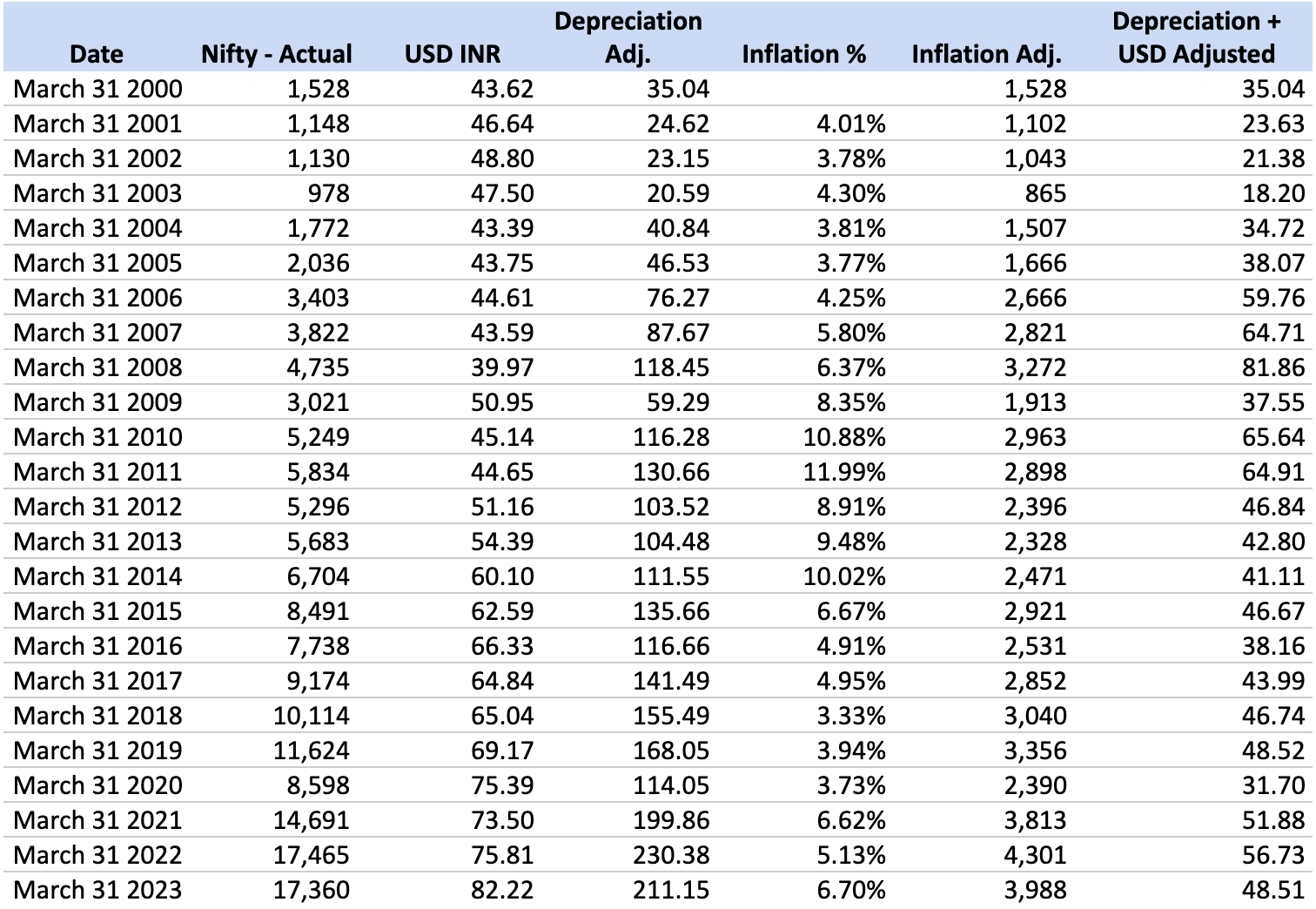

I was doing some calculations on the Index since the start of the century and I was surprised by the results.

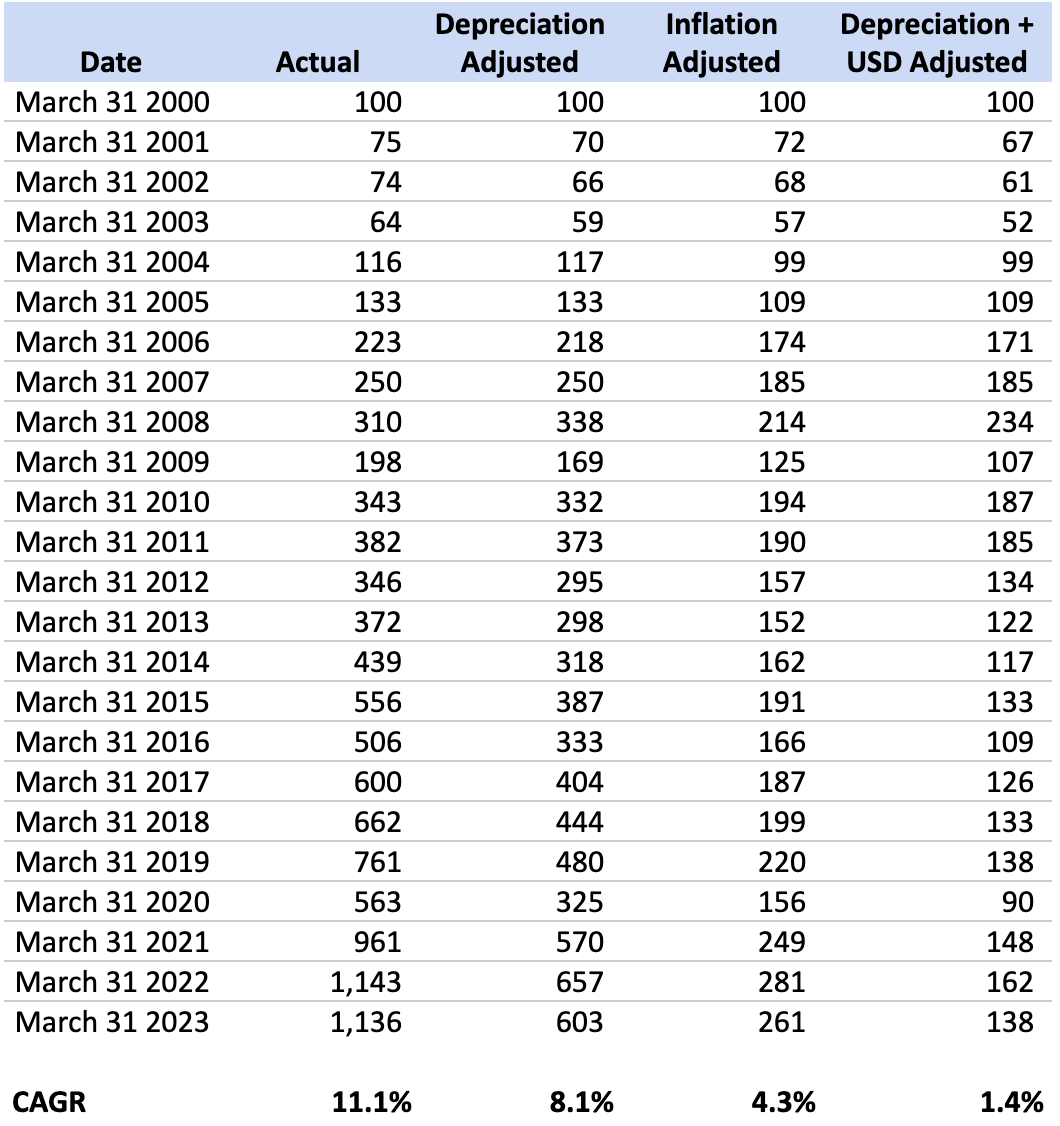

From March 31 2000 to March 2023, the Nifty rose from 1528 to 17360, at CAGR of 11.1%. Prima-facie, this is a return that most investors would be content with over a long period and would appear to be a moderate compounder of wealth.

However, it is important to factor in the real rate of return. While from a macro-economic perspective, the real return only factors in inflation, I wanted to capture the effect of currency depreciation as well.

Is India really growing? 1.4% returns compounded over a 23 year period is abysmal. How do we define growth? Excluding inflation, where is growth taking place? At a macro level, has the standard of living improved? Has productivity improved? Has value creation increased?

Compounding, while magically accelerating returns over time, also accelerates expenses over time. We should be aware of the real return. Do passive investors (most people) invest for capital preservation or capital creation? Why is there a push indexing investments?

While I am personally diversified across asset classes, no other class matches the returns of equity. With this, given the fact that equity is the only instrument that can preserve purchasing power, does it make any sense to diversify, in a meaningful way, across asset classes in India. Fixed income returns with this approach will likely be consistently negative while gold / bitcoin can be used as a hedge calamity.

If you are considering USD depreciation, then the inflation has to be also in USD terms. Uniformity of currency to be maintained while evaluating inflation.

In the long term, near 4% real return is what is expected in stock, i.e., passive funds (including US market). Check out the book “Stock for the long run” by Jeremy Siegel. India’s performance is almost same to that of US in index investing, if adjusted against inflation/currency depreciation.

You have to consider dividend. It is a major part of total return over long term. Taxes have to be also considered.

Other than equity, all other asset classes return real negative after taxes. Hence, I don’t invest anything other than equity and for short term needs (less than 5 years) I hold in cash / liquid funds.

Very nice to hear that you invest fully into equity , just like me. Recently i was doubting this approach, as everybody is talking of proper asset allocation and gold, debt etc. I thought, am I being more aggressive and will it boomrang on me, if market goes down. Whether i should invest into other asset classes too, as all experts, fund managers also prescribe this. If possible.kindly shed some.more light on this to reinforce my thesis.

You will easily get return data on Nifty. If you ignore minor tracking error, Just check Nifty Index fund returns which will give return data in lumpsum and sip mode for nifty. there are index funds from UTI, ICICI, HDFC etc there from last 20+ years.

Minor expenses will be there anyway if one buys ETF or Index funds.

If majority of Active funds unable to beat the Nifty/Index returns for several years, one will move to Index funds to save expenses. For the expense active funds charge, they should able to generate 4-5% excess return. Do not compare just 1/2 years, looks at 5/10/15 years long term if active funds able to beat Nifty returns.

why you need diversification? you invested 100% in equity and during market crash you need sudden money. will you sell your equity taking loss?

To safe guard such situations, some portion has to be in liquid/debt/FD instruments where capital is preserved.

one needs money in next 1-3 years, they should not invest in equity. need to choose FD/liquid/debt as no one know how stock market will be when you need money.

Asset allocation between equity and debt / gold is touted because it slightly minimizes the portfolio drawdown. And if there is less drawdown, it is psychologically easier to follow through the plan. But, logically for psychological comfort one takes in less return.

One way to visualize and stick to equity is this:

Dividend payout (in Rs) of Nifty has never had a drawdown of more than 10%. I evaluated for past 15 years. It is probably the same when extended over longer period.

Decently diversified equity portfolio increases its dividend at an approximate rate of 10 to 15%. Nifty has about 10%. Whereas, debt / government securities have zero growth rate of interest income.

If you have Nifty 50 as your portfolio or a coffee-can portfolio and live on dividend income. Then it is an extremely stable source of income, even during market crashes and panics (including Global financial crisis, Covid crisis etc.). The only caveat is that you don’t re-shuffle your portfolio a lot.

What is the logic behind looking at currency depreciation? I understand it could be relevant for folks living in the US and investing in India but otherwise can you explain how it would impact the general investing public? The inflation adjusted return makes sense but then i think that taxes and dividends should also be accounted for.

Is there any website or tool for finding XIRR or CAGR from zerodha or upstox trading statement or ledger. It is very painstaking process to count it manually. I am asking here as we need to also find what is rate of return when we are doing DIY method and compare it with index return. Thanks!

Artos app on Android does provide XIRR values. It also imports your statement from zerodha and upstox to build your portfolio. Not available on iOS yet, but looks like a good app to try

USD value is inflated to some extent due to might of US and being sole superpower for last 30 years.

Also, US has been exceptional economy for same reasons. So comparing with an exceptional currency may not make sense.

Basket of currency may be a better approach. Or may be Gold.

US inflation has to be chosen as you are trying to get USD returns.

Growth is better experienced (both -ve and +ve) around us rather than look for in stock statistics.

High stock returns may be complex issue to judge growth. A lot of countries in Europe and even Japan have not shown lot of growth at index level but countries have progressed and standards of living improved.

Diversification has its benefits and limitations. Allocation that is made to uncorrelated assets is safeguarded when market falls, but if the allocation is substantial, and if market is going up for extended period, we may feel we should not have allocated so much.

I vote for debt though, as this serves both as a cash flow in bad times, so that equity if fallen is untouched, and for investing more at such times. And as the equity allocation increases with time, despite the increase in knowledge and experience, it is hard to look at a big loss, even when it is notional.

It depends on the financial, psychological states and the age we are in life.

I am more invested in debt than in equity, with small allocation to gold and silver both w.r.t diversification and trading opportunities, and my learning is focused on equity, as I see it as an opportunity to get more than debt.

If asset allocation to other than equity is just meant for the purpose of emergency expenses so that equity is not sold off during wrong times, then better to have a contingency fund for 1 year expenses as well as income from active profession. Remaining all net worth can be invested into equity as its a superior asset class compared to any other asset class. The comfort and stability can be sought by active income as well as emergency provision.

My point is that, diversification among asset classes is both a broad strategy and can be customized as per the requirements. And equity as a component in itself can be diversified too as per one’s own requirements through stocks, ETFs, or even active funds.

This is all personal finance, as much as it is about financial products, it is personal too. And I for one, like the availability of so many choices to construct a PF as per time, capital and return expectation.

What if we are into one of those no-returns time zones. Do you expect great +ve returns when commodity cable, chemicals etc are trading at north of 50PE

We have a history of +ve returns and media fund managers, PMS guys and most of finance world has vested interest in showing us a rosy picture. But how do we know the future. Most of us look at US markets to clue. It is a nation which is an exception on this planet.

When i closely observe the periods of “zero returns”, they are not flat…there are ups and downs during that time. Only the definition of zero return is starting point of the zero return period and ending point are same. This is applicable to people who put all their capital at one point of time( may be start of zero return period) and withdraw at one point of time ( end point of zero return period). But for a person like me, who will be investing regularly during this zero return period and also withdrawing regulary for expenses, I will have multiple points of entry and exits during zero return periods and hence there wont be relative zero return for me.

Use Dollar based indexes . They tell you how much dollar based growth. Now you know why FII’s are selling Indian equities . They get 5 to 6 % un US bonds why burn midnight oil in India ??

I had similar thoughts like you at one point and the general advice of 50% equity and 50% debt for young earners didn’t appeal to me much. I think when the portfolio is small, and when you are starting out, 50-50 makes a lot of sense. Gives one a lot of peace of mind.

However, if you look at a 1CR+, do you need 50% of the same in debt? Especially if you are living way below your means and retirement (or lack of employment) is 10+ years away? I don’t feel that way. I think one could go for 70% or 80% into equity. The assumption is that you know what you are doing and is willing to sit through (and buy more) during drawdowns.

Emergency fund, short term and medium term goals are outside of the above math.