Whirlpool - a MNC, play on consumption story and super underperformer in 2021,used to be market quality bucket candidate ( still is probably as no major long term thesis changes)

Quick look at long term performance

-

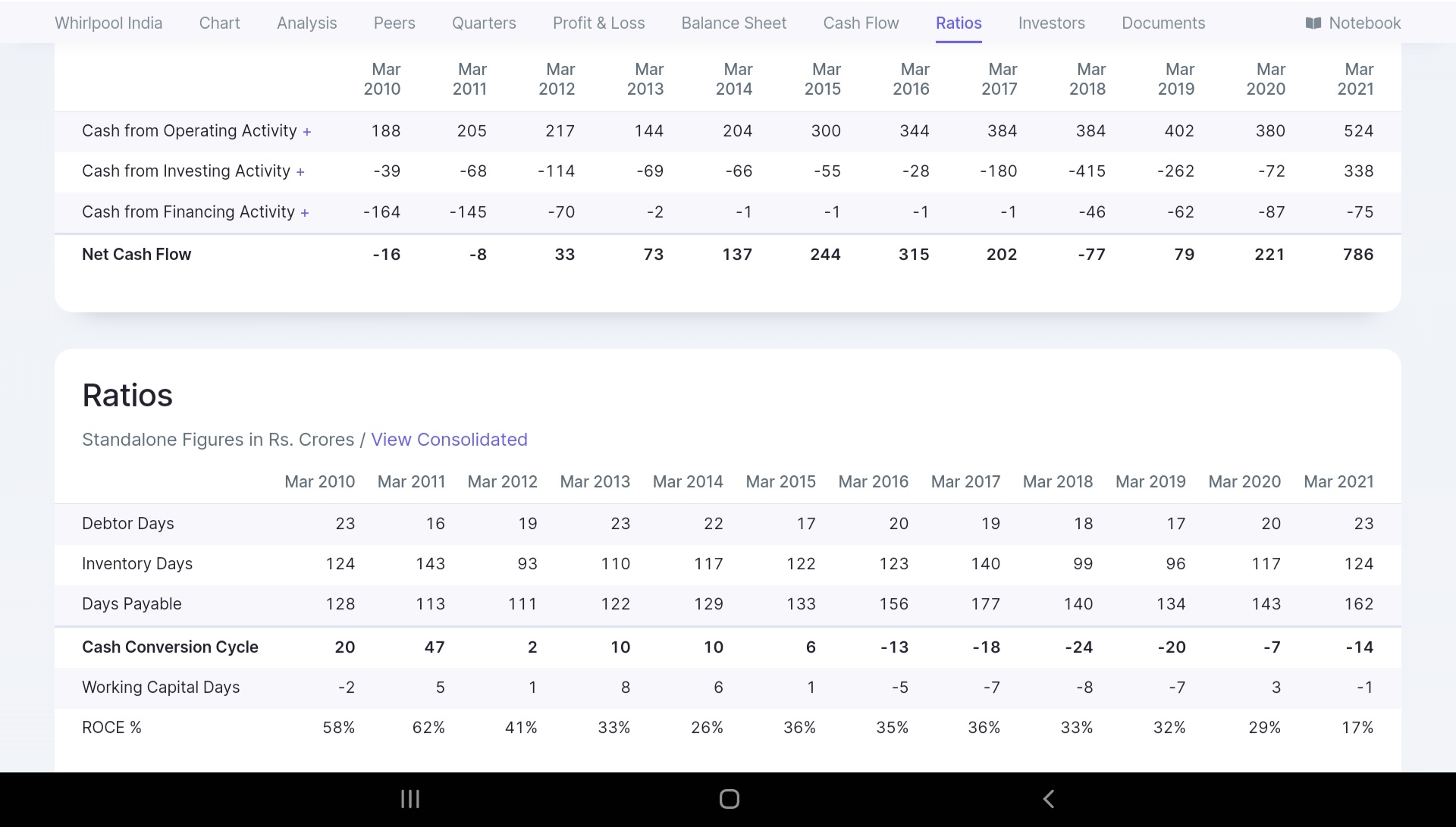

Sales growth has been good across all periods, has not de grown even in 2021 though many in industry did, Profit under pressure inline with industry trend.

-

It is been a negative working capital, Solid cashflow machine all throughout, reason behind long term average 55 PE.( screener data)

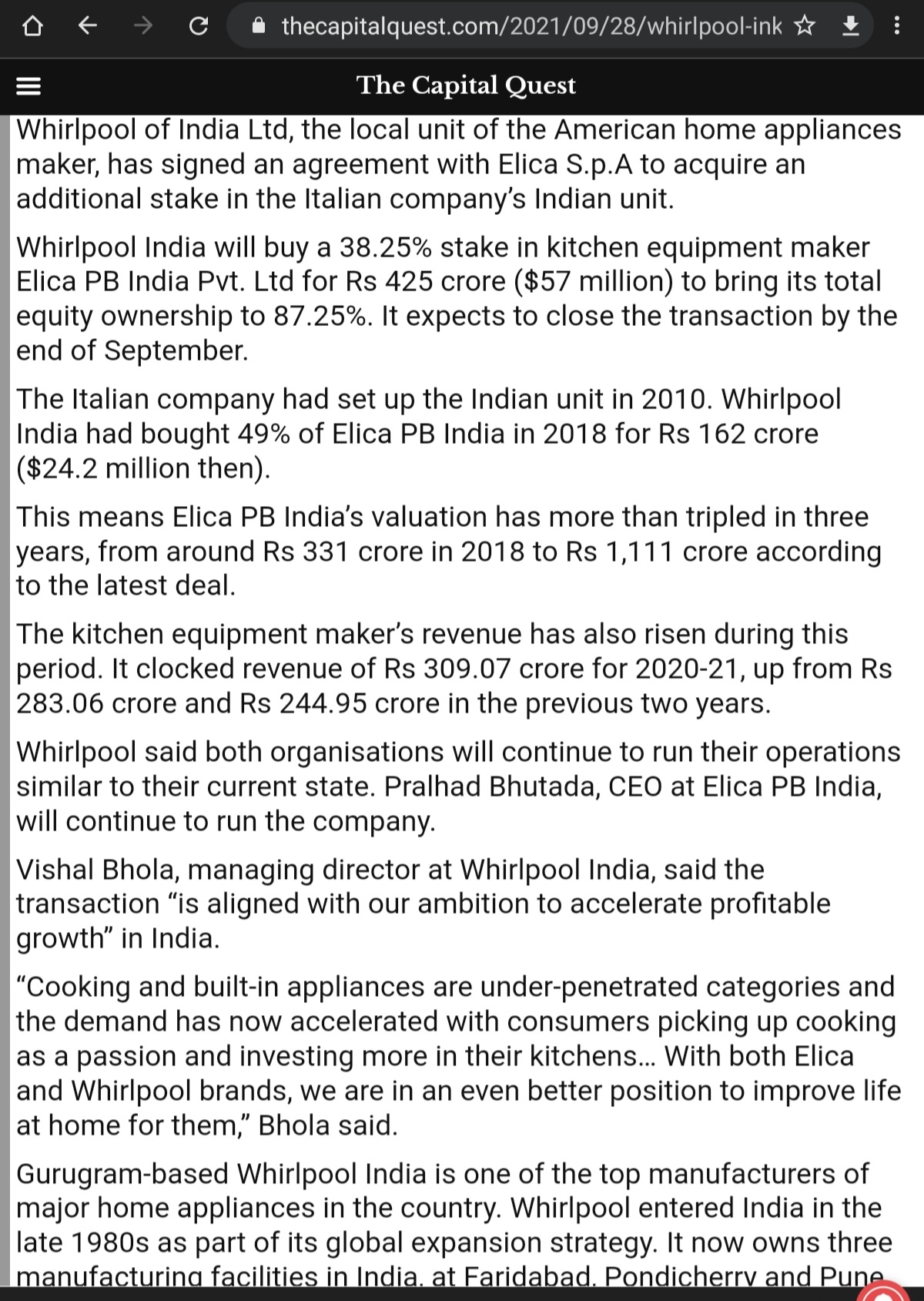

- Appears Elica acquisition(90%) is at very attractive validation ( approx 650 cr) for a fast growing consumer brand with approx revenue of 400 cr vicinity in FY 22

Valuations

-

TTM it is at 6200 cr revenue, opm 8% at 475 cr, PAT 290 cr , Q3 is generally best in lot

-

TTM under long term average margins for similar revenues, opm at 11% at 700 cr, pat would be 500 cr+

-

At nominal 10% topline growth in FY 23 , revenue would be 7000 cr+, opm at 12% around 840 cr , pat around 600 cr+

-

For FY 23, add about 400 cr revenue from Elica, at similar margin it adds 40 cr in bottomline ( remember it’s a high growth segment and irrespective of covid has grown 20% in FY21 as well to 310 cr) - Here details

-

That is FY 23 , 7500 cr rev and 900 cr opm, 640 cr in bottomline - at long term median avg of 55 that gives us 34000 cr+ mkt cap, cash in books would be 2500 cr+ ( 500 cr per year type and after elica acquisition they Currently have 1500 cr). Current market cap is 23000 cr. That is 35-40% upside when margin performance revert to mean

Technicals

On long term support levels and bouncing back with good volumes on weekly

Now on Risks

- Don’t know for sure as to what caused recent steep fall from 2300 to 1800 - multiple factors seem to have converged

- Margins trajectory is weak, but so is case of rest of industry, should mean revert eventually given secular consumption growth in home appliances

- Apparently they lost some mkt share to LG/Samsung- as they took price hikes and competition didn’t, now competition increasing prices as well and counter measures from Whirlpool - article in thread above

- Apparently tax evasion at parent ( Whirlpool usa) level, though this doesn’t impact India unit,

- Competetitive intensity and ability to retain/grow mkt share in core segments of washing machine and refrigerator- innovation, quality and customer services driven - key monitorable

Small position