WHY INVEST | GET YOUR MONEY TO MAKE MORE MONEY

Posted on November 22, 2010 by Donald

Why Invest? Get your money to make more money and build long-term wealth. In the process you beat inflation, achieve financial goals, and provide for a comfortable retirement.

Why Invest at all?

Why invest? This came to me sometime in late 2004/early 2005 as I strongly felt the need for making my money work better for me. We were blessed with twin daughters, and full of hopes and dreams.

I was transforming to become more financially responsible and aware. No one needed to educate me on why invest, as I suddenly realised that to achieve these dreams, I needed to shed a bit of my happy-go-lucky attitude and set longer term financial goals. And to achieve these financial goals, I needed to invest!

Investing to me, is focused primarily on making my own money (work harder, and) make more money for me. It is clearly about long term financial goals. As I started reading up and thinking more about building long-term capital, certain simple why invest basics became very very clear to me.

Time Value of Money

Like most things in life, the early bird catches the worm! I understood I was already late into the game. Realised I could never play catch up – even if I doubled the stakes – compared to having started just 10 years earlier.

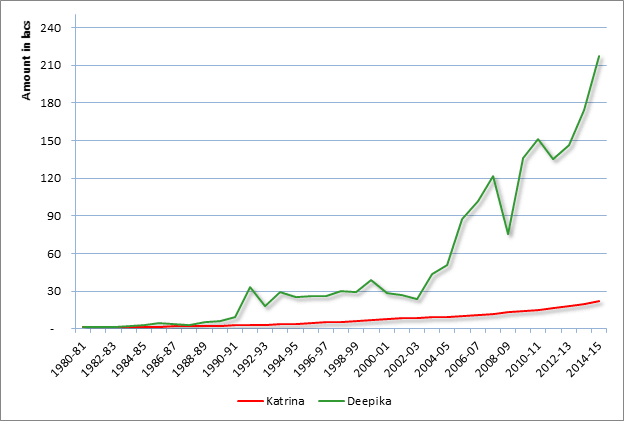

Consider the graphic below. Suppose you start early at age 20, invest Rs.20,000 yearly for 10 years in a safe government-backed instrument like PPF (Public Provident Fund) and forget about it-just let it lie in the bank till retirement. And somone who wakes up somewhat later in life, at age 31, and starts investing double that amount Rs.40,000 every year for 30 years, till he reaches the age of 60.

At age 60 You, the Early Starter would have invested just Rs. 200,000 and seen your investment grow to ~Rs. 3.4 million, and seen a return of 16x. Someone like me who woke up later, will have invested a not inconsiderable Rs. 1.2 miliion, but seen only a 3x return!

Wished I could start the game all over again? You bet, I did! Understood perfectly this aspect of time value of money or what is also called the power of compounding. The longer your money remains invested, the better it works for You! Why Invest, became a no-brainer.

By now my mind had started ticking! Hey wait, what if I could make my money work just a bit faster?

Compounding at different rates

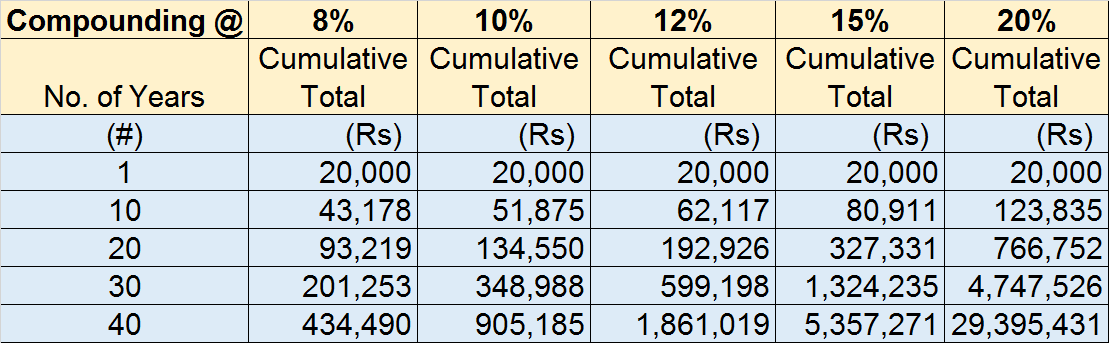

It appeared to me now hey, there are other financial instruments too. If I can make my own money work just a bit harder and faster, perhaps I could play catch up? Lets see how the figures stack up.

Now this was getting interesting. Compounding at just 2 percent more per year every year for next 20 years made for a sizeable 44 percent difference in overall returns. And over 40 years the 2 percent difference more than doubled the returns! Why Invest, indeed!

Now I had learnt my math in school, and knew this is due to the power of compounding! But had I ever worked figures through like this? The miracle of the power of compounding ensures that our investment makes money and the return on that investment makes some more money – keep it that way for a number of years and our investment quickly starts exploding. The more the time our money remains invested and/or earns a higher return, the higher the trajectory of our returns graph.

The Thumb Rule of 72

How long will it take to double my money? From a why invest novice, someone was getting greedier here!

The Thumb rule of 72 comes in handy here. Just divide 72 by the interest rate and you have the number of years it takes to double your money, roughly. So if we are getting a 8% interest rate, it will take 9 years. And at a 15% rate, your money doubles in roughly 5 years. Use a calculator, or an excel worksheet to Test this! Its an amazing thumb rule to keep in your head.

So the next time an agent comes to you, preaches why invest, and talks about doubling your money in 10 years, you know that it means compunding at a rate of 7.2% only. And that you have better options. On the other hand if he is promising the moon, you know how to bring him down to earth with some quick incisive queries.

Other Why Invest considerations

There are a few other considerations too.

Post-tax returns

Many instruments are subject to tax, while some are not. I might be getting a nice 9% annual return on say my fixed deposit, but what is my effective post-tax return? Probably no more than 6.5% compounded annually. You know that’s a paltry return vis-a-vis some other risk-free return instruments, right?

Real Returns – Inflation

And there is the bigger factor of inflation. Inflation, measured as an annual percentage increase, is a sustained increase in the general level of prices for goods and services. As inflation rises, every rupee you own buys a smaller percentage of a good or service. None of us could have missed (even if someone else buys our groceries) the high inflation figures cited by the press in 2008 – so what happens to my real rate of return? Post-tax return minus inflation? While 2008 saw inflation figures topping 11%, the long term average rate of inflation is ~5% in India.

With a 6.5% post-tax return and a 5% inflation figure to absorb, my real rate of return was zilch. I didn’t need more pointers on why invest. Do you?

Different Investment Options

Now that you are better informed on the why invest proposition and the horrifying real-rate of return, you sure want to understand more about the common investment options available to us in India, the pros and cons, taxability, risk and typical return levels associated with each instrument.

Certificates of Deposits

These are short-to-medium-term interest bearing, debt instruments offered by banks. And are low-risk, low-return instruments. There is usually an early withdrawal penalty. Fixed deposits, recurring deposits etc. are some of these.

Average rate of return is usually between 5-9%, depending on duration/instrument. Returns are taxable.

Bonds

These are fixed income (debt) instruments issued for a period of more than one year with the purpose of raising capital. The central or state government, corporations and similar institutions sell bonds. A bond is generally a promise to repay the principal along with fixed rate of interest on a specified maturity date.

The average rate of return on bonds and securities in India has been around 10-12% p.a. Returns are taxable.

Public Provident Fund (PPF)

One of the best instruments available. Must have in your investment portfolio. Scheme can be opened with SBI, leading Pvt. Banks, and Post offices. This is a long term investment vehicle with a term 15 years. Maximum deposit in a year Rs. 150,000 with the current rate of return fixed at 8%. It’s a good idea to first maximise this Rs. 150,000 limit every year before putting surplus money into other investments.

Why? For one, because of the longer term you can unleash the miracle power of compunding to good effect here. Besides its a tax saving instrument, completely safe, risk-free government guaranteed instrument. Returns too are currently, tax free.

Post Office MIS (POMIS)

This is another popular scheme among those who need some regular monthly income, say e.g. Senior Citizens. You may not need the regular monthly income, but hey you could put that regular stream of cash to other investment avenues, such as a reputed mutual fund SIP, compounding at a higher rate, ofcourse!

Again a risk-free instrument you can invest with at Post Offices. Maturity period is of 6 years, with current rate of interest fixed at 8% compounding. Automatic credit facility of monthly interest to a linked savings account at the post office. There is a bonus 5% payable on maturity, so effective compounding return goes over 10%. Returns are taxable.

Stocks

Investment in shares of companies, is investing in Stocks. Stocks can be bought/sold from the exchanges (secondary market) or via IPOs – Initial Public Offerings (primary market).

However unlike Bonds or Certificate of Deposits, investing in stocks isn’t risk free. The market returns over the long term is dependent on the company’s business performance – after all buying a share is a part ownership in the company! If you are going to trust your investment with a company for the longer term, you need to be reasonably sure the company will stay in business for next 10-15 years, and profitably! Investing in shares is not for everyone, requires hard work, a lot of discipline and patience to make a success of it. Else all the analysts would be sitting at home and rolling in the moolah, right!

Having said that, history shows us that investment in quality stocks have proven to be the ideal long term investment. On an average an investment in stocks in India has provided returns of 15-25% p.a. over the medium to long term. Dividend Income and Long Term Capital gains (>1 year) in India are currently, tax free.

Mutual Funds

These are open and close ended funds operated by an investment company which raises money from the public and invests in a group of assets, based on a published set of objectives.

Investing in Mutual Funds provide benefits of diversification (investments spread over a larger number of stocks and thus lesser risk)and professional money management -they have the team of researchers and analysts to pick the best stocks for you.

The rate of return again is market-performance related; generally substantially more than what is earned in fixed deposits. Each mutual fund has a rate of return dependent on how well its stock-picks have performed in the market.

Good Mutual funds in India have given a return of 15–20% p.a. over the long term. Dividend Income and Long Term Capital gains (>1 year) in India are currently, tax free.

Others

There are also other savings and investment vehicles such as gold, real estate, commodities, art and crafts, antiques, foreign currency etc., which too can be considered.

Wealth Creation studies in India

Finally as I dug in more on the why invest case, I was lucky to come across the extensive Wealth Creation studies conducted and documented by Motilal Oswal on the most consistent wealth creators in India.

That was an eye opener for me as I learnt how some of the best and trusted names in India have delivered more than 30% compounded returns annually (with all dividends re-invested), over the last 15 years and more. Names like HDFC, Infosys, ITC figure here – but more on that, later.

Using the thumb rule, I knew a 30% compounding rate means doubling the money in 2.4 years. Amazing. I was even more astounded when I used the excel sheet to work out that with 30% compounding, an investment of Rs. 20,000 in ITC 15 years back and left untouched, would have grown to Rs. 1.02 million, or grown over 51 times! Why Invest I asked no more, I became a convert.

As I digested this better, I resolved to gift my wife 100 ITC shares, for her next birthday. To her credit, she didn’t quiz me on why invest! But you are, I know, I know …there are no gurantees, but what the heck, that smokers will keep smoking is a good enough bet, or what?

Well that’s the run-down on some important basic why invest realisations that convinced me why I should invest and made me a committed long-term investor. Hope, it is equally convincing for you too.

Related content

How to Invest |Understand Return and Risk |Risk Return analysis

How to Invest |Return requirements |Risk tolerance |Your Investment profile

Where to Invest |Asset Allocation |Portfolio diversification