Is west coast the cheapest paper stock currently in the market? please correct me if I am wrong it has Mcap to sales 0.5 assuming 3200cr for this year. It is completely integrated from pulp to paper and also it acquired Andhra paper not a single year financials after acquisition and business normalization and debt is also very modest 500cr of which sales tax loan of 100cr which is interest free.

Please throw some views or add anything you are aware of, looks like a good reflation bet.

1 Like

West coast has better grip over western markets in copier segment and quality is also top class in segment.

I have spoken to number of large copy ( xerox ) centres and everyone has vouched for B2B copier paper as it does not get stuck during fast copying process.

But valuationwise JK paper is better placed as it is likely to clock almost 800 to 1000 crs bottom line next year.

Have a look at JK Paper thread if you are interested in paper sector.

1 Like

For cyclicals in general - Since these are asset heavy business, i use P/Bv. I check what multiples the company and its peers were trading at the bottom and top of the previous cycles. Gives me an idea of how much the market is generally willing to pay for such cyclical bets and i see if there has been any change in industry structure since the last time (Eg: Even in bad times its unlikely that sugar firms will trade at the valuations that they used to as sugar is no longer just about sugar) Valuations matter a lot here because stock will start tanking before the cycle turns. Personally I think its still early days for paper.Its best to have a basket approach when investing in cyclicals. Hope this helps

Disc: Invested

2 Likes

Some significant structural changes have happened with paper industry over last few years

1)Evolution of e commerce

2) Online Food take away business

3)Overall increase in packaged food consumption.

4) Implementation of GST has made interstate business and transportation easy leading to higher requirements of packeging.

5)Rise in palletised container exports .Palletised containers consume higher paper boxes.

6) Many people have bought printers in lockdown due to online education. This will fuel higher paper consumption in future.

7) Govt proposed ban on single use plastic.

8) Supportive global pulp prices.

Over next few years many paper companies will churn out good profits.

One with full pulp integration,better product mix, economical production capability and good management will not only grow as per sector but will snatch market share from smaller players and to some extent from same sized competitors.

These companies will become debt free and will not be valued at P/B ratio but with PE ratio.

Trick is identifying such companies from the sector who have already built capacity as the cycle just starts picking up.

4 Likes

Strong results from Andhra Paper -

A possible negative is they are exploring expansion -

-

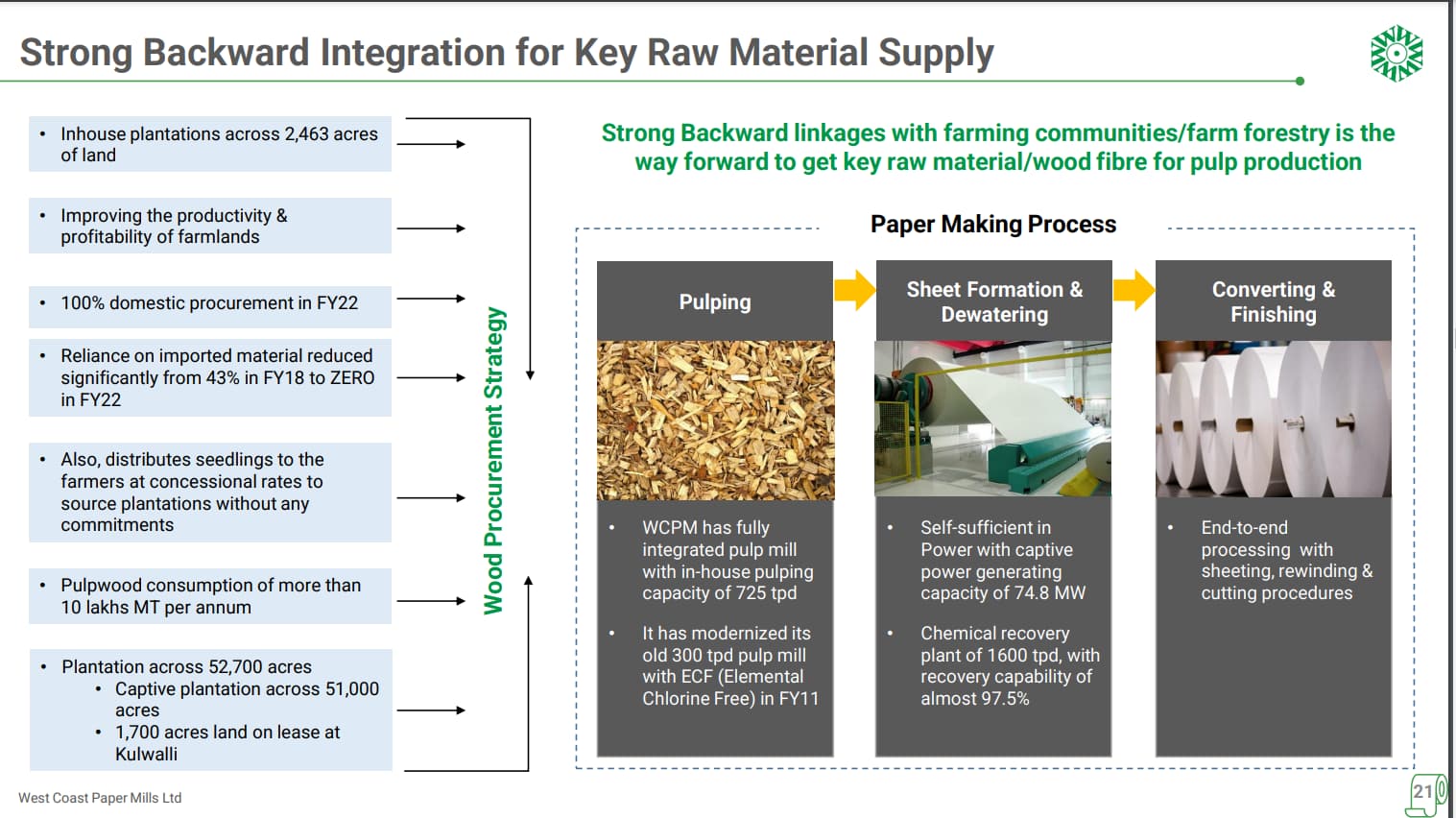

Since 2022, import of RM has reduced to 0. ( Mar23 concall)

-

Borrowings are reducing each year.

-

Long term rating upgraded from AA- to AA ( ICRA credit report Nov 22).

Studying, No Investment yet.

3 Likes

Andhra Paper results -

Results look decent considering that there has been talk of a industry slowdown…

2 Likes

Any one tracking this company can highlight the reason for such low valuations

Thanks…yes saw their numbers which was on weaker line now the valutions are inline with other paper stocks.

~ not to forget the fact that paper usage per capita is very low in India compared to western counterparts.

~ only time will tell whether digitalisation is a threat to this sector

~ given the size and domestic consumption of our country I can’t just avoid this sector in my watchlist

5 Likes

Insider buying seen at West Coast Paper. Might be window dressing but at current valuations the stock is just too cheap even within the paper industry. Certainly should grow from here for a 1-2 year viewpoint.

2 Likes

With 2000 Cr investments on balance sheet, at current market price it is available at 1 time FCF, for a long term 6-7% sales growth. Recent acquisition of uniply, gives an optionality to deploy cashflows to scale that business. It can be a very good value buy for someone with long-term horizon.

Disc.: Invested

2 Likes

Can someone help the group out in tracking:

- Industrial wood

- Domestic price and international pric s of the paper

- Pulp price (Since low pulp price leads to a lot of imports)

1 Like

You can use screener for all 3. Example - Login - Screener

1 Like

Antidumping investigation into imports of Virgin Multi-layer paperboard is in progress. JK Paper, TNNPL, ITC, etc are parties to it. Does the outcome of that impact West coast also? Also, What’s the likelihood of it ending with positive outcome?

Also, government is relooking the FTA with ASEAN countries from where most of the imports are getting dumped. A bit of chance there too.

1 Like