Report :  INVESTEC - PAPER INDUSTRY REPORT has the content related to Westcoast paper mills

INVESTEC - PAPER INDUSTRY REPORT has the content related to Westcoast paper mills

West Coast Paper Mills (WCPM) is one of the top branded paper company in the country, which is benefitting from a consolidating industry in India, and overseas. WCPM has successfully delevered its balance sheet over the past few years, and we expect it to be practically debt free by FY20. The management team is one of the more experienced team in the industry, and has built a solid distribution network making it capable of quickly expanding capacity, and sales. Valuation of 7.6% FY18 FCF yield, 10x FY18E P/E (8x FY20E EPS) is supportive, even as we expect strong cash flow to sustain. However, a track record of unrelated diversification makes us somewhat cautious, and we initiate on the stock with HOLD rating.

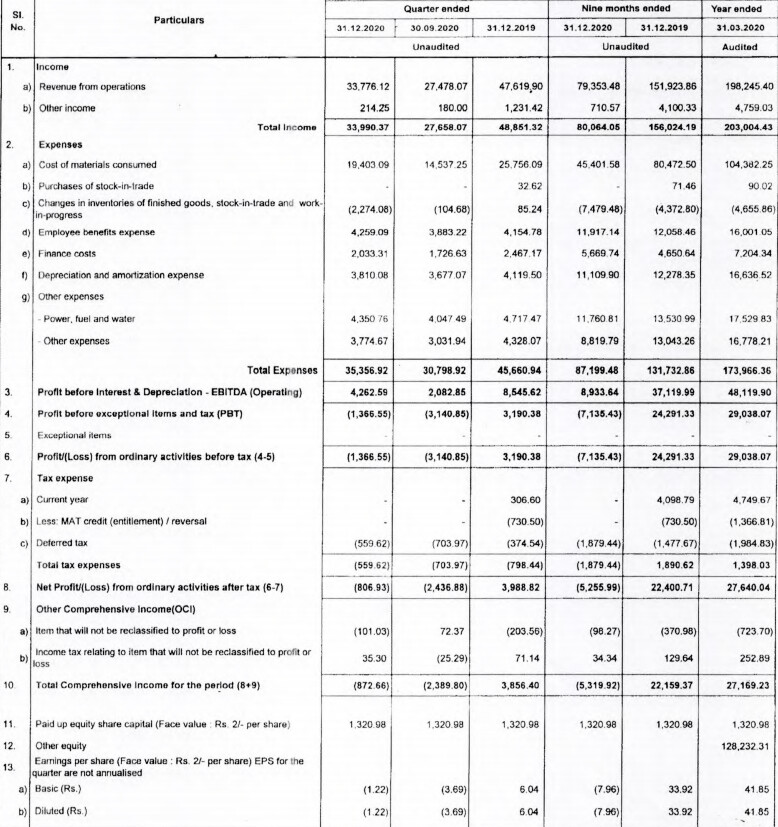

WCPM is one of the top paper companies in the country by size – it operates a 320,000 integrated paper mill, with sufficient pulping capacity, and a 75 MW power plant. An optimal size of the plant, it is amongst the more profitable paper companies in India today – FY18 EBITDA margin of 21.2%, and RoIC of 14.7%. WCPM also enjoys adequate supply of water, a key ingredient in paper making, ensuring a disruption free production schedule.

WCPM is one of the top paper companies in the country by size – it operates a 320,000 integrated paper mill, with sufficient pulping capacity, and a 75 MW power plant. An optimal size of the plant, it is amongst the more profitable paper companies in India today – FY18 EBITDA margin of 21.2%, and RoIC of 14.7%. WCPM also enjoys adequate supply of water, a key ingredient in paper making, ensuring a disruption free production schedule.

We expect the paper cycle to remain buoyant, which should support profitability of top paper companies like WCPM. Over the past 2 years, WCPM has generated

over Rs.5,825.6 mn of free cash flow as it has taken advantage of the 2nd widest distribution network in the country as the paper cycle recovered.

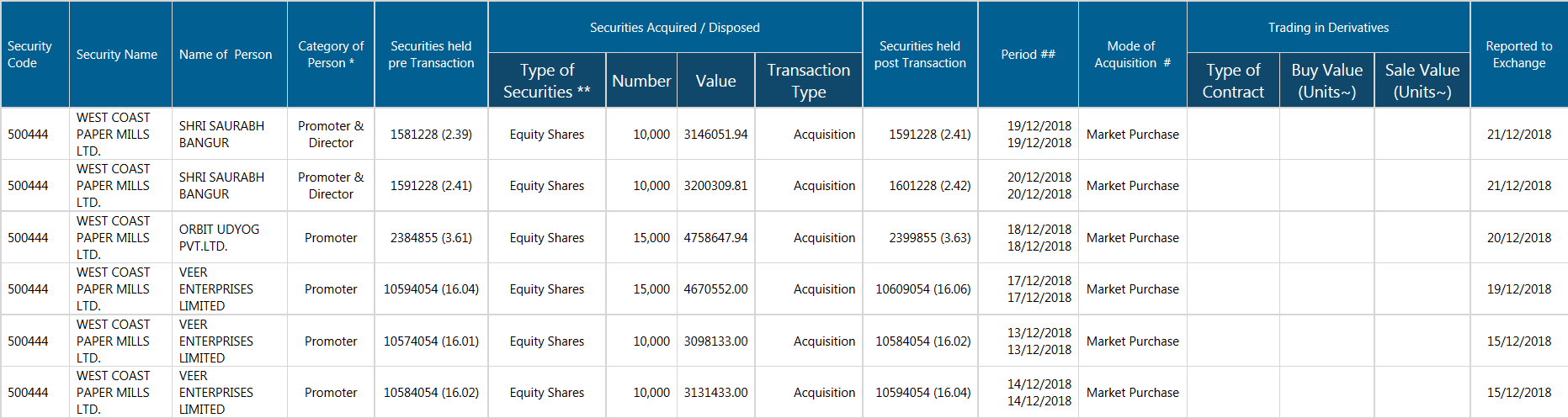

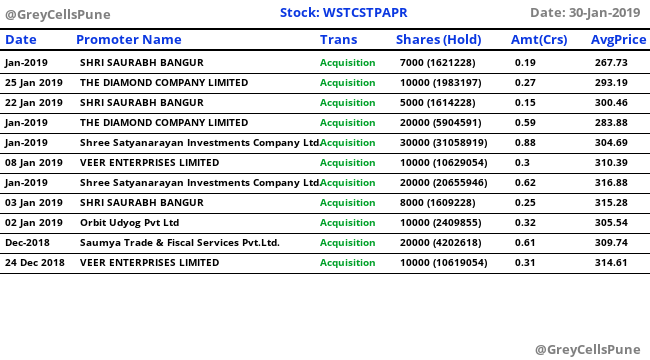

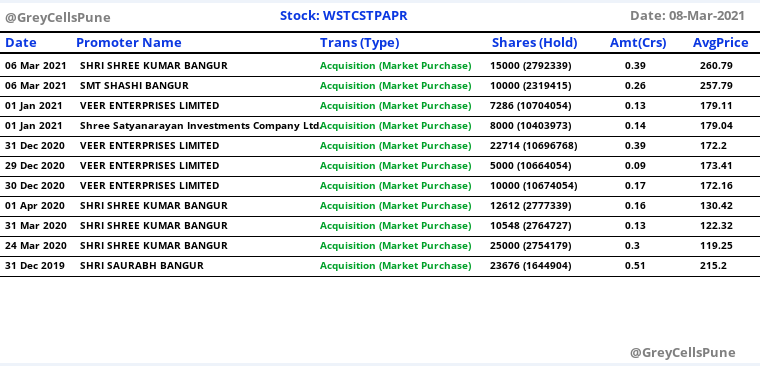

WCPM has successfully delevered over the past 2 years, and is practically debt free today. While a solid balance sheet positions WCPM to be one of the consolidators, a bank default in one of the group companies has created a stumbling block in the NCLT process. This means that expansion by WCPM has to be organic, making its desire of expanding its manufacturing footprint more challenging than its competitors. For instance, it was ruled out of the NCLT process for Sirpur Mills, which eventually has been acquired by JKPL.

Like the other majors, WCPM has also sought to control its supply chain for wood fibre. However, success has been somewhat mixed, and it still imports ~43% of its requirement of wood fibre. This exposes WCPM to price volatility of fibre, which has been a key risk for the industry in the past.

Above report has well covered analysis on JK Paper, west coast paper mills and Tamil Nadu Newsprint Papers Ltd. One go through the report to get an idea on the paper industry

Disc: no holdings

WCPM is one of the top paper companies in the country by size – it operates a 320,000 integrated paper mill, with sufficient pulping capacity, and a 75 MW power plant. An optimal size of the plant, it is amongst the more profitable paper companies in India today – FY18 EBITDA margin of 21.2%, and RoIC of 14.7%. WCPM also enjoys adequate supply of water, a key ingredient in paper making, ensuring a disruption free production schedule.

WCPM is one of the top paper companies in the country by size – it operates a 320,000 integrated paper mill, with sufficient pulping capacity, and a 75 MW power plant. An optimal size of the plant, it is amongst the more profitable paper companies in India today – FY18 EBITDA margin of 21.2%, and RoIC of 14.7%. WCPM also enjoys adequate supply of water, a key ingredient in paper making, ensuring a disruption free production schedule.