Not sure if the water rides are stopped due to water crisis. Water rides are major attraction during summer.

1 Like

I don’t think so that water rides are stopped as I have search regarding the same on YouTube and found some ramdom person posting videos of there recent trip to Wonderla Bangluru and in that videos they are enjoying water rides n all without any Hassel. There expences are rising like salary n all because they are hiring more n more person at top level and also on operational level of park as Bhubaneswar park is almost ready and going to be operational on 24th may.More things will be clear in today’s concall

1 Like

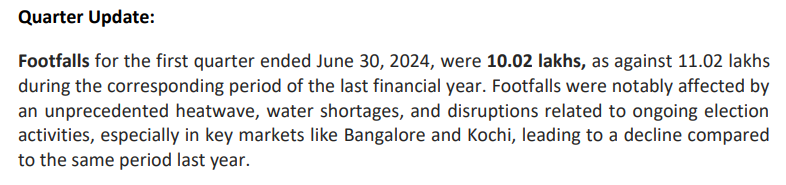

Note the drop in footfalls, this has hit other income in a large way.

1 Like

Time to add more of this stuff as next qtrs this should improve (We have Bhubaneshwar Park added) . Need to find the reason for less footfalls. Will try to research and update here.

More parks getting added in the coming years!

Active discussions with Madhya Pradesh, Uttar Pradesh and Punjab State **

Governments is on track.

Attended the Call - I was looking for an answer for reduction in footfall in Kochi and Bangalore - The reason was reduction in group booking from Schools and Education institutions due to preponement of exams etc… Major footfall reduction is in Kochi followed by Bangalore.

3 Likes

Forgive me, I don’t understand this. Children do not go to outings before exams. How does the preponement of exams manage to reduce footfalls?

Because they have to prepare for exams, their teachers and parents have to adjust for the changes. Considering they have many rides catering to different age groups, and if an entire school which consists of all the classes, the students would at least be in single digit hundreds, just the students also, and if staff and some parents join, the number would be even more. And this is for one institution, so the more such entities, the more will be the footfalls. Maybe resort generates some revenue too from these footfalls. How much such revenues will be generated, and what is the % of such revenues in a quarter’s revenue, I have no idea.

Just some general thoughts, not invested but follow the thread, interested in the business.

2 Likes

Key takeaways from concall -

-The company plans to open 1 new park every year(Huge)

- Does not expect improvement in footfall from existing parks as the are old and already running at optimum level.

- Bhuvaneshwar park expected ARPU to be around 800-1000 and expect margins to get dilute due to this over next year.

- Expect chennai park to be completed by Q3 next year.

- Increase in employee cost in current quarter due to ESOP granted to key management.

- Current quarter looks good but little impacted due to heat waves in bangalore.

My observation - The company has yet again raised ticket prices this season by around 10 percent but struggling to get footfall which is evident by lot of marketing efforts and offers it is running in current peak quarter which were earlier not there in previous years.

Disc - Invested.

8 Likes

Thats right . Hope you got it @Pickett . Families go in April - May and you will see the difference in Q1 Results.

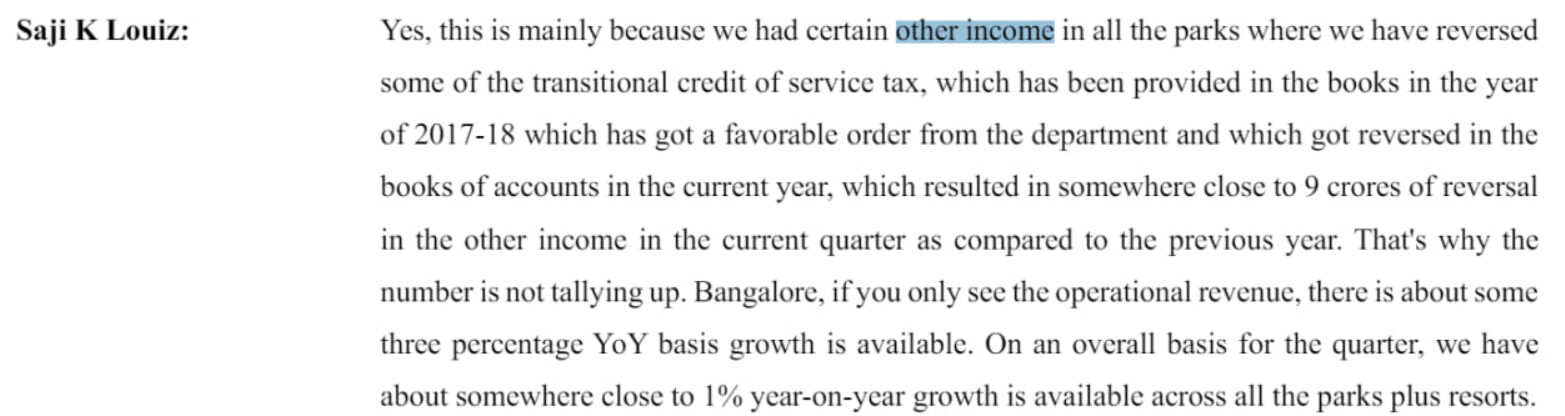

I have been pondering the other income drop, here in the below excerpt from the concall, this is mentioned:

From reading this, does it mean that the gain that they had in 2017 was reversed in 2023-24?

I’m very confused by the whole comment. Can someone help decifer this?

The whole concall is below:

https://www.bseindia.com/xml-data/corpfiling/AttachHis/f1e38cff-6ca8-404c-bc48-080afd42e47d.pdf

1 Like

Wonderla Holidays -

Q4 and FY 24 highlights -

Q4 outcomes -

Revenues - 99 vs 98 cr

Adjusted EBITDA - 42 vs 56 cr, down 26 pc ( margins @ 40 vs 50 pc, addition of new employees for Bhuvneshwar park and salary hikes contributed to margin decline )

PAT - 22 vs 35 cr, down 35 pc

ARPU @ Rs 1349 vs 1184

Footfalls @ 7.09 vs 8.04 lakh

FY 24 outcomes -

Revenues - 483 vs 429 cr, up 13 pc

Adjusted EBITDA - 251 vs 235 cr, up 7 pc ( margins @ 50 vs 52 pc )

PAT - 158 vs 148 cr, up 6 pc

ARPU @ Rs 1430 vs 1243, up 15 pc

Footfalls @ 32.5 vs 33.1 lakh, down 2 pc

Park wise footfalls for FY 24 -

Bengaluru - 12.7 vs 12.04 lakh

Kochi - 10.33 vs 11.39 lakh

Hyderabad - 9.49 vs 9.67 lakh

New Park near Bhuvneshwar to open for public wef 24 May 24. This will contribute 36 days of revenues for the company. This park should be a key growth driver for FY 25

New Park near Chennai to be operationalised in next FY by end of Q2, beginning of Q3. Chennai park is going to be twice in Size vs that of Bhuvneshwar Park

Company believes that drop in footfalls in Q4 were led by advancement in some examination dates @ both school and colleges. Also Q4 LY was strong due to a post COVID bounce

Don’t see much footfall growth in Bengaluru, Kochi in FY 25. Do see some growth in Hyderabad ( low double digits ). Looking at 8-10 pc ARPU growth from these three parks

On a conservative basis - Bhuvneshwar park should clock 4 lakh kind of footfalls @ ARPU of around Rs 900. That translates into an additional revenue of 36 cr or so for FY 25

Looking at Gujarat, PB, UP and MP to open new parks. Will sign definitive agreements post elections. Aim to keep opening a new Park every FY for next 3-4 yrs

May end up raising both debt and equity in case going for aggressive expansion

Expecting Bhuvneshwar park to be EBITDA positive wef FY 25

Company depreciates its equipment and machinery installed in the Parks over a period of 10 yrs

Company ensures a high degree of differentiation wrt the rides / experiences among its parks

Disc: added a tracking position, not SEBI registered, Biased

6 Likes

Moreover, with 7-8 parks in India - won’t the competition increase thus the growth would be a lot tougher, therefore, my suggestion is to reduce it further by Park 8

Below are the latest quarterly results and company announcement

I hope you find these useful

1 Like

Invested (please verify calculations):

We are definitely disappointed.

There is a conference call today, and we hope they have some optimism for us to latch onto.

The company has not excited us for the last few quarters. Of course, there is the expenditure in Chennai and, to a smaller extent, Orissa. Again, we suffered lower footfall and less spending on food. Now, we hear about water problems. Operating profit margin (OPM) is still good but has dropped compared to before.

If the situation is going to be lower footfall at all the old parks, are we looking at chasing a snowball downhill with capital expenditure across the country?

Even the old parks have to remain viable. If not increasing profits, we definitely should not be looking at lowering profits by 25%, especially in our busiest season. Our bread and butter right?

We hope sir has answers for us.

| Growth | YonY |

|---|---|

| Revenue | -6% |

| Other Income | -19% |

| Expenses | 20% |

| PBT | -26% |

| PAT | -25% |

| EPS | -25% |

| OPM | 48% |

1 Like

I believe operating leverage has already played out in this business, for them to grow further from here they will require capex to go live and functional parks.

3 Likes

Really very disappointing results. I was expecting better results due to vacation etc…

Share has dropped around 5% today… not a big fall… an averaging opportunity may be.

Hello Folks,

I have exited the stock recently and would want to share brief update here:

-

Firstly, Did not particularly like Q4FY24 results. The growth was flat v/s Q4FY23, but most importantly there was severe footfall degrowth, flat revenue was only due to very good ARPU increase. So, with recent hirings at top level and additional ESOP cost, EBITDA took a hit.

-

Management in past 3-4 quarters have been stating that these are the best margins and best footfalls we have achieved. While they have confirmed further footfall growth, but they also said EBITDA% would drop a bit as these are at very high levels. Basic screening shows that footfalls were at highest in FY24 and Margins were at highest in FY23. So, there is no element of further upside surprise?

-

Thirdly, the valuations were not cheap (As per my understanding). And earnings growth forecast has been reduced by the fact that they were at peak. So, it did not particularly gave me comfort to hold for longer.

-

And because of all the above + good entry point of 200-220, i have kept a momentum based approach to exit stock if it falls and ride as it kept rising. Also, possibly starting of Odisha Park meant more stress in near term as costs will be front loaded. Hence, had kept tight stop and exited the stock when it hit my SL levels in June when actual NDA results came out.

-

Q1FY25, kind of continued the negative footfalls. Banglore taking a -25% hit on footfalls and other parks too. Ex-odisha the results are -11% in revenue and -22.5% in EBITDA. And things will also not turn immediately given that Odisha park will also need to stabalize to contribute significantly to PAT.

-

By the time Odisha Park starts contributing, we have Chennai Parks cost front loaded when it starts. Obviously, there will be surprise in form of new park announcement, but fundamentally things will look dull for FY25 atleast.

Hence, a combination of above was reason I exited the stock. However note that, the reason for my exit was that I had entered low and wanted to protect gains in case if market corrects a bit. And my choice of not going through temporary dull period (my expectation of FY25).

These are just my views which could go wrong, hope it helps!

Regards,

Mukul Jain

9 Likes

Disclosure: Invested

Please verify for yourselves the below by listening to the concall. If you do see a mistake below, please do let us know here so all of us can benefit.

My notes are not very good, but here goes:

Hyderabad did ok, but not the other 2 parks. This is because of elections, a lack of promotions in Bangalore due to the fact it could have been in bad taste during the heavy impact of water shortages in Bangalore.

The Orissa park is going well, they expect the ARPU to come down once the excitment dies down, but think footfall will hold.

Chennai has been delayed to perhaps Dec 25 or perhaps Jan '26.

They will be going for some kind of funding for the next 7 years, so the promoters are truly devoting their life to this venture, quite reassuring to the investor I think.

However I thought there was a concern on why footfalls fell this badly (-25% Bangalore) and I’m not sure if they know why it is. I worry about the same given we have come short 3 (?) quarters in a row for one reason or another. OPMs are great but I fear a weaker future for now. May be the business is taking a breather.

Wish all here good luck.

6 Likes

Well thought out, Sir, I would think that we may see much better gains in 2026 with Chennai firmly on board. The adventure park they have planned in Blr may also be good for footfalls. We hope so at least.

3 Likes