Bruckner India senior ex-employee scuttlebutt

I had a chat with a senior bruckner india ex employee regarding bruckner. Please find notes below:

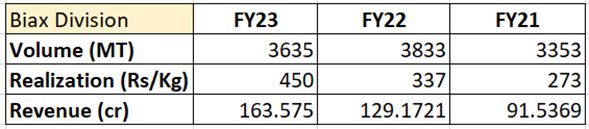

the purpose of this call is to evaluate a company called XPro india limited which is an indian Biaxial dileetric capacitor film maker.

Q1. Why does it take bruckner so much time to scale up production? For companies ordering today the delivery date is 4 years away. Why? What limits bruckner’s scaling up?

A: Biax oriented film. Oriented in 2 directions. Longitudinal direction. Other type of film monoaxial are very compact machine. Biax tech is a huge machine. THis machine takes lot of time.More than 70,000 components. Different suppliers. Manufacturers. Testing/validation. It is set of 16 machines integrated & synchronized together electronically. Continuous operation operated from single control room. Mechanical configuration takes lot of time, writing logic takes lot of time. Since 2009 onwards, demand for packaging film has grown very high level domestic as well as export. This has led to heavy burden on machine maker. Demand or repeatability of 1 part. Sourcing has to be from same supplier who supplied that part earlier. Its like a sine way. It goes up, Drops down, again goes up. Its like a sine wave. Even sub supplier may not be ready to expand on a small demand.

Q2. To what extent are these capacitor film biax extrusion lines/machines customized by the capacitor fim company per the order of the customer?

A: Capacitor grade: different grades for input. Although substrate is PP. But we need metallization also. Biax orientation is same in packaging & cap films. Cap grade film fall under technical or specialty grade. Not commodity grade product. High end application. Difficult type of manufacturing under controlled clean room manufacturing. Machines are customized. Normal PP is different from capacitor grade. Capacitor grade doesnt go beyond 1000 KG/hour. 1 customization which is done on all machine. Must be able to cater to Low speed operation. Diff sections like: RM handling, drying, extrusion, filtration, minimum & maximum flow rate. Normal flow rate does not work for capacitor films. Capacitor: Thin & ultra thin films. 2 micron to 15 micron films. All packaging: 10-75 micron film. Lot of customization is needed. Filtration is very low volume. Diff types of filters. There may not a cooling bath, low volume cooling bath, the feet that are designed have a different structure, different finish, Contact winding, gap winding, online treatment where operating parameters are customized, cap film: very narrow width: 400mm. Packaging is 1200 mm wide. Low capacity production. Precision control of operating parameters, hygienic environment.

Q3. Is the configuration of such machines a secret sauce of the client? Is it possible for bruckner to sell the same machine which they sold to xpro to also sell the same machine to any other capacitor film maker in india? Or is the design/configuration of such machine lines protected by any IP (intellectual property) which XPRO owns?

- This machine is producing PP Cap film for grade. Tech or operation in each machine is specific to stage of production. Some of these stages have been patented. Spinning on steam roll. Edge cutting. Thickness scanner. Some of these technologies have been patented. You start discussing what you want exactly. If any of your demand falls into bucket that bruckner has agreed with previous customer, if they sell 1 machine to 1 region or country, then that customer can enter into agreement with bruckner to not sell same machine to anyone else. Agreements can exist.

For so & so machine bruckner may not be able to supply and will outright refuse. Few machine or few section have got IP protocol. They are not ready to discuss enquiry & quotation for some machines.

Q4. Why is there not much competition for such machines ? Why does bruckner have a monopoly in this space?

A: Machine technology is of orientation. Developed in 1960s. Pioneer was Mr bruckner. Another german company started making. Lot of people tried to copy the machine. Bruckner is best for PP. Someone else could be best for polyester. Each company has their own specialized fields. Fair technology practices. In china they try to copy. But there are lot of things behind : metallurgy, requirements, performance may not be the same. Couple of companies are well reputed. Bruckner is market leader for PP based biax capacitor films. Efficiency, reliability, engineering etc bruckner is best.

Q5. Xpro has placed an order for these machines in 2021 september. The timeline they shared with their investors is 2-4 years from then. Does that sound like a reasonable timeline to you?

A: No way anyone else can supply machine in a period less than that.

Q6. Biax machines: Pricing of machines: 20m euro.

A: Price of machine is machine is driven by features you add into it. You can even bring it down as long as you have experience & knowledge to bring it down. Technical negotiation rather than price negotiation. Level of automation. Make of the machines.

Q7. Can client customize in house?

A: What bruckner does is: It goes up & then comes down, The entire value chain is cyclical, Business of machine supplier is also cyclical. How do they ensure they have continuous business? By way of upgrades, spare parts (identical & same): customization has to be there, otherwise every

2. Whether you can customize in house: generally there are guarantee & warranty clauses: maybe 24 months or X months. Until such time you cannot modify it in house. I need support for next XX months. Then that will add to the pricing also. Protocol for handover : free to tamper, upgrade it, reinstall it, whatever you want you are free to do, OEM will also help you with upgradation service.

Q8. Buying this machine is not like you tell i want to buy capacitor grade machine. You give enquiry takes 1 year to finalize the agreement. They have to combine ingredient according to client requirement. Client has to be technically prepared. Sending right enquiry. Bruckenr needs 2 months : 3 big box file quotations. Several sections of machine.

Q9. Can a client use packaging film machine to make capacitor films:

A: It seems possible. But they have to do capacity downsizing. Clean room conditions, hygienic conditions

Book lamination varies by 5% doesnt matter. Change in thickness of flim changes the capacitance of the capacitor.

Needs lot of Precision by way of understanding the bottlenecks of different sections.

Major hardware changes. (Sahil’s notes: this is what xpro must have done for first machine) For a week you have to keep line idle.

Q10. Who are the other large customers for bruckner’s capacitor film division in the world who have the capability to manufacture 2-4 micron capacitor films at scale ? Name & country.

- Toray industries: japan, few companies in china , few in taiwan,

- Capacitor film: Being low volume, client cannot buy a huge container, do not need tonnes of the film. People try to find suppliers near to them to avoid freight costs etc.

To be most interesting insight was that the machine is very complex, and difficult to create in house. The complex supply chain means that any of the dozens of sub-vendors or the 10000s of components could be the bottleneck

Disclosures same as before