Just wondering why there is no discussion about this company. Is it because of frequent negative news about promoters manipulating stock price? Refer moneylife

In addition to negative mentioned above company is currently loss making. 95% shares of company are with 10 entities. However, i am not sure to count is as positive or negative.

Brief about company:

WDL focuses on putting up and operating Quick Service Restaurants (QSR) in India through its subsidiary Hardcastle Restaurants Pvt. Ltd. (HRPL). The Company operates a chain of McDonald’s restaurants in west and south India, having a master franchisee relationship with McDonald’s Corporation USA, through the latter’s Indian subsidiary.

Opportunity: Opportunity is purely on long term basis i.e. more than five years. And rational is based of much quoted consumption growth story.

While doing my own research i found the following various news items useful and as a lead for further research: Article 1 Article 2 Article 3

Very interesting story and attachments. The family jewel is the Master Franchise Agreement with MacDonalds, which is tucked in as a wholly owned subsidiary (HRPL) of WESTLIFE. This protects the family jewel in private hands without direct legal access to the public.

Listing is only on BSE and not on NSE. Trading continues to be very thin and still dominated by bulk deals within promotor family members. Besides, all returns ratios (ROCE, RONW, OM & NP) are erratic over the past years.

In effect, this is a protected jewel with price discovery & real unlocking of value yet to happen in the marketplace. Its anyone’s guess how long this would take as the Principal does not like listings overseas to be publicised (most franchises are built on franchise fee and royalty model). Shrewd business family.

Research if minority investor interests have been protected in the past, if you really want to invest.

31 March 2017 shareholding pattern submitted to BSE indicates 12 Foreign Portfolio Investors with interest in this counter with holding of 5.43% as at quarter end vs 10 investors @ 4.67% in previous quarter end.

Is the stock gaining international investor interest ?

These are great results.

Everything is going good for them.

SSSG 9.2 % in this economy

RoM (Restaurant Operating margin ) up to 17.5% from 15 % YoY

11 new restaurant opened in the quarter.

(I refer to results which exclude ind as 116 as it is more comparable)

Disc- Added Today

Hi,

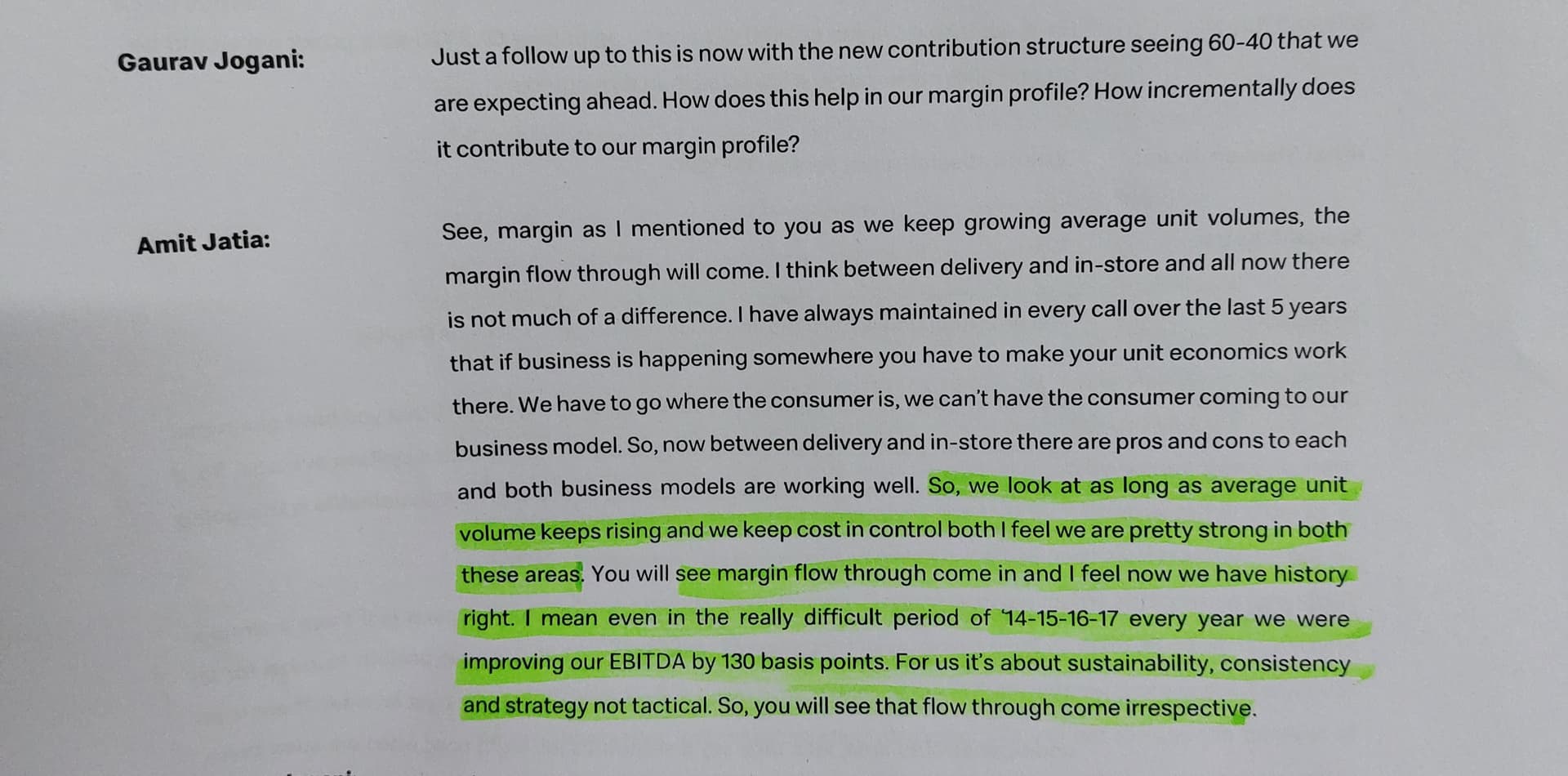

History helped us to be a better investor in the time period of FY14,15,16,17 It was a tough period for the whole qsr but Westlife managed to improve their margin by 1.3% every year consistently. concall attached please look.

Key Highlights : Encouraging 3% SSSG in 1H FY24 on a strong

base of last year

• Same Store Sales Growth (SSSG) in Q2 stood at 1% YoY despite the continuing weakness in consumer eating out trends and high base

• Share of consumer visits to McDonald’s and brand equity scores strengthens across West and South markets.

• On-Premise as well as Off-Premise business grew by 7% YoY. Off-Premise contribution remained stable at ~41% vs last year.

• Focus on Digital through Self ordering kiosks and Mobile Apps continues with Digital Sales contributing 67% to topline, up nearly 30 YoY.

EBITDA grows 7% YoY in 1H FY24. Margin was weighed by relatively lower operating leverage Gross margins improved 93 bps YoY in Q2 led by better mix and cost saving initiatives. Input costs remained broadly stable. Restaurant operating margins were lower by 58bps YoY as higher gross margin was offset by royalty and annual store payroll hikes. Operating EBITDA margin was lower on account of higher G&A costs. However, on sequential basis G&A remained largely stable and is likely to track

the current run rate.

The total revenue for Q2 FY25 shows a marginal year-over-year increase, indicating slow but steady growth.

The gross profit remains relatively stable compared to the same quarter last year.

The Restaurant Operating Margin (ROM) stands at ₹114.97 crores, showing profitability at the operational level.

Weaknesses:

Continued Negative SSSG: Despite improvement, Q2 FY25 SSSG remained negative at -6.5%, indicating ongoing challenges in fully recovering to pre-pandemic same-store sales.

Impact of External Issues: External community-related issues continued to impact some stores, affecting on-premise sales in specific locations. While WFL is actively addressing these issues, their extended duration presents a potential risk.

Exposure to Macroeconomic Factors: WFL acknowledges the impact of macroeconomic factors, particularly higher inflation and subdued consumer spending, on its business.

Quality of Earnings:

WFL’s gross margin and cost optimization efforts suggest no relative improvement in earnings quality.

The continuing negative SSSG and the effect of external issues on on-premise sales raise questions about the sustainability of earnings growth.

Overall, WFL’s Q2 FY25 results reflect a mixed performance.

Disclaimer: Invested and Biased. Less than 4% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any transactions