The management is focussed on there business there is no doubt. It’s just after two high growth years they are seeing some dip in footfalls. They are doing fund raise to fuel growth for next 7-8 years comprising 5 park. They don’t need fund for Chennai park. They have moat in there business as they manufacture and install there own rides. I think next ten year all we see a new wonderla. I think they will raise approx 1500 - 2000 cr for atleat 2 big parks like Chennai and Bangalore(500 cr each) and 3 tier 2 parks like orissa and kochi (200 cr each)

4 Likes

Q1FY25 Concall Summary

Business Updates

- The growth was lower due to external factors and footfalls were affected by heat wave, elections and water shortages

- There has also been a decline in discretionary spending

- The fourth park at Bhubaneswar has commenced operations during the quarter

- The park in Chennai is expected to operationalize in Dec 2025

- The management is in talks with other states for new parks and board has given approval for a fund raise to setup capex for the new parks over the next 7-8 years

Participants

Ambit Capital

RK Bhojani & Associates

RSPN Ventures

DSP Mutual Fund

QnA

- The expectation for Bhubaneswar park is a footfall of 4.5 lakhs for the first year and expecting a double digit footfall growth post that for the initial years

- There are 2-3 projects already in the pipeline so would like to raise the capital first and it will be declared to exchange in due course of time once finalized

- Presently there are 4 operating parks and one under construction. The company is in talks with state governments for 5 other parks and thus the capital raise will be for this expansion over the next 7-8 years

- The revenue from Bhubaneswar in Q1 was Rs 9 crores and EBITDA in Q1 was around Rs 85 lakhs. This was operational for around 38 days

- The moat with the company is a combination of an amusement park and water park and the ride quality is better with lower cost of setup

- The focus will be to get the footfall back and could resort to discounting as well which will keep the ARPU in check and hence not much growth in this number should be expected

5 Likes

My sense is that current moderate margin profile is here to stay because they will be in expansion mode for next 4-5 yrs (with one new park being added every 1-2 years) at least. Hence until operational parks count becomes substantial their margin numbers will continue to be dragged down because of operating de-leverage.

On topline growth, Bangalore had serious water crisis in Q1 and that could have hit them adversely. With focus on product mix change (such as adding resort rooms), maintenance & brownfield capex, new parks coming up every 1-2 years, they should be able to grow their topline in double digit going forward.

Note: Not invested neither SEBI registered.

2 Likes

Hi Everyone,

I am seeing lot of negative commentry here. Here is my viewpoint.

- This management is one of the most honest management in India. This is rear breed in India.

- With Orissa park, they will start making close to 200Cr profits every year. This money should be enough to open one park every year.

- I see in next 5-6 years this company should start making close to 500+ crore profit. Which will be 7-8 P/E, which will be dirt cheap.

- They have managed to increase ARPU at 11% in last 10+ years, meaning in FY13 ARPU was 572 and now it is 1430. This itself is giving you much better returns that an FD in the bank.

Thanks,

Nitin

6 Likes

Hope things work out well for them. I have invested and have positive expectations. One thing to note that they are positioned themselves in very high level with very less competition. The sector is very capex intensive and developing a good network of parks takes time.

1 Like

Wonderla Holidays Q1 FY25 Analysis: Key takeaways!!

Wonderla Holidays faced some headwinds in Q1 FY25, with revenue declining 6% year-over-year to INR 172.9 crores. Footfalls decreased by 9% to 10.02 lakhs, primarily due to external factors like heatwaves, water shortages, and election-related disruptions. Despite these challenges, the company remains optimistic about future growth, particularly with the launch of its new park in Bhubaneswar and ongoing expansion plans.

Strategic Initiatives:

- New park launch: Wonderla commenced operations at its fourth park in Bhubaneswar, spanning 50 acres and creating 450 new jobs.

- Expansion plans: The company is progressing with its Chennai project, set to open in December 2025 or January 2026.

- Future growth: Wonderla is in talks with various state governments for potential new parks in Indore, Mohali, Noida, and Ahmedabad.

- Fundraising: The Board has approved exploring fundraising options to support projects for the next 7-8 years.

Trends and Themes:

- Post-COVID normalization: The company observed some sluggishness in discretionary spending following three years of “revenge tourism” post-COVID.

- ARPU growth: Average Revenue Per User (ARPU) increased by 3% year-over-year to INR 1,680, driven mainly by non-ticket revenue.

- Expansion of SMB offerings: Wonderla introduced new theme dining experiences to cater to a diverse customer base.

Industry Tailwinds:

- Recovery in travel and tourism sector

- Growing middle-class disposable income in India

- Increasing demand for experiential entertainment

Industry Headwinds:

- Weather-related disruptions (heatwaves, heavy rains)

- Water shortages affecting park operations

- Election-related activities impacting footfalls

Analyst Concerns and Management Response:

-

Concern: Decline in footfalls, particularly in Bangalore

Response: Management acknowledged the impact of external factors and is working to recover lost footfalls in the coming quarters. -

Concern: Delay in Chennai project timeline

Response: The company revised the opening date from June 2025 to December 2025 or January 2026. -

Concern: Margin pressure due to new park launch

Response: Management explained the impact of one-time expenses related to the Bhubaneswar park launch and ESOP costs on Q1 margins.

Competitive Landscape:

Wonderla positions itself as a comprehensive amusement park offering a better experience and higher-caliber rides at a lower cost compared to local competitors. The company’s mix of water park and amusement park attractions sets it apart in the market.

Guidance and Outlook:

Specific guidance was not provided, but the management expects to maintain historical EBITDA and PAT margin levels. They aim to recover lost footfalls in the coming quarters and potentially achieve slight improvement over the previous year’s numbers.

Capital Allocation Strategy:

Wonderla is exploring fundraising options to support its expansion plans, with a goal of adding five more parks over the next 6-7 years.

Opportunities & Risks:

Opportunities:

- Expansion into new markets (Bhubaneswar, Chennai, and potential new locations)

- Increasing non-ticket revenue through new offerings

- Tapping into growing demand for domestic tourism

Risks:

- Weather-related disruptions affecting park operations

- Economic slowdowns impacting discretionary spending

- Execution risks associated with rapid expansion

Regulatory Environment:

The company’s expansion plans involve negotiations with various state governments, indicating the importance of favorable regulatory environments for new park development.

Customer Sentiment:

The management’s focus on improving ARPU and introducing new experiences suggests efforts to enhance customer satisfaction and value perception.

Top 3 Takeaways:

- Wonderla is aggressively expanding with new parks in Bhubaneswar and Chennai, plus plans for five more locations in the coming years.

- Q1 FY25 performance was impacted by external factors, but the company remains optimistic about recovery and long-term growth.

- The company is exploring fundraising options to support its ambitious expansion strategy over the next 7-8 years.

5 Likes

An article on slump in Disney theme park revenue offset by Inside Out sequel and Disney+ streaming service revenue.

An interesting insight from the annual report is about the bhubaneshwar park for which lease period is for 90 years and annual lease rent is 6 lakhs per annum, also the total lease rent have been paid upfront in a single go!

13 Likes

This is one of the biggest holdings I have. As we know Wonderla is in talks with various state governments to build new parks. Recently came to know that they are planning a second park in their home state which is Kerala. (Not confirmed yet by company) This Qtr they have spent good amount on Ads which I expect to turn to more footfalls and good Q2 is what will help the stock to go up further.

3 Likes

I also have almost 33% allocation to this stock… Bought around 200 levels… My main question remains why is Co not Going to destination like say Goa where lot of tourist come… Domestic as well as international and weather is good almost through the year… Also might help get better arpu there and strengthen the brand name as visibility is more here

5 Likes

Good. The reason they may not be going to tier II & III towns is a priority issue. I guess, First they want to cover major towns where people with higher disposable income are present. Land & water availability can also be an issue.

5 Likes

People going to Goa may not spend (waste) a day in a theme park unless it’s very unique. Also land prices will be high to setup a theme park.

2 Likes

Why is going to a theme park waste? Also wonderla doesn’t buy land it rents from government…

Goa is an international tourist city. If a tourist, domestic or international, plans a 3 day stay in Goa, he/she might want to enjoy the beaches (North and South beaches) and other historical attractions like fort, church, etc which are unique to Goa rather than spending a day in a theme park, unless it is exceptional like Singapore’s universal studios or Paris’ Disney land. Even people going to Paris may not go the iconic Disney land.

But hey it’s my opinion and it differs from people to people and I may be totally wrong as well.

12 Likes

They may be looking at cities which have a good population - which may choose to visit the park as a weekend/holiday destination. Normally when you visit a place you may not visit a regular theme park there which is also available in many other cities (Something unique like Disney is entirely different).

If the city has a good population, then in turns someone or other might choose to visit it once in a few months.

It is just a guess. Views welcome.

Disc: Invested recently in past 1 yr. Small part of pf

2 Likes

Not invested:

They have a pre-tax loss, but due to the deferred tax, they ended up with profit. They also had a footfall drop.

4 Likes

Yes. Wonderla has again disappointed us with Q2 Results. I listened to the Concall and I am willing to continue hold my investments however I just stuck with one question, if the business is so well, they could have gone for Debt instead of QIP. When they have good margins, they could have afforded this. Is there some uncertainty which forces them to stay away from Debt? QIP may lead to dilution of equity and possible decline in EPS etc…

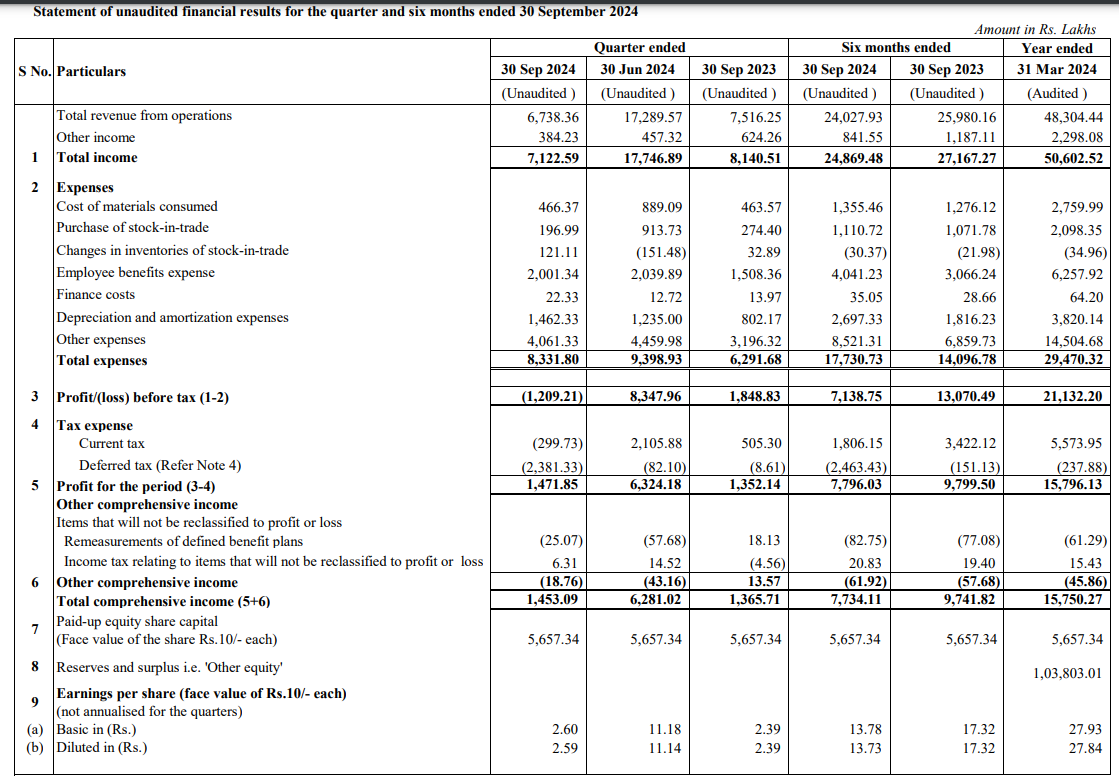

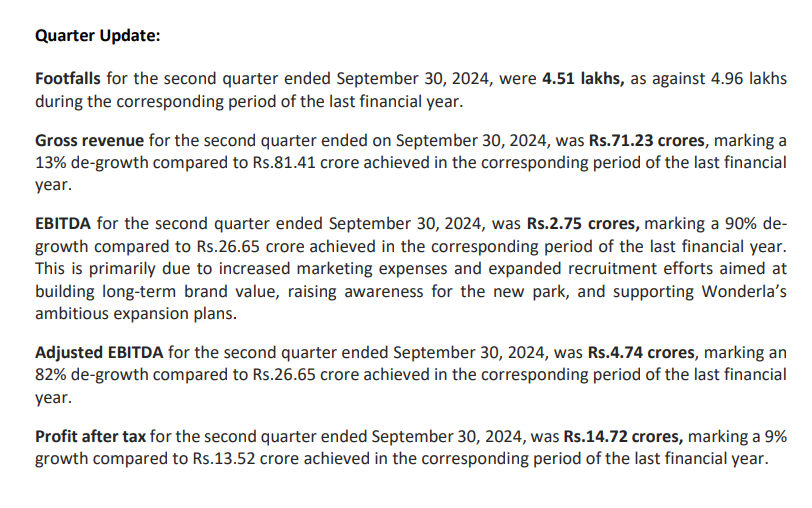

Wonderla Holidays -

Q2 FY 25 results and concall highlights -

Currently operational amusement parks -

Kochi ( since 2000 ) - 94 acres, 56 rides

Bengaluru ( since 2005 ) - 82 acres, 60 rides

Hyderabad ( since 2016 ) - 52 acres, 52 rides

Bhubneshwar ( since 2024 ) - 51 acres, 21 rides

Company makes 30-40 pc of its rides - in house, has a talented set of technicians for the same. Rest are imported

Q2 financial outcomes -

Revenues - 67 vs 75 cr ( down 10 pc )

EBITDA - 2.6 vs 26 cr ( down 90 pc ). Company incurred a one time launch cost for the Bhuvneshwar Park @ 4 cr in Q2. Also had to incur additional hiring costs for the Bhuvneshwar park which further compressed the EBITDA margins

PAT - 15 vs 13 cr ( due deferred tax reversals )

Park wise footfalls, revenues in Q2 -

Kochi @ 1.39 lakh. Revenues @ 19.8 vs 24.7 cr

Bengaluru @ 1.96 lakh. Revenues @ 28.4 vs 31.6 cr

Hyderabad @ 0.92 lakh. Revenues @ 13.5 vs 16.1 cr

Bhuvneshwar @ 0.24 lakh. Revenues @ 5.3 cr

Heavy rains in South India in Q2, landslides in Kerala did impact the footfalls

Added multiple rides to the Hyderabad park in Q2. Spent 15 cr on the same

New Park @ Chennai should go live in Q3 FY 26

Raising 800 cr via QIP - in order to fund expansions in future ( it ll be a mix of Equity 600 cr and Debt of around 200 cr - roughly ). This should be enough for company’s expansion for the next 5 - 7 yrs

A new - large size park in a city like Mumbai / Delhi should cost around 700-800 cr. For a tier 2 city like Mohali / Indore, it should cost them around 200 cr

Intend to add a min of 3 / max of 5 parks in the next 5-6 yrs

Saw encouraging footfalls in the month of Oct 24

Aiming to hit > 3 lakh footfalls in the first full year of operations @ Bhuvneshwar Park

It takes a min of 18 months to set up a park from scratch ( post all the clearances )

Company has surplus land in all their current parks. Company will keep adding rides to their existing parks to utilise the same

Current ticket : non ticket revenues are 75:25. Aim to drive it towards 60:40 in next 4-5 yrs

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

7 Likes