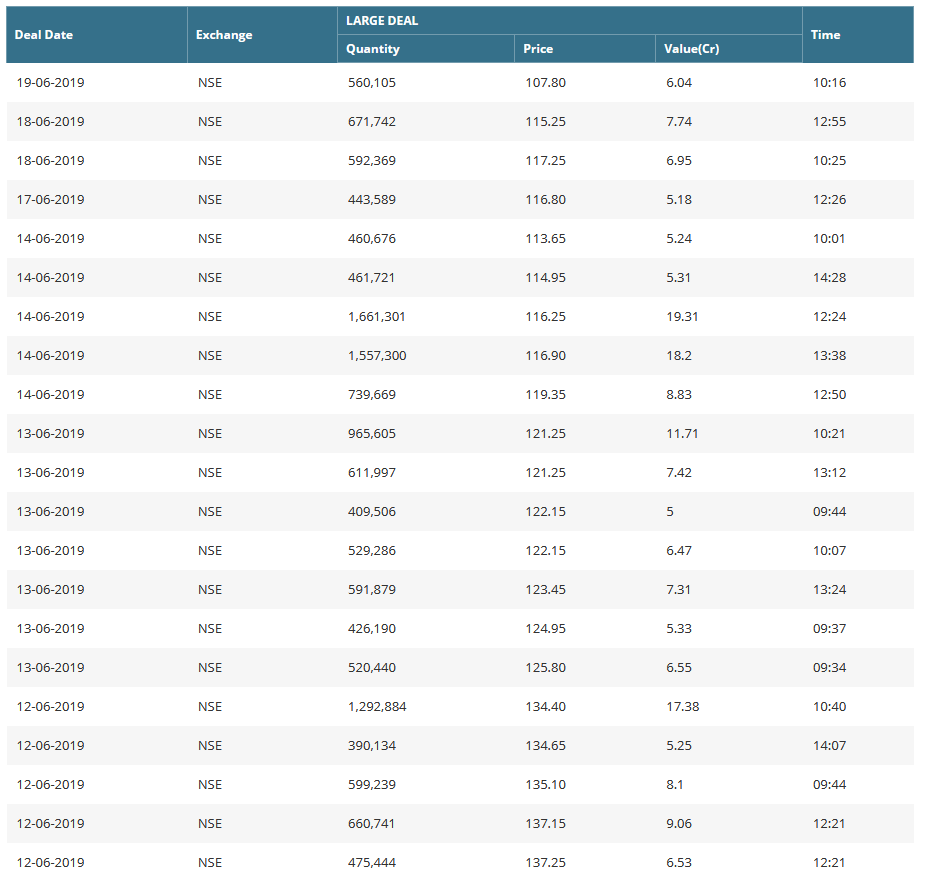

Hi Ashish,

This screenshot shows trades of about 200 crores worth. Yes is looking to raise a billion USD. Buying that much from open market would trigger an open offer besides raising the price. Having said that, its difficult to argue for premium in the face of stock price crashing daily by 5-10%. Let’s hope for the best.

2 Likes

Fair point. But a QIP buyer would look at the books before buying. A QIP buyer would want a board seat. Can an open market buyer demand those things?

Open offer is not the only other option. You can buy through bulk deals also.

Seems Q1 & Q2 result will have major things recorded in black & white… hopefully start of Q3 will give right opportunity for investors with a cleaner slate

1 Like

Risk To Yes bank are:

New CEO will take time to cleanup books

New CEO from foreign deutsche bank (25 years) will take time as things are different in indian bank

Scaling Up retail portfolio is getting tougher both on liabilities as well as assets as competition like SFB etc

Structured lending to DHFL ADAG etc

Timing & Pricing of capital raise both are at risk

Growth is at risk

If want to invest need to take long term view to sort all these issues.

Risk and stress based adjusted return does not look good enough for me(better to get HDFC Bank)

2 Likes

You are right on risk and stress part. Yes Bank investors often forget this part. I’ll tell my own story here.

I was invested in Yes Bank from 2010 to 2014 and had 20% of portfolio in it. My split adjusted average price was 54. The promise was the fast growing corporate bank which was improving all parameters like CASA, ROA with nil net NPA.

The Bank was doing well and Andhra MFI crisis of 2011 came. The stock was down 30% from top in no time. The things settled eventually. Till 2013, few more 15-20% draw downs came. Then the INR fell sharply and along with other financials Yes Bank was down by 55%. It was gut wrenching for me. It’s not easy to see your 20% folio holding going down 55%. It eventually recovered. But I had enough of pain over the years. I sold it at 116 in 2014 making 2.2X. This was the hardest 2X I have ever made.

Compare this with HDFC Bank I am holding since 2011. The stock had maximum 20% draw down in all these years. That too only once. And guess what, the price is up 6X from 2011. Even if you ignore recent 50% fall in Yes Bank, it still doesn’t match HDFC Banks price performance.

Another point is it’s never easy to make a good exit in Yes Bank. Whenever you spot some good opportunity elsewhere, YB is in one trouble or other and you almost never get good price to exit. It’s maybe only 10% of the time that market feels good about YB and you make a good sell.

All in all, YB is only for buy and forget investors (I know a few who bought since IPO and planning to hold forever). If you are an active investor and track stock prices regularly, don’t even think of investing in YB (trading is fine).

18 Likes

Nikhil - agree with everything you said about yes bank.

What needs to be also considered is that purchase price is the biggest determinant to returns. Current 1x P/B & 22-25% growth can rerate to 2x P/B & Book could double in 3-4 years so 4x type returns are possible provided company executes. If book shrinks by 10-15% then it can take may be 5 years(worst case).

Bank has a retail and SME portfolio which is pretty much flawless, growing faster and should be half of the book at that time.

Hello friends, This is regarding an observation for credit cards business by Yes bank.

Last year from maybe June’18, yes bank was issuing lifetime free credit cards to all. Even their top end cards like yes first and yes exclusive were also issued lifetime free. This maybe done to aggressively enter the already competitive market which is mostly owned by HDFC Bank( they have the largest market share in credit cards).

Can someone help me understand, how to determine the revenue generated by credit card business?

Also, recently Yesbank (similar to HDFC Bank smartbuy platform) launched Yescart website where you can shop products from Amazon, Flipkart, Myntra and Tata Cliq and earn some extra reward points on Credit Cards and cashback on Debit Cards on shopping. I want to understand, how does this work?

I mean either yes bank has registered themselves as affiliates and earn some money from Amazon, Flipkart, etc. or they are burning their own cash.

If my queries are not relevant, please ignore and I will withdraw my post.

1 Like

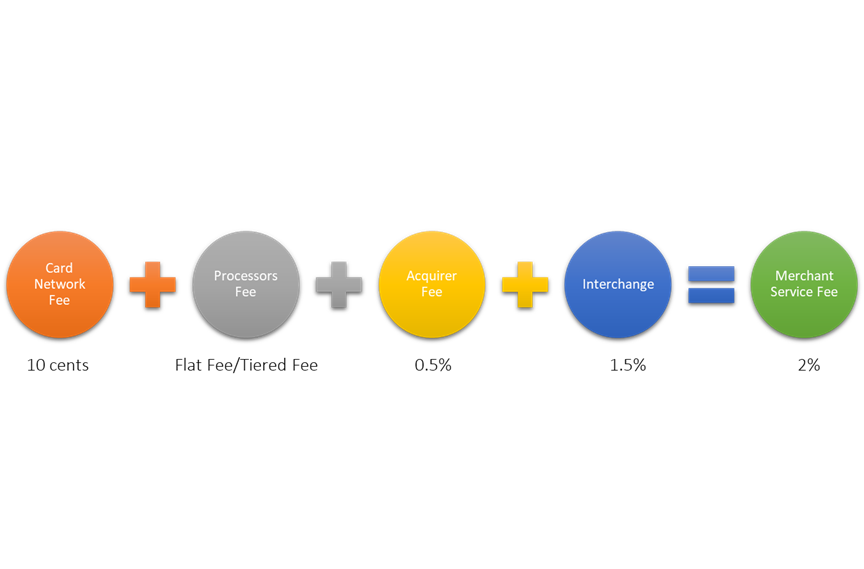

There are three ways a credit card earns money.

1)On transaction fees. Credit cards charge around 1.8%(negotiable) plus gst from merchant on every swipe .

2) Interest and fees on late payment which can go from 24 to 48%.

3)Fees and interest on emi transactions.

3 Likes

Another perspective from Amit Stallion Asset and definitely not something this thread has not discovered yet.

5 Likes

Hi

I had covered this topic in detail in last year’s VP Goa meet. Link to the deck

Pasting the mechanics for revenue generation with an example

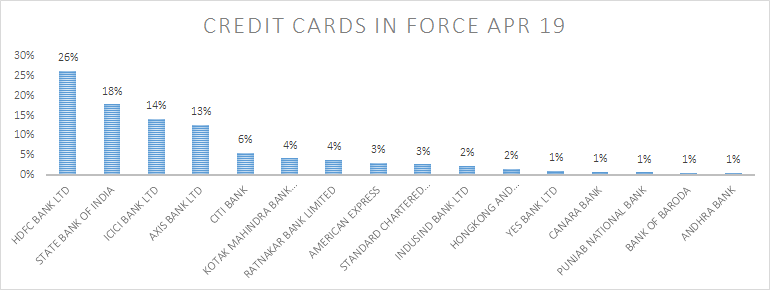

On the issuance side for credit cards YBL is an insignificant player. The average txn size per card for YBL (assuming all cards are active) is 22% below industry average.

It has only 1% of the cards in force in the market.

I would not give time to evaluate this business of the bank as its too fledgling.

Rgds

Deepak

disc: studying the company have tracker position. have been invested before.

1 Like

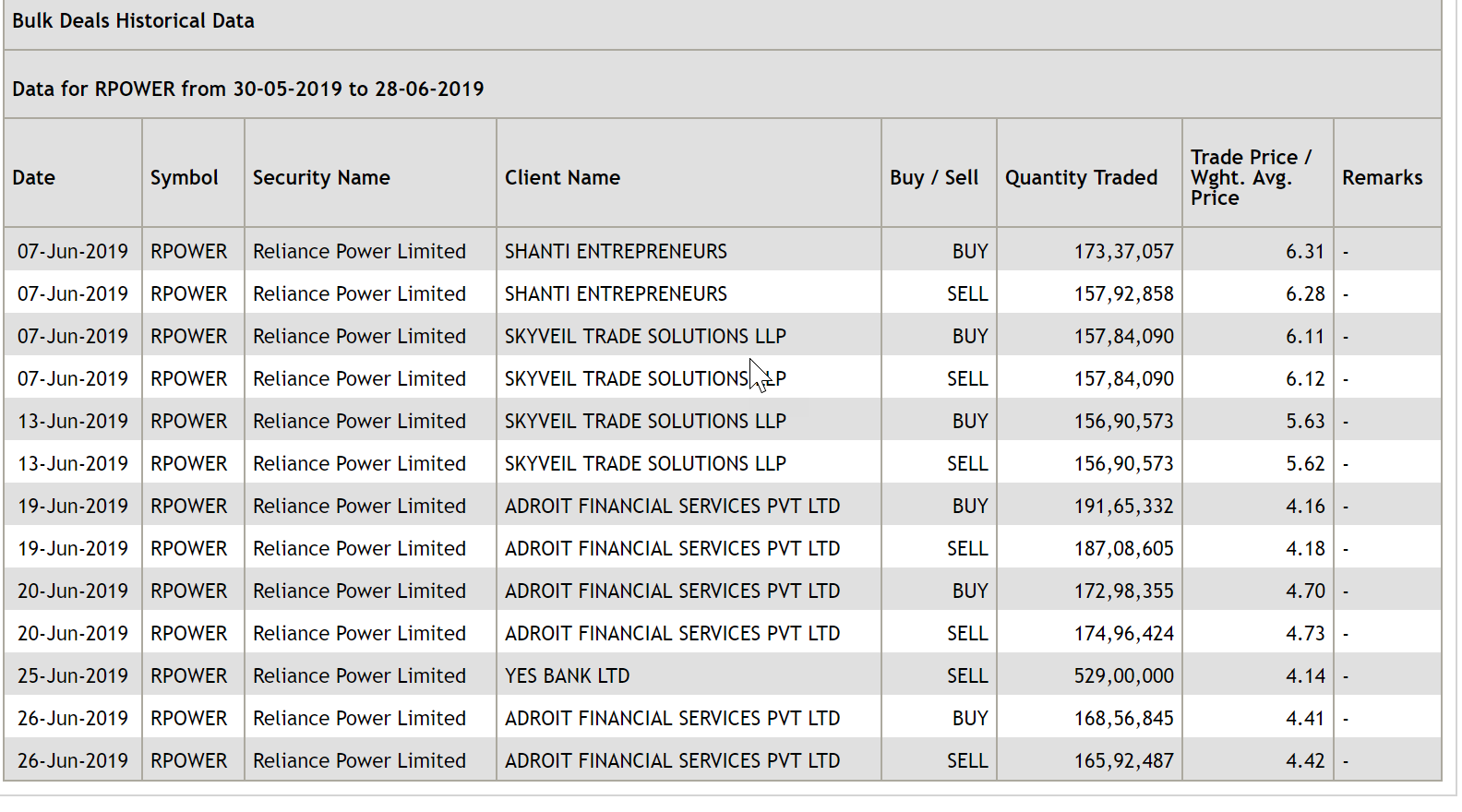

Yes selling RPOWER shares in open market( 21 CR). looks like they have given up on recovery from RPOWER now.

1 Like