Wintac Limited was started in the year 1987 with the name of Recon Limited and as an offspring of Bangalore Pharmaceutical and Research Laboratories Pvt. Ltd which has been in existence since 1956. The company shot into prominence for launching quality products which were within the reach of common man. Over the years, Recon leveraged its expertise in launching products that encompassed a wide range of therapeutic specialties.

In 2001 – Recon was renamed as Wintac Limited, coined from We INtend TAking Care (WINTAC) its range of specialties includes Large and small volume injectable and Ophthalmic solutions.

They have a Manufacturing Plant at Nelamangala which was inspected by USFDA during September

2011. There were eight observations from the USFDA and consequently they had to suspend

the export supplies to US.

In 2013 company entered strategic alliance with Gavis Pharma LLC promoted by Dr.Veerappan

Subramanian and are now the current promoters of the company with ~55% stake.

In 2014 itself Gavis helped them to fill 20 ANDAs with USFDA . As of now 5 products are commercialized and is being sold in US market.

In April this year FDA inspected the plant with No 483 observations.

Company did sales of 32crs last year vs 18cr as exports to US started last year since oct.

Interesting thing is on sales of 32crs they recieved ~38crs as advances from customer. I believe they sell products to promoters other holding co Somerset Therapeutics, LLC which then markets it to USA.

Verrappan subramaniam the current owner of Wintac ltd has an impeccable track record of creating a business from scratch, growing it and then selling it at huge premiums.

In 1997 he strated Kali labs which was sold after 7 years for $150M

Then in 2006 he strated Novel labs and Gavis Pharmaceuticals. This company was thensold to Lupin foe $880M !!

In 2015 he has started another co Somerset therapeutics llc and calls wintac its affiliate. Somerset already had filled 25 andas and is working on 30+ molecules.

I think wintac provides an excellent opportunity for side car investment.

If there is a possibility of exponential growth - this high valuation can be justified. Caplin point could be recent pattern of FDA-approved injectible player making big. Appointment of Dr. Mandar Shah is a positive event. But will Somerset Therapeutics held privately by promoters will allow Wintac to earn super normal profits?

Shareholding pattern: Old and New promoters hold close to 90%. Retail only hold 10% or so.

Company’s board is meeting on July 27th to discuss about Rights issue for investment.

Mkts might have liked the fact that Wintac has an FDA approved site with 0 observations in an audit held on April this year.

Also as its been 3 years of filling of Dossiers, mkts are expecting lots of approvals this year. 2 products got approved this month alone.

I agree that as of now its a pure manufacturing unit with 0 own branded products, margins will be low. Only management can clarify how they want to take this company ahead.

Somerset Theraps receive Tentative approval for PALONOSETRON HYDROCHLORIDE, Helsinn Healthcare SA’s brand Aloxi who’s exclusivity is set to expire in Nov 2017.

US sales of Aloxi totaled more than $500 million in 2015.

WINTAC LTD sales consist of job work charges paid by SOMERSET ,raw material supplied by someset ,Hence calculating valuation based on sales is wrong concept ,Globally Injectble business commands higher value (recent Baxter buyout of Claris inj biz).Wintac will do very well in next 18-24 months .

As Gavis out of non competition clause period from LUPIN ,i am expecting much aggressive steps from SOMERSET which inturn benefit WINTAC .

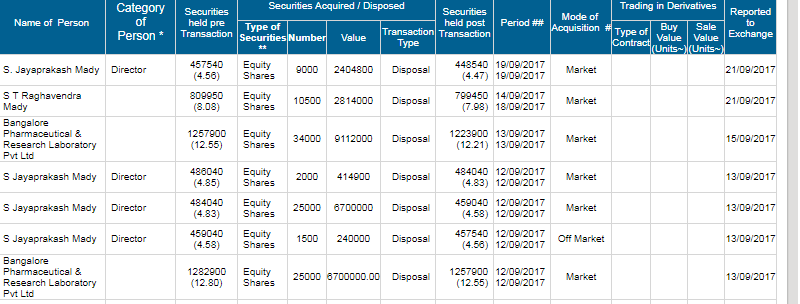

Are they done with it ?

Will they continue selling further?

Who has bought those shares ? General public or some HNI ?

Why Somerset is not interested in increasing its stake when old promoters are selling?

Why there is no representative on the Board of Wintac from Somerset ?

Meanwhile, another product has been launched, total products now marketed 8. ANDA filings pending 23.

Also Somerset is in process of setting up its own R&D in USA. What does it mean to Wintac ? Will listed entity get business from the products developed in that R&D ?

Old promoters are gearing up for rights payment hence they sold , now they won’t sell becaz right issue is deferred .

Looks like some HNIs bought don’t know the name , looks like now Somerset may convert their unsecured loan towards preferential ( its my wild guess ) can increase stake by 10% from current levels .

Don’t have clue on Somerset R&D if they are doing they will rope in wintac as partner at least low end research .

Have anyone studied or know the implications. The promoter proposed 220 per share as part of delisting. If a minority shareholder does not want to sell at that price, what happens ? Any others thoughts of wisdom here ???

The last two quarters for the company has been very good in terms if both sales growth and profitability. Management also plans to raise funds for expansion. Looks good at current valuation