Here is the list of stocks which has given CAGR return of more than 40% according capital line

I am creating a topic to analyse what was the factor which worked for them? Was there anything common between them? what went right? was it management quality? Was that EPS growth? was the factor moat they were enjoying? Pricing power? unique products? marketing of the products? technolgy? combination of the above?

Answering this might help us finding the new opportunities.

if possible you can put 3 more columns -1)PE of 2009 ,2)PE OF 2019 3) Earnings growth between 2009-2019 -this will give an indication of PE expansion and actual growth in earnings which will help in understanding -is there a pattern

Common themes running through the above stocks are–1.Consumption.

2. Steady demand.

3. Management quality.

4.No compromises on quality.

5. Year on year steady numbers.

These are not stocks for the short term punter, they are investment worthy stocks.They are not operator driven stocks. And they are anchored by a steady management hand on the rudder,untainted by managements out to make a fast buck at the cost of the shareholders. And not surprisingly, Bajaj Finance leads the performance pack,as it has the consumer reach and consumer confidence to be a “lambhi daur ka ghora”.

No magic winning formula,but an amalgam of consistency and hard-won consumer confidence.

Some of the companies have real earnings growth while others had momentum surge pushing the stock up higher. Hence the same portfolio will definitely not produce similar outcomes.

All this really tells me is how powerful hindsight bias can be. Most of these companies weren’t so obvious “quality multibaggers” back in 2009. To quote a few:

Bajaj Finance didn’t adopt their latest business model back in 2009. They changed it only about 3-4 years back. There’s no way in god’s green earth someone could have guessed that they would adopt this model 6 years down the line and that the model would become successful.

Eicher Motors was a mediocre company at best during 2009. IIRC, their RoCE was in the range of ~15% or so. In fact, at that point in time, they were known equally well for their Eicher-Volvo line of CVs. The most famous Royal Enfield model, the Classic 350, came out only in 2010, after which Eicher stock blew up. Several famous investors/fund houses, like Prof. Bakshi and Motilal Oswal, first bought Eicher stock based on their CV business, not the motorcycle business. In fact, Prof. Bakshi sold Eicher stock somewhere around this time and bought it back after Classic 350 became a hit.

TVS Motors had an even worse business in 2008-09 times. They were posting losses and had been going through several years of bad business up until then, losing market share rapidly. Then around 2011-12, they developed better engines, set up financing partnerships for their vehicles, launched better models etc to regain their lost market share. And they eventually did very well.

I suppose you can find a handful of more examples if you know some of these other companies better. This is the biggest risk of talking numbers alone without stories backing them up. There is no context.

In my opinion, we should stop fantasizing about 30-40% CAGRs and aim to earn SENSEX/NIFTY + 3-4% CAGR. Over a long period of investing, this would result in commensurate wealth creation.

I dont think we should discourage people from dreaming big or aiming high ! There are patterns if one were to looks closely at few stocks and these in no reason why similar pattern may not be exhibited by some other stocks in the future. There is always a thing or two one can learn from learning the history.

A man can dream. But I’m talking about expectations. If you expect a minimum of 30% CAGR, you tend to make riskier bets. That’s how the market works.

And you may end up earning that returns, too. But for every Eicher Motors, there’s a Vodafone. You just have to acknowledge the fact that you’re just as likely to make mediocre returns if you aim that high.

I interpreted the topic differently . I dont think the thought process of the post was to make a 30-40% CAGR and i dont think anybody can consistently do it. I think the objective of the post as i read is to identify the patterns or commonalities that led to these companies post such staggering CAGR. Out of 15 stocks you own may be only one or 2 does it but its worth looking for. The problem is not with trying to find high CAGR stocks but people expecting it to be 10 baggers in a year and as you can see most of these companies took a long time to grow their business. So it essential the mindset of time frame rather than your CAGR expectations that you end up owning duds.

Nice thread Pratik, i have also wondered if there is a common thread about these multi baggers…

sometimes one gets lucky as Dinesh pointed out, we could not have known that Eicher would strike success in Classic 350 and not the earilier VC business. Also TVS would come back from the brink, so lets accept that sometimes its plan luck.

But for the rest, we must have a checklist, and one major thing i would like to see is presence in a growing industry with high market share and a deeper understanding for why they have that market share. . i.e. whats their moat which will ensure they will be able to maintain that market share going fwd too.

There have been studies done by Ambit on the same, which will be helpful…

looking forward for learnings through this thread…

I had read an old interview of Rakesh ji, around 2001/2 time frame, he had given 3 names, Titan was one of them but rest 2 did not go anywhere. I learned couple of things,

No one knows which stocks will turn out to be a multibegger

You need only few good ideas ( and luck + Patience) to make very decent returns

On average all the ideas will not work but the ones which work, they can outweigh the

negative/laggard stocks over time.

A better study would be about the companies which consistently doubled or more, their market cap, every 4-5 years, since last 15 years. Amongst the MNCs names like HUL, Nestle, P&G stand out. Among Indian companies, names like Titan, Pidilite, crop up.

The moot question is - can they keep repeating this? I think it is worthwhile to plonk some money in to these companies, to test this.

Good learning in those pithy points. But one small learning that I can add here is that no company enters this world all cylinders firing,and that too no company finds it’s bearings so quickly. It is a continuous process of finding the right business model,the right product,the right CEO,the right process,and the right growth trajectory. Just too many variables to put down in a pat formula.That said, Life,and the stock market, is all about hitting the right buttons,and sometimes even the best can only look back with a prayer. Witness Rakesh Jhunjunwala, who hit upon Titan after some flops.

Some fast growers sputter out fast, others manage to hit the sweet spot through trial and error. This forum is all about finding the right combination,the right pattern from those who wish to share their learnings from their investment journey.Each one who participates in this forum,has something to impart,and it is up to each one of us to spot that learning,that pattern.What works for one,may not work for me.And quantum physics has some light to shed here–the mere fact of observation and analysis may alter the equation.

Just as some generals always fight the last battle by looking into the rear view mirror,forgetting that they must look through the windshield instead,to prepare for future battles,so my limited learning is that the formula that worked in the past,may not work in the future,because the entire eco-system is dynamic, keeps on changing. As time old wisdom puts it,You cannot bathe in the same river twice.

So perhaps,we should study the past,without back testing so much as to become it’s prisoner.We are all wiser in hindsight. The quest for that X-factor will always go on.

@pratikchandak

At a high level, I like to think increase in stock price as a function of primarily 3 items

a. Growth : Put simply, sales figures and YoY growth in them

b. Efficiency : Using lesser resources per unit of sales/production, put simply Operating margin

c. Multiple Expansion : Entirely market driven, multiple market is willing to pay; primarily PE ratio

Obviously there are multiple nuanced items which affect prices, but everything can be categorised as an either/or in the above three buckets. Different industries primarily move on different parameters, Cyclicals move due to efficiency; FMCG/Durables moves due to growth and multiple expansion. Capital intensive industries move due to efficiency. Then the are industries which start off as capital intensive industries and develop a strong enough brand pull to show characteristics of durables and so on and so forth. Different metrics such as ROE, ROCE, ROIC, PEG are outcomes of above three business/market factors.

To answer your question, what went right for these stocks, I am attaching a sheet for which shows primarily which lever pulled the top 10 stocks into stratosphere

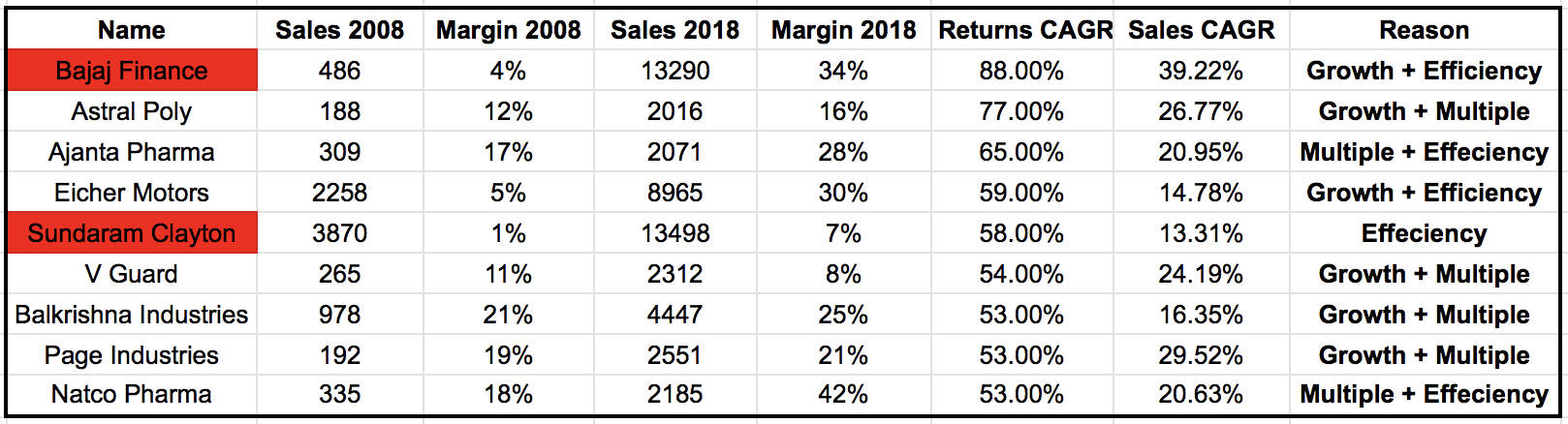

The red ones were in losses during that period. Growth would be common theme across all so included in only companies where it made sizeable difference.

Among the three factors Growth and Multiple expansion are relatively less difficult to understand and make a reasonable future assumption. Understanding efficiency is whole another beast and would require deep understanding of factors of production and raw materials market cycles.

To reiterate the point raised by @dineshssairam on hindsight bias, there were far more companies that were better on multiple business fronts than the above stated companies. To have picked up these companies and have significant amount of capital invested into them would have required an immense amount of foresight and more than one’s fair share of luck.

Good management, low capital requirements, favourable and growing business environment, Opportunity of growth remain as valid pillars of returns as they were in 2008-09.

Well said…I remember I bought TVS motor at 60…then it went down n down n down…till 35 and all were saying to sell…no doubt we listen to such dubious people. Great learning for me

You weren’t alone, probably. TVS fell from a high of Rs. 80 in April 2006 to a low of Rs. 9 on Feb 2009. Of course, the 2009 crisis was also a culprit. But that’s a 88.75% fall. That too a slow and painful erosion over 3 years.

During 2009, you essentially had a struggling business, which had posted back-to-back Net Losses for 2 years, paid dividends on top of the loss, almost doubled their Debt levels and were struggling to push sales (Increasing WC). It wouldn’t be until 2013 that they’d design a newer, more efficient engine, proactively sign contracts with Banks for vehicle financing and launched several successful models, which slowly pulled them from the brink of being a terrible business.

Sitting in 2009, TVS Motors would have the last choice of investment for most of us. It would have either required being foolish or having incredible, company-specific insights (Bordering in inside info) to have had the courage to invest in the company.

I have heard this statement from so many experienced folks in recent times. Setting / resetting the expectation goes a long way in creating sustainable wealth

No no…it’s not mind set.

If your wealth gets eroded by 80% , what you think next?

Save left 20% ?

Or give away that too?

It’s the second choice sometimes which has to be made and most difficult one. One you have seen a stock erosion of 80% you won’t expect it to be a multibagger … right?

Getting Multibaggers is also a function of probabilities. Peter Lynch had as many as, I suppose, 127 scrips. Many of them did tank. But, some were Multibaggers. Overall the result was positive. Point being, if one is aiming for Multibaggers then he should get his probabilities right as well.