Seeking your feedback on what looks like a too good to be true opportunity in Wheels India.

Basics of the idea:

1). SEBI allows promoters to bring their shareholding within the regulatory limit of 75%, one was allotting rightsonlyto minority shareholders. Thus, in these issues, the promoters forego their rights entitlement and only the residual shareholders participate in such a way that post issue promoter shareholding is brought down to less than 75%. In the case of Wheels India, promoter (TVS group + Titan International) is at 91.44%. The promoters have thus chosen to use the rights to minority holders as the route to bring down their shareholding also presumably raising much needed funds for the company (to pay down existing debt) in the bargain.

Issue Price 400 (E)

Record Date for entitlement : February 14th 2014

Theoretical Ex-rights price is 749.

3). Returns and the risk

Assuming you are able to sell your 20 shares at the theoretical ex-rights price of Rs 749, you would book a loss upfront of Rs 1528 (825-749)*20 on your investment of Rs 16500.Subsequently, if you are able to sell these 51 shares at the same ex right price viz 749, you would make a profit of Rs 17799/- explained as [(749-400)*51]. Net of your loss of Rs 1528 booked earlier, you would still be left with a profit of Rs 16271/- leading to a theoretical return of roughly 98% on your investment of Rs 16500/-!!!

Risk is mainly from the not so good fundamentals of the company with mid-teens ROCEs, high debt on the books, lack of pricing power being primarily an OEM supplier and the general pangs of overall auto industry slowdown.

We have put out a detailed note on the post as well here:

On PE basis the stock is very expensive. A trailing pe of 32 .even if we take into account the slump in auto ind, it is still quoting at high valuation. In last 10 years the profits have hardly grown. The fundamentals as you mentioned are weak. If we forget about rights issue and if we have to value the stock basis diluted equity Will we be willing to pay 400 rs for the stock. What will be its fair price. May be the stock is quoting high due to punters in anticipation of rights issue or may be the price will crash after rights issue

We are slightly wary of valuing this company on a PE basis. This is largely because it is a manufacturing business undergoing a cyclical downturn. While depreciation is on the entire asset base, capacity utilisations currently are at ~ 70% and thus earnings are depressed. Due to this reason a lot of cyclical manufacturing businesses tend to look expensive when looked at it in PE terms during downturns. Also presence of debt (475 cr in the case of Wheels India) sometimes tends to distort the PE picture. We tend to prefer EV/EBIDTA which is at ~ 8.5x at CMP. Business of course is not great but looked at on EV basis it is not super expensive while surely not cheap. Have attempted to answer this question in greater detail on the post. Am repasting the link here since it did not go through properly the first time

Entirely agree with you that the key risk is price correction after issue ex date but sense that there is some safety margin in built due to the special situation.

Can we say wrt to this deal that Shareholders getting almost 10% stake in Wheels India for 40cr and hence company valued at 400cr mkt cap and hence at half of current PE?

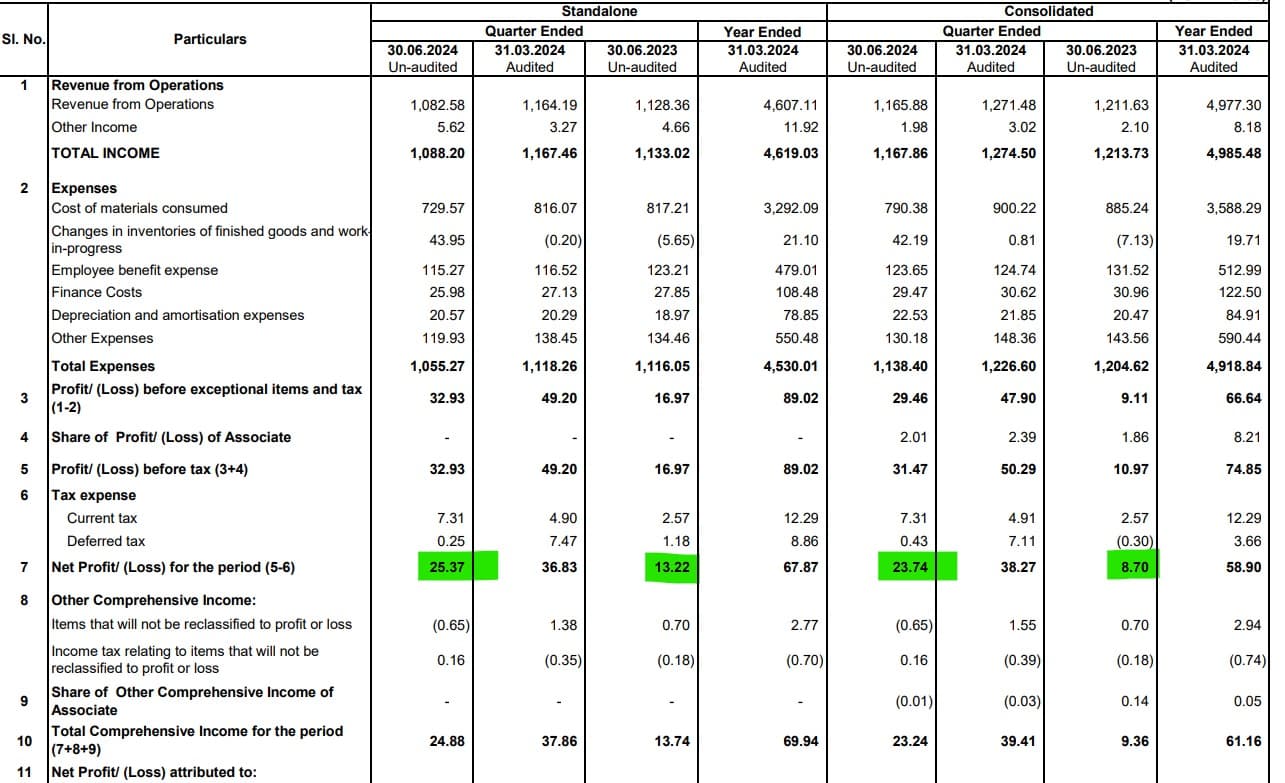

Wheels India reported good set of numbers. As management communicated in previous concalls margin improved to 8% in Q4FY24. 1% being contributed by discount by customers which normally gets accumulated in Q4.

Some points from concall

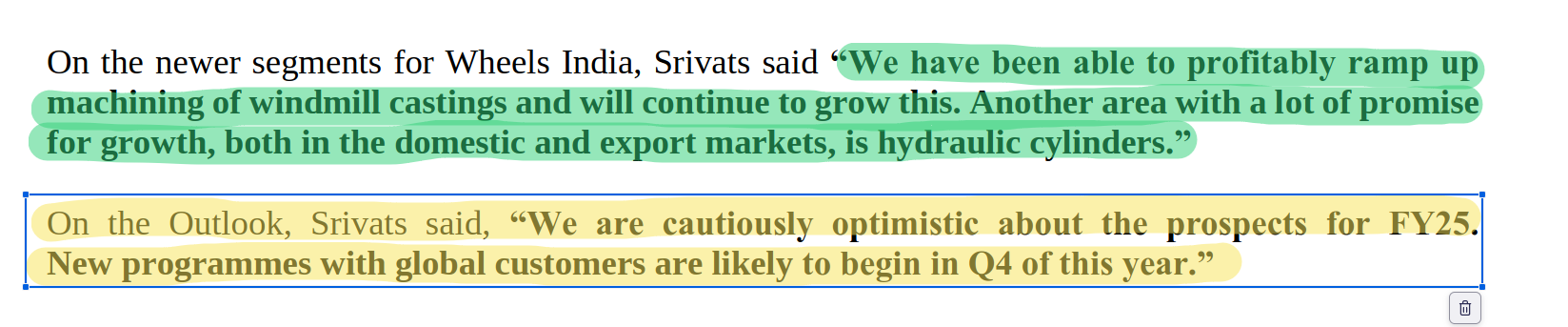

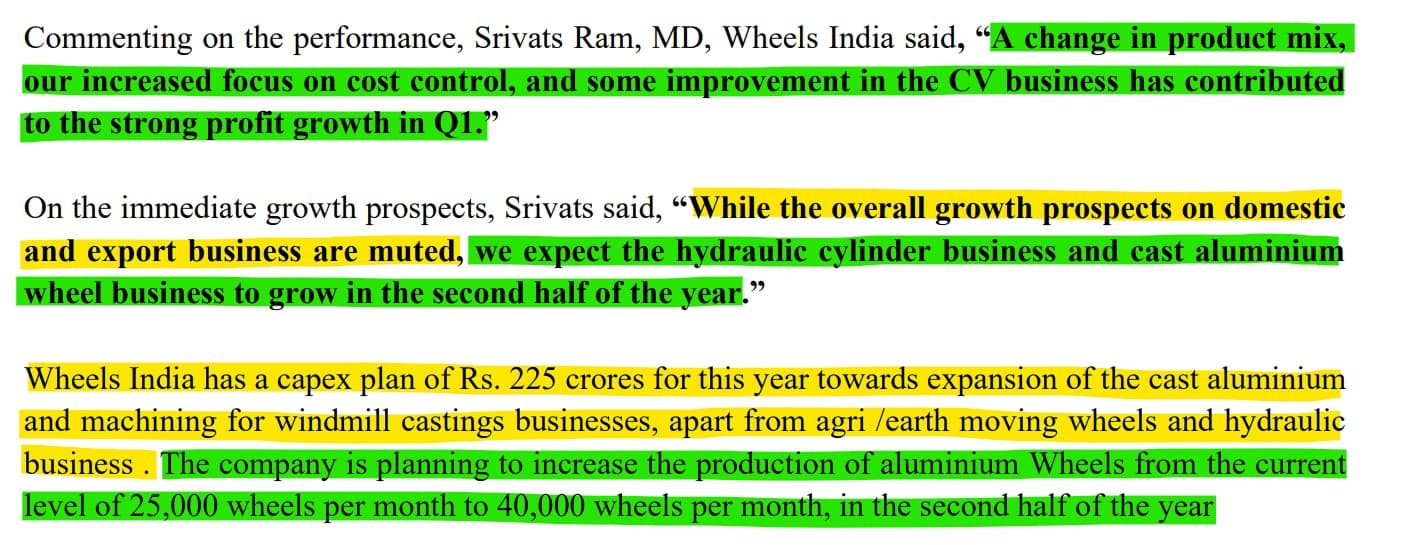

Expecting flat growth in FY25. Possible to grow if market situation improves

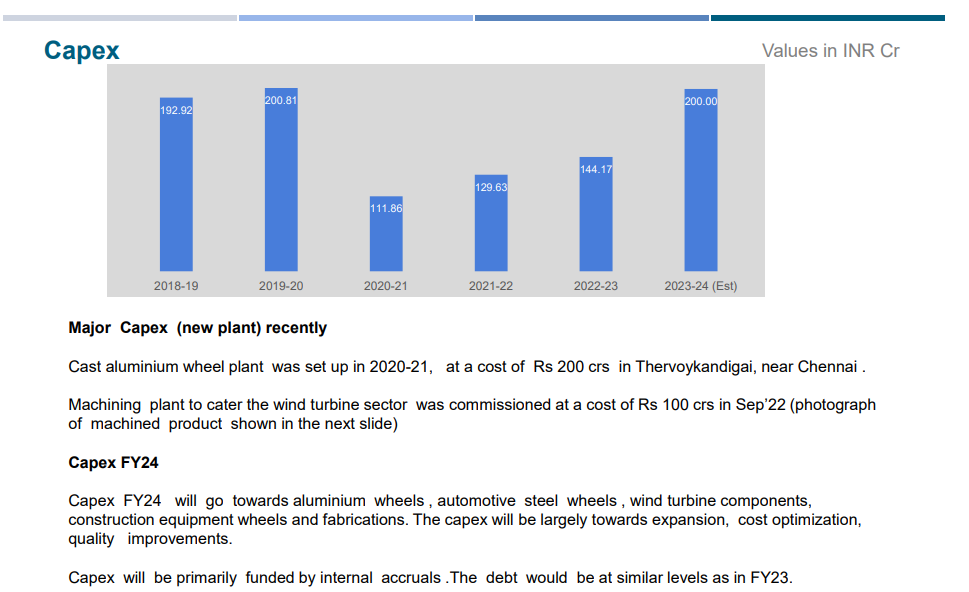

Planned capex of in excess of 200Cr across Wind components machining, cast aluminum wheels, earth moving & tractors, hydraulic cylinders and CV. All capex to be from internal accruals. If there is any moderation of capex, then 35-40Cr of debt to be retired.

Business opportunity in Railways - Looks not really focused here. They don’t directly wok with railways. They supply to customers like Alstom

Cast alloy wheels supply to domestic customer to start from Jun-24. Ramp up might happen in Q2 or Q3 of FY25. Since the ramp up has not happened, I believe this segment is not contributing to bottom line yet.

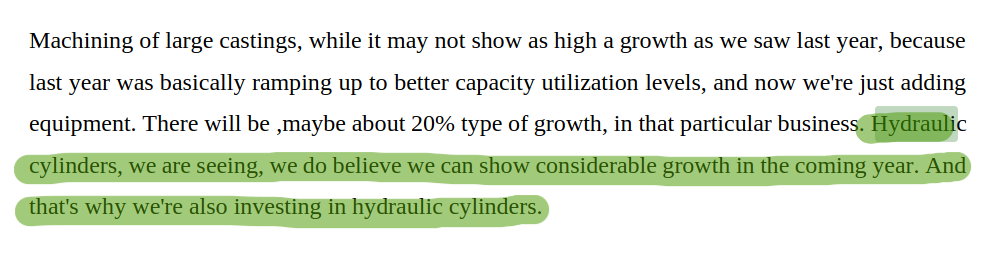

Machining / Fabrication of Wind castings - Supplies to both domestic and exports. Ramp will be inline with ramp of customers.

Monetizing of any assets / or rights issue to reduce the burden of interest - There is no non - core assets as of now to monetize. Will look for rights issue only for greenfield capex (as and when it happens).

Started supplying alloy wheels to one of the domestic OEM. This segment shall reach double digit margins once the ramp up happens to 40K wheels per month

Expecting exports to be muted as some of the new customers programs are going to be started towards end of FY25

Wind segment to grow as per the growth of customers

Raw material inflation/deflation is a pass through every quarterly

FY24 - profitability got impacted due to one time provision. One of European distributor got into trouble.

Although sales growth is muted, there shall be growth in bottom line

Capex will be 200Cr per year for the next 2 years

Expected IRR is 15% for new projects

wrt to margins - CV and tractor is single digit and rest all are double digit

40% of the overall business is having double digit margins

Sundaram Hydraulics is merged and good growth is expected in this segment. RIght now its high single digit and reach double digit with increase in sales

With the current capacity, sales can hit 6K crore (given all the segments doing well - as the industry is cyclical)

Directionally company moving towards 18% ROCE in next few years

Merger is Sundaram Hydraulics Lts is earnings accreative. In FY24, SHL clocked revenue of 158.9 Cr vs 127.1 cr (previous year) and PBT of 4.1 cr vs loss of -3.03 Cr. Management is confident of showing growth in hydraulics division

Not much participation from investor community. Only one asked few questions and the other one (myself) was listener

Decent set of numbers from Wheels India. As promised by management, profitability ratios have increased and good to see the same ratios in H2FY25 as well.

Also good growth is seen in hydraulics division. Management is confident of doubling the revenue in 2- 3 years from the current 150/160 Crs.

Loss making Wheels India Cars (Passenger car steel wheels) has turned profitable

Industrial segment turned profitable (loss reported in YoY quarter was due to one time pre inspection charges)

Reported a strong operating cash flows of Rs 215Cr vs 194 Cr half yearly.

Rs 133 Cr worth of inventory has been reduced

As per management Company has gained market share in export markets. But things are slow in US and EU. Need to wait for these markets to normalize for volume to pick up.

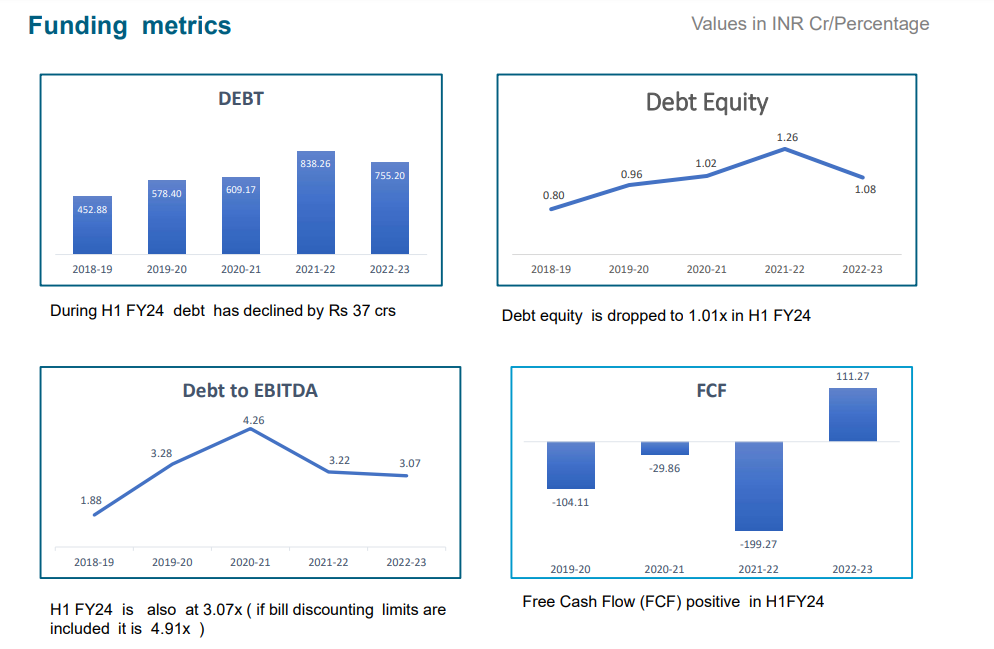

As per the management as the profitability of the company is increasing, expected to reduce the debt going farword (they didn’t mention how much, but considering the capex of 225Cr this FY25, my guess is that they could reduce in the range of 30-50Cr keeping the debt of the same level as that of FY24)

Even if we consider muted revenue growth - 5K cr (~ same as that of FY24), OP margins of 7.25%, company shall clock 362.5Cr of operating profits. If we take out 120Cr of depreciation and 80Cr of interest, PBT shall be around 150Cr where as the current EV is around 2500Cr)

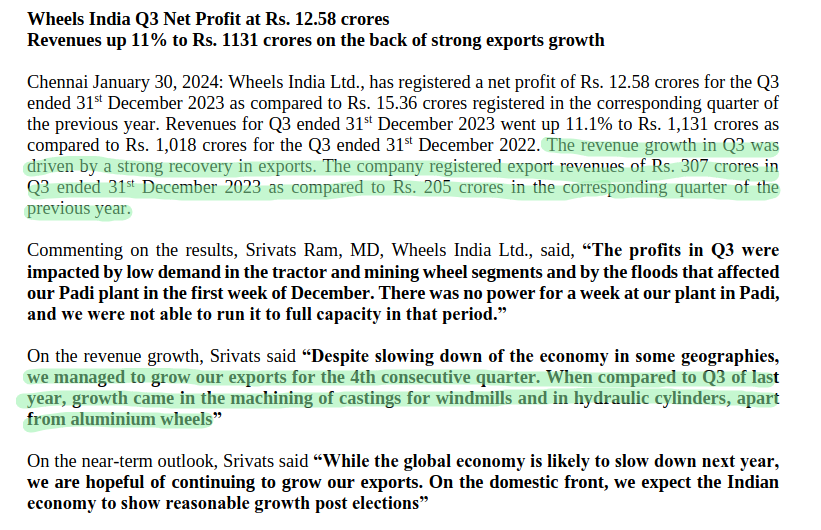

Press release:

Disc: Invested and topped up in the recent market fall.

Thanks for highlighting most of the positives. However the real problem is the revenue itself. The slowdown in CV and tractor segment has impacted the sales and management expects the same to remain in near future. They have also curtailed some earlier planned investments. So no real revenue growth to be seen in near future.

And another major contributor in profit growth is optimization of internal controls like cost and production not from improving product mix only which is kind of one time event and cannot be improved beyond certain point.

In my view above points have resulted market disliking the result.

The improving product mix is definitely contributing already. Windmill castings, alloy wheels, hydraulic cylinders and air suspensions all have better margin in double digits. While the revenue growth will look flat until the CV cycle and export turns, the margins are definitely improving and will probably peak at over 9 % once the CV cycle also improves. With debt getting reduced (and re-rated in due course) from the 300 Cr+ Operating cash flow, it will slowly shift into a Rs.6000 Cr business with a 9% EBITDA margin and a 200 to 250 Cr PAT in 2-3 years. Not a bad investment at a 1700 Cr market cap esp when other Auto ancilliary companies with barely any growth and definitely no margin growth are already quoting at 30 to 50 times earnings (range depending on how many times the words “EV” and “Lithium” appears in their concalls)

What about SSWL? Wheels India’s closest competitor. Margins are way better than Wheels India. Debt is lower. RoCE, RoE is also better. Aluminium knuckle casting revenues will kick in later during the year. AMW Autocomponent acquisition also over. Still way cheaper than Wheels India.