About the promoter

Womancart’s founder and promoter is Mrs. Veena Pahwa. She is a Delhi University graduate and began her career as a Client Account Coordinator for Electronic Media at Vignette Advertising and Marketing Private Limited. After a period of family responsibilities, in 2015, she established “The Family Store,” a grocery store in Paschim Vihar, Delhi, which she successfully operated both offline and online until the onset of the COVID-19 pandemic.

Following the pandemic, Mrs. Veena Pahwa decided to channel her passion for beauty and style to empower women, not just in terms of their outward appearance but also their inner confidence and positivity. Her vision was to offer customers a straightforward, approachable, and upscale buying experience, which led to the creation of retail outlets providing a unique shopping experience. She actively oversees the design and procurement processes for the company’s own brands.

Ms. Veena Pahwa is on the Board of Directors at Womancart Ltd., Global Holidays Destinations Pvt Ltd., Manommay Ecombiz (OPC) Pvt Ltd., MSV Beautyy Shop Pvt Ltd., MSV Prompt Shop Pvt Ltd., MSV Retaail Fashion Pvt Ltd., Varadda Beverages Pvt Ltd. and Varadda Overseas Pvt Ltd. In addition to her

Mr. Madhu Sudan Pahwa Managing Director and Chief Financial Officer

Both of them don’t seem to have any experience in a internet lead startup in the past or in this

About the company

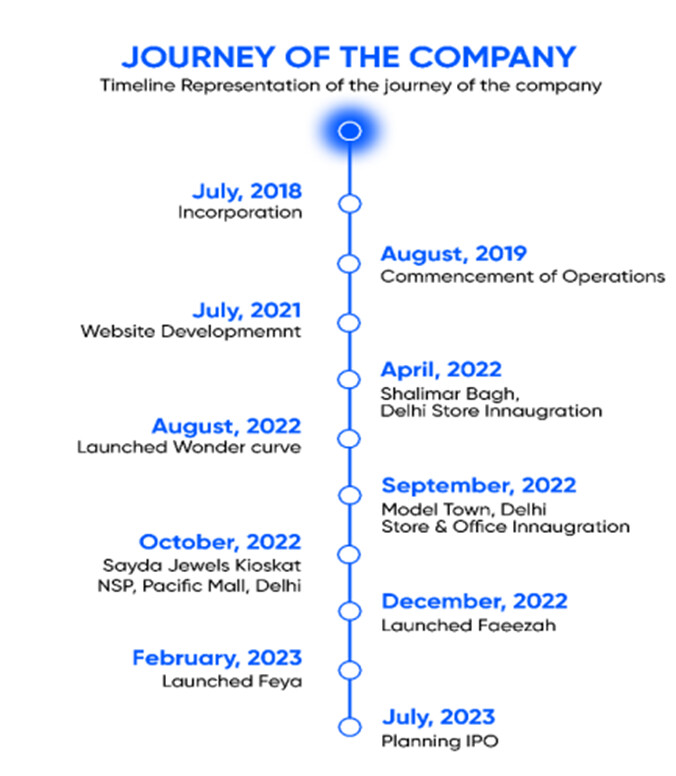

Womancart Private Limited, originally incorporated on July 4, 2018, under the Companies Act, 2013, as a private limited company with a registered office in New Delhi, underwent a transformation to become Womancart Limited on May 19, 2023. This change was executed through a shareholders’ resolution, and a new Certificate of Incorporation was issued by the Registrar of Companies, Delhi, on May 31, 2023.

Womancart Limited operates as a digital consumer-centric retail platform with a focus on beauty and wellness products. They offer a diverse range of classic and emerging branded products for skin care, body care, hair care, and fragrances for both men and women. Additionally, they sell lifestyle brands encompassing makeup, imitation jewelry, and lingerie. The company operates both online and brick-and-mortar stores, allowing customers to make purchases and engage with the brand.

Women’s cart website

The company prides itself on sourcing specially curated products to meet everyday needs, including skin care, makeup, fragrances, and hair styling tools. They have a separate section dedicated to men’s grooming needs, offering products like shavers, trimmers, and beard care items. Womancart Limited is committed to providing an easy shopping experience, excellent customer service, high-quality products, and fashionable essentials from head to toe. Their product portfolio comprises approximately 10,000 SKUs, including their own brand and a variety of national and international brands.

Womancart has transitioned from a high-volume e-commerce reseller to an omni-channel brand house.

Started with a niche focus (Deodorants) on marketplaces, achieving ₹10 lacs/month in sales.

Scaled by becoming distributors for multiple beauty and wellness brands.(Omni-channel & Private Labels)

Digital: Launched own website to capture direct-to-consumer (D2C) data.

They have their Indian website, Their Australian website and Instagram page

It has a good level follower in Instagram more than 30 thousand followersOffline: Established two owned stores in Delhi and a mall kiosk.

House of Brands: Launched four proprietary brands: Wondercurve (Lingerie), Sayda Jewels (Jewelry), Faeezah & Feya (Clothing/Accessories).these brands will give it more revenue than 3 rd party brands

New Categories: Recently branched into Home Decor (diffusers and bedsheets).

- Operational Scale & Efficiency

The company is aggressively expanding its physical and logistical footprint:

Infrastructure: Operates an 18,000 sq. ft. mega-warehouse to support scaling inventory.

Logistics: Successfully piloted a 2-hour delivery model in Jaipur, signaling a move toward “quick commerce” for beauty products.

International Foray: Entered Australia; currently completed 6 months of operations and hosted its first physical exhibition there.

- Financial Performance (FY25 Milestones)

| Metric | Mar-23 | Mar-24 | Mar-25 | CAGR (2-Year) |

|---|---|---|---|---|

| Sales | 9.64 | 29.21 | 58.86 | 147.10% |

| Operating Profit | 0.85 | 3.7 | 9.93 | 241.79% |

| Operating Profit Margin (OPM%) | 0.088 | 0.127 | 0.169 | 38.32% |

| Other Income | 0.01 | 0.47 | 1.13 | 963.01% |

| EBITDA | 0.86 | 4.17 | 11.06 | 258.61% |

| Interest | 0.08 | 0.35 | 1.22 | 290.51% |

| Depreciation | 0.1 | 0.36 | 1.34 | 266.06% |

| Profit before tax (PBT) | 0.68 | 3.46 | 8.5 | 253.55% |

| Tax | 0.16 | 0.62 | 1.31 | 186.14% |

| Tax% | 0.235 | 0.179 | 0.154 | -19.07% |

| Net profit after tax (PAT) | 0.51 | 2.84 | 7.18 | 275.21% |

| Net Profit Margin (NPM%) | 0.053 | 0.097 | 0.122 | 51.85% |

| Cash from Operating Activity (CFO) | 0.49 | -9.82 | -26.52 | NM* |

| Capex {(NFA+WIP) change+Dep} | 0.89 | 2.2 | 13.56 | 290.33% |

| FCF | -0.4 | -12.02 | -40.08 | NM* |

| Total Debt (D) | 1.32 | 6.6 | 14.37 | 229.94% |

| Share Capital | 1.11 | 4.21 | 6.04 | 133.27% |

| Dividend Paid (Div) Without DDT | 0 | 0 | 0 | 0.00% |

| Net Cash Generation | 0.85 | -6.62 | -32.4 | NM* |

| Cash + Investments (CI + NCI) | 0.76 | 4.67 | 14.13 | 331.19% |

the company has grown its sales aggressively although its was done at the cost of equity dilution and sales growth

- Unit Economics & Customer Experience

For a retail business, the return and damage metrics are critical indicators of operational health:

Return Rate: 10–12% of sales. (Note: Standard for fashion/beauty e-commerce is often 15-20%, suggesting better-than-average fit/description accuracy).

Damage Rate: 2–3% of total sales (Low breakage despite shipping fragile jewelry/bottles).

Return Policy: Offers a competitive 15-day return window for online customers.

The companies orders are also growing healthly every year

Over the years the company has diversified its revenue steam

- Key Investment Considerations

Social Media Reach: The company attributes a significant portion of its growth to “outstanding reach” and digital appearance, reducing customer acquisition costs (CAC).

Diversification: The pivot from 3rd party distribution to “Home Brands” (Private Labels) is likely the primary driver behind the 2.5x profit growth, as private labels offer higher gross margins.

Global Ambition: The Australia expansion serves as a test case for a global rollout.

Australian website

Why the company choose Australia for expansion rather than India strategy of the company remains a mystery

The company now has to

Comply with the laws there in Australia

Ensure last minute delivery

Maintain inventory in a foreign country

Have foreign currency risk

In addition the number of people purchasing Indian ethnic ware in Australia will be small about 10 lack people and only half are women

Valuation

For a small cap company the valuations seem to be high at a market cap of less than 200 crores the PE is more than 20 and th book value more than 2 times although rapid expansion may justify the value

Competition

the company is exposed to serious competition from the likes of amazon, Flipkart, Myntra and other sellers from Instagram including celebrity endorsed sellers and speciality sellers of certain products

companies like amazon and Flipkart

can have better delivery system

they have more information on the client

they have more financial muscle to tolerate bad times

however women’s cart can differentiate by catering to one set of customers and customization of products

scaling up of products and other cities is a key monitorable for the company

Negatives

Execution risk dilution risk and funding risk

Preferential issue seems to be under priced compared to market value

https://nsearchives.nseindia.com/corporate/WOMANCART_29122025124036_Outcome.pdf

Collapse of prices and tightening of margins

Rapid growth in new and alternative geographies or business that causes execution risk

Failure of quality standards and risk of reputational damage

The company seems to be trading at higher valuation of 20 times its earnings high for a small cap company

Intense competition from established players

Established players will have huge data and understanding about the customer preference

Expansion and scalability will be a key monitorable in the near future

Promoter warrant

The promoter has issued a warrant for herself at the price of 128 per share this is significantly lower than current market price this implies transfer of wealth from minority shareholders to the promoter although same shares were allotted to non promoters at more than market value

More than 12 crores were raised from the promoter

More than 40 crores from non promoters by preferential allotment

sources

Annual report

SME_AR_28621_WOMANCART_2024_2025_A_1860807_05092025181017.pdf

presentation

https://nsearchives.nseindia.com/corporate/WOMANCART_30102025131757_presentation.pdf

website India

Not invested in the company

Did not use AI to generate information processed with AI Sources Annual report 2025 and oct 2025 presentation