This has been a trend with most established large appliances players IMO. Plus recently there has been a surge in the number of players entering this field like Voltas entering this space with Voltas-Beko, Lloyd launching refrigerator segment, RIL bringing Kelvinator, BPL back etc. So, there is huge competition. Also, there is inflation of component prices which has forced OEMs to raise prices resulting in market cap erosion.

Not exactly comparable as they are into small appliances barring Air Cooler.

I believe you should compare Whirlpool performance w.r.t their focus segments refrigerators and washing machines. In AC they have a tiny market share, and in water purifier segment they are just beginning.

Personally, we have recently bought an washing machine replacing our old Whirlpool top-load. I wanted to buy an Whirlpool one this time also, but Samsung / LG seemed to be more value for money, and so finally bought a Samsung one. I am not sure how Samsung / LG can give such value for money. No idea about their margins. In Whirlpool, I am aware that their margins have been industry best in the last few years barring this pandemic-ridden times.

Agree with this. They need to keep their focus on these segments only, and maybe strengthening parts of these segments where they are not at the top like front-load washing machines, high-end refrigerators etc. And focus less on newer segments like dishwashers, air purifiers, water purifiers etc where they were so keen on entering without much preparation. They have also recently raised their stakes in Elica PB India, which I didn’t like at a time when they are facing existential crisis in the segments where they were successful.

Disc: Invested in Whirlpool, Voltas, Havells, Bluestar.

Isn’t Johnson the Indian manufacturer partner and Hitachi the brand? I don’t track it too closely but that was my impression. I have also seen a brand called ‘Ryoku’ in the market which is a Johnson own label. That affects the valuation perspective for me - as it’s purely an AC play (like Amber in contract manufacturing) and also not MNC management and R&D. I have seen a bit of fridges from Hitachi, but I think they are very small in the space - I expect the leaders to continue doing well in refrigerators.

On Havells - I see it more like an evolving FMEG play but the business also has several other products like wires and switches ans quite a good percentage of it. I keep it in the same pool as a Polycab (maybe a more evolved version of it). I think it has a long way to go before being in line with white goods leaders.

Voltas not a fan of the product range or categories they are in. The brand perception I have seen in people around me also sees it more like an economical brand - and it lacks pricing power in my opinion.

My product experience with the ACs and refrigerator has been good for Whirlpool and with service.

All that said - not that Whirlpool has it in abundance - but it was the best of the lot for me and hence the portfolio allocation - driven by a desire to be invested in consumer durables.

Johnson Hitachi AC is very much an MNC brand with Johnson Control being a leading US based Automation/tech company and Hitachi a Japanese giant. I believe its a 60:40 partnership in India between the two.

I did some checks and apparently it seems that Ryoku is a sub brand name of Hitachi AC owned by the same Indian parent - Johnson Hitachi AC. The manufacturer/publisher in below link mentioned that

Fair point - as I said don’t track Johnson Hitachi in detail as I am already invested in Amber and that’s good enough for me from the AC perspective.

Ryoku - good to see that it is co branded now with Hitachi - it makes sense with the 2 partners. A couple of years back was not the case though. I only wanted a front unit changed for an AC and Ryoku was suggested as an option by the AC guy (that got me interested in the company). But there was no Hitachi branding on the remote or the AC for the product. Just said manufactured by Johnson Hitachi. That has obviously changed now as per your link.

I agree to all your points, however only Fridge and washing machine cannot make our investment much fruitful here going forward. As you rightly mentioned, Voltas, RIL etc are all gearing up to sell their own brands via their ecommerce/physical ecosystem and in such environment the vision and strategy of this MNC would be very very crucial in next few years - Any idea what they want to become and what are their future focus areas apart from these two?

Also, regarding good margins, one reason could be they have decent backward integration (correct me if wrong) and another is that I do not see them pushing their products via any Physical/online channels. You find sponsored products of Panasonic over Amazon but never a Whirlpool, Similarly if they do not have th einfra to service Water purifiers at large scale, they can use Rescue service of Reliance digital - I must say their service is even better than what the OEM brands provide…but to push their products via this physical channel would mean giving better cut to the retailers? (I am no expert here and just thinking loud). They dont seem to do any of this and their own network and ecommerce is many years behind to keep pace with the Tata and RIL ecosystem…if not decades…

What are they doing to cater this new upcoming challenge for coming decade?

I am not sure and hence concerned…

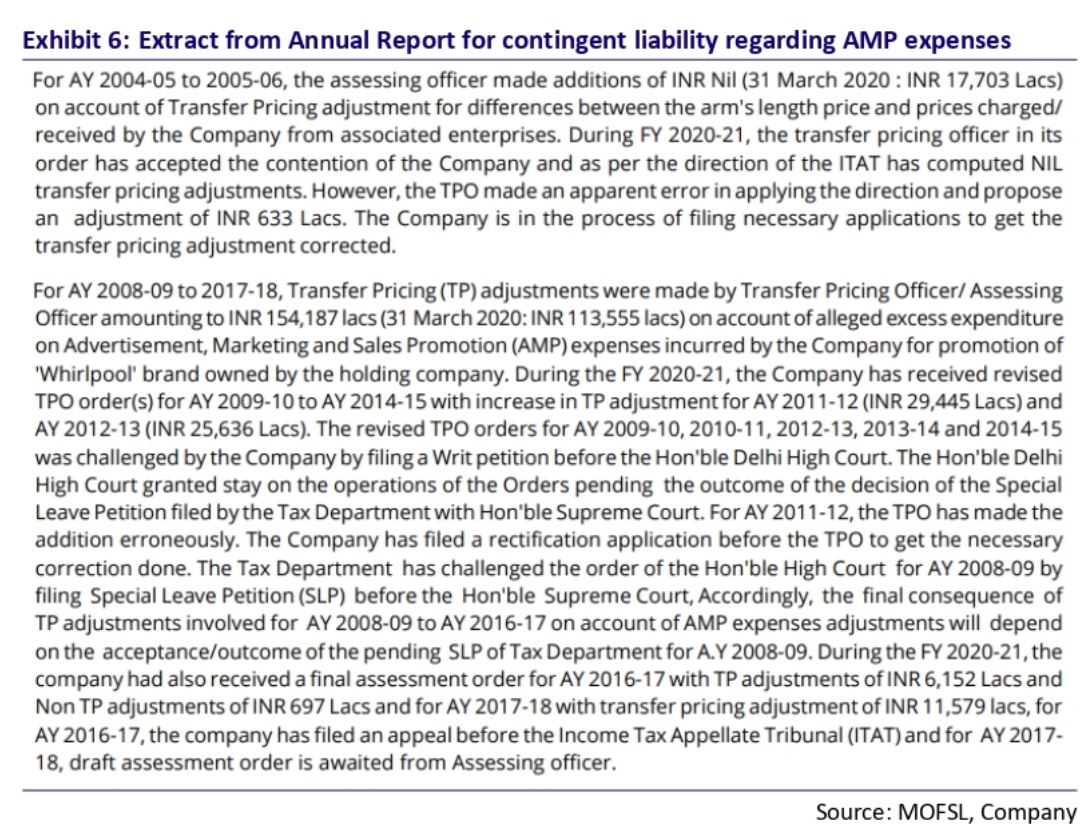

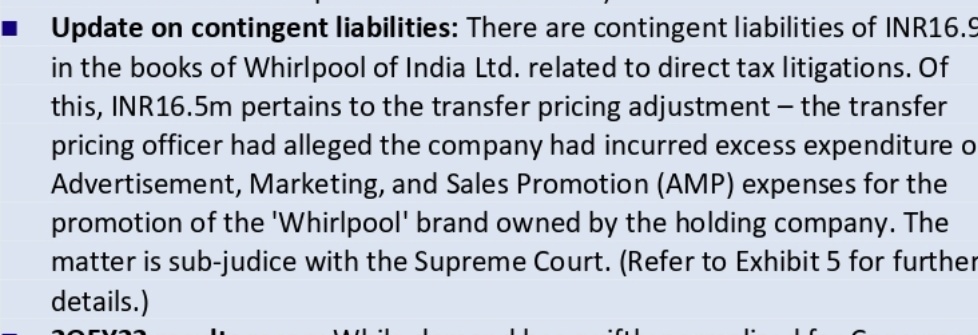

Generally, most of these MNC’s have these cases with respect to AMP expenses on the customs side or the income tax side. Many cases for MNC’s pending before CESTAT and lower authorities also with regard to AMP expenses and adjustments thereof.

Disc: transactions undertaken in whirlpool in the last 30 days.

Isn’t it still too expensive (trading at 30x 2024) for a consumer durable company.

Trading below historical level may not mean a lot if it was too expensive to start with.

Whirlpool - a MNC, play on consumption story and super underperformer in 2021,used to be market quality bucket candidate ( still is probably as no major long term thesis changes)

Sales growth has been good across all periods, has not de grown even in 2021 though many in industry did, Profit under pressure inline with industry trend.

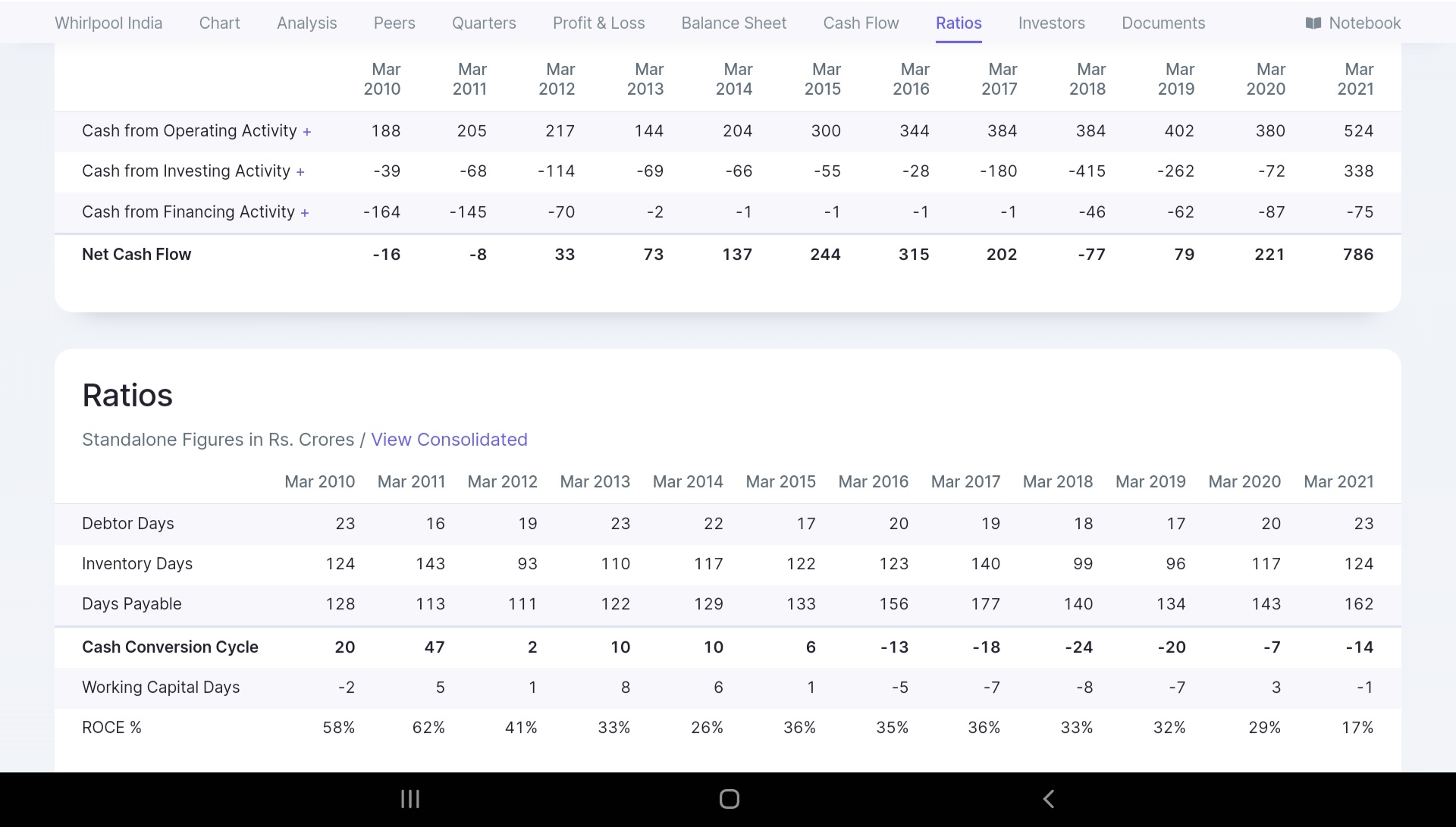

It is been a negative working capital, Solid cashflow machine all throughout, reason behind long term average 55 PE.( screener data)

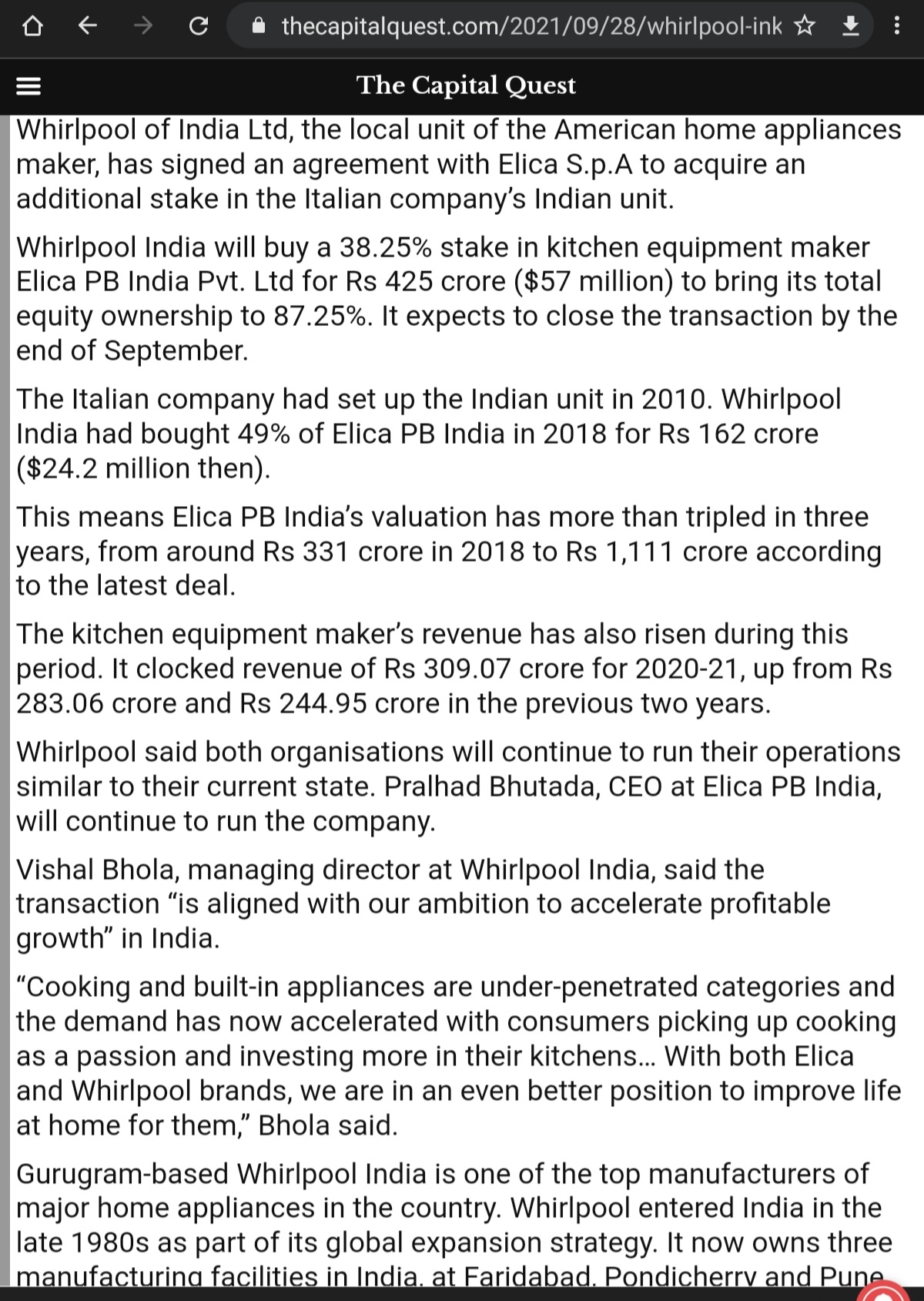

Appears Elica acquisition(90%) is at very attractive validation ( approx 650 cr) for a fast growing consumer brand with approx revenue of 400 cr vicinity in FY 22

Valuations

TTM it is at 6200 cr revenue, opm 8% at 475 cr, PAT 290 cr , Q3 is generally best in lot

TTM under long term average margins for similar revenues, opm at 11% at 700 cr, pat would be 500 cr+

At nominal 10% topline growth in FY 23 , revenue would be 7000 cr+, opm at 12% around 840 cr , pat around 600 cr+

For FY 23, add about 400 cr revenue from Elica, at similar margin it adds 40 cr in bottomline ( remember it’s a high growth segment and irrespective of covid has grown 20% in FY21 as well to 310 cr) - Here details

That is FY 23 , 7500 cr rev and 900 cr opm, 640 cr in bottomline - at long term median avg of 55 that gives us 34000 cr+ mkt cap, cash in books would be 2500 cr+ ( 500 cr per year type and after elica acquisition they Currently have 1500 cr). Current market cap is 23000 cr. That is 35-40% upside when margin performance revert to mean

Technicals

On long term support levels and bouncing back with good volumes on weekly

Don’t know for sure as to what caused recent steep fall from 2300 to 1800 - multiple factors seem to have converged

Margins trajectory is weak, but so is case of rest of industry, should mean revert eventually given secular consumption growth in home appliances

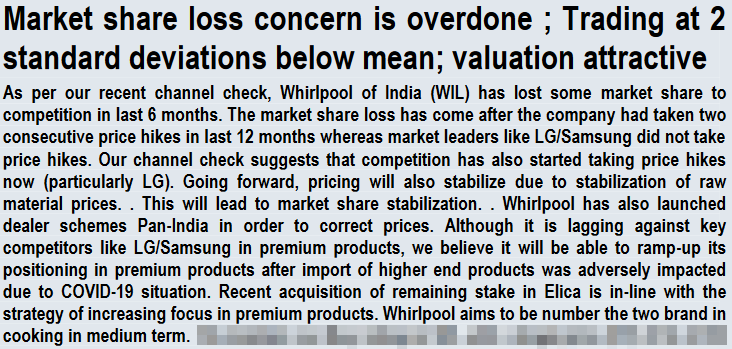

Apparently they lost some mkt share to LG/Samsung- as they took price hikes and competition didn’t, now competition increasing prices as well and counter measures from Whirlpool - article in thread above

Apparently tax evasion at parent ( Whirlpool usa) level, though this doesn’t impact India unit,

Competetitive intensity and ability to retain/grow mkt share in core segments of washing machine and refrigerator- innovation, quality and customer services driven - key monitorable

After Old MD DESOUZA MOVED TO TATA CONSUMER NEW CEO MD is more corporate employee type. Does not consider minority shareholders are stake holders and rarely take interviews or con calls…he thinks this is just a division of whirlpool ltd so leaves it to corporate PR …stock never recovered after last CEO left. Needs a mamagement change for sure …poor sales and poor profit in high competetion … no focus of exports which should be part of their plans . Does not want to roxk the boat internally…

So the parent has decided to offload 24% of the company and the market is reacting negatively to the same. Can someone throw light on the pros and cons of this decision?

I think overall given WHirpools Indias slow growth it will be OK for parent to offload shares . It will increase free float. Also they will be more open to external growth now that it’s a 51% sub interms of maybe allowing contract export to group to gain more sales…

One of the issues Whirlpool India has is that group allows them to only make products for India ? With dilution , and depending on who is the buyer offcourse we can hope that WIL will have greater freedom to supply as contract partner to more locations outside as well as have more choices to manage costs in business decisions. Who ever is acquiring parent stake is not going to sit …they will excert pressure to relaease value and push them to deliver more results

Hi Niraj(@niraj) - Would appreciate and love to hear your evolved views about Whirlpool, touching upon recent MD change, sales stagnancy post COVID, OPMs mean-reversion, right to win in the new categories [AC, Purifier, Dishwasher] etc.

My observations from the AGM transcript of recent yrs. are as below:

What’s Interesting?

Least margins in the last 10+ Yrs. | Contributing Factors: Loss in volume due to pricing index challenges compared to the competition, raw material inflation, recent rollback in pricing, regulatory impact. With lower commodity prices, cost reduction initiatives and expected volume growth esp. in the premium segment shall restore the margins in the medium term.

Growth Drivers:

Growth in overall per capita income, Middle class boom and lower penetration rates

Replacement Demand

Scale up of the new categories [AC, Water Purifier, Microwave, Dishwasher]

Launch of the Front Load Fully Automatic Washers

Kitchen proposition under Elica brand with 20% revenue growth rate

Focus on Premiumization of the core categories [Ref, washing m/c | 85~90% of the revenue share | LG and Samsung are the market leaders]

I am not updated on whirlpool from more than 02 years now since i exited my position completely in late 2021. I will still try to explain my evolving understanding regarding this sector over last few years.

First of all, the 02 most important traits which are required for sustainable weath creation for a very long period of time (decades) are megatrends and leadership (explained very beautifully by Mr Utpal Sheth of RaRe enterprises). Consumption is one of the biggest megatrend in india and it will remain so for foreseeable future because India is such an under penetrated market and now growing one of the fastest in the world (combination of low base and very high growth makes consumption in India one of the megatrend). You can also call it a sector with long term tailwinds or a sector where Total Addressable Market is very large and growing. Whirlpool ticked this box for me back in 2020.

Story is very simple as of now. Now it comes down to the second trait which is to find out companies which exhibit leadership qualities among these megatrend sectors and themes. These factors are also simple to analyse by asking basic fundamental questions like

Does company has high market share and is compamy gaining market share from peers? (growing faster than the industry)

Company margins are volatile or stable over long periods of time across cycles (commodity element or brand).

Are return ratio like ROE, ROCE significantly high and no reduction in ROCE after deploying incremental capital in the same business? (This will tell us if growth is coming by going down in value chain or by going up, basically capital allocation strategy of the company).

How are margins comparable to peers? (May not necessarily be high but better than peers. Amazon and APL apollo have created great businesses even if margins are quite low because of better efficiency and inventory turns. So, return ratio remains high)

Are company products susceptible to technology change? If yes than what is the attitude of company towards R&D and keep developing thier own products for better.

Does company has a very strong moat (either supply side or demand side or both).

The answers to most of these questions in case of Whirlpool were not very positive. Hence the exit (obviously i realised this over a period of time after giving sufficiently longer rope and did not act on a very short term performance).

Now coming to third part of my understanding. Consumption remains a megatrend but finding companies which exihibit leadeship qualities is the key. There will be many sub sectors among consumption where no company will exibit such qualities. Few industries and sectors are just gruesome and difficult businesses. Consumer durables like refrigerstor, washing machine and air conditioners may be simply selling like commodities. Reasons can be multiple like excessive competition, no product differentiation other than cost etc but leave those reason for some other day, that will be beyond the scope of this write up. Available data point towards commodity nature of business among these products.

Coming towards last part. Understanding of profit pools is important. We have to understand that in any particular industry, there will be multiple entities responsible for bringing a product from factory to end user. Somebody may be supplying a critical part, somebody may control the distribution and the supply chain (e-commerce companies), somebody may own the the customer (platform companies). These are just few examples. We have to understand who is making the highest margins or who get to keep the highest amount among this entire value chain.

Disclosure: No holding. exited long time back. Found better opportunities in retail like Aditya Vision, Redtape and Senco gold.