Thanks sirji.. hope November and december sales data show good improvements in coming days.

Baby step in further backward integration

5 Likes

From the latest presentation . Efficiency levels have improved for cell from Unit 1 + unit 2 production started + Module output improved for Oct + Nov . Q3 should be much better than Q2. Valuations have also become very attractive….

Disc: Holding

2 Likes

Could not find this interview on YT.

Some important points covered

websol mgmt on ndtv profit

q3 guidance

- some deficit will b there in earlier guided 500 cr

- impacted by delayed take-off from some client due to expectation of lower prices & inventory mgmt

- also prices saw some 10% softness in last 2 months

- trying best to reach target & come v close to what was announced

ingot/wafer - linton mou

- will come later, lot of prep works to be done

- next 6 months understanding the tech since it is new area & train websol’s people

have a look at video for more details..

2 Likes

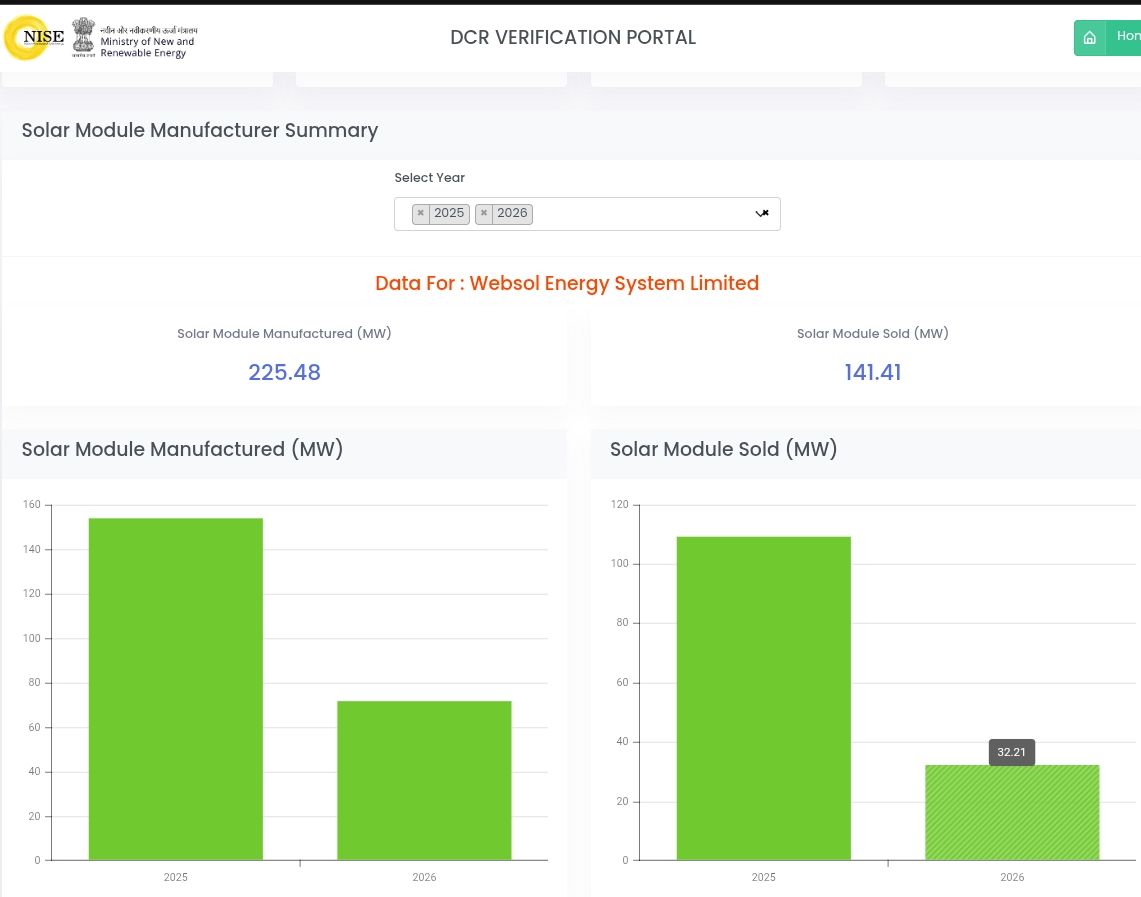

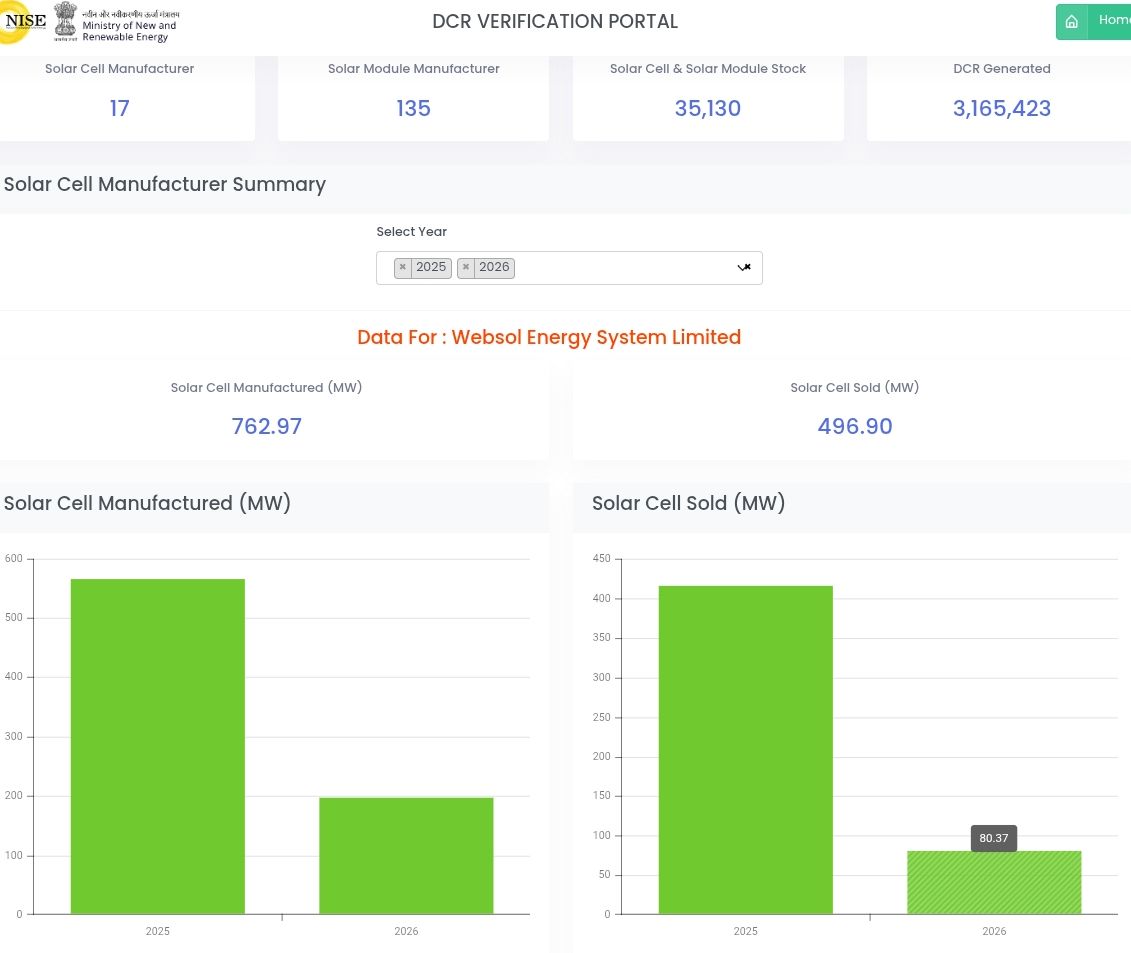

Still Sale data very weak on DCR Portal..

Any insights behind why the sales is substantially lagging the production on DCR portal data as on today? This doesn’t seem to be the case for other companies.

Doesn’t that have to do with captive consumption by their module line?

they have mentioned in concall…whether it is cell sales or module sales…both counts as dcr sales. hence, data should reflect either sales.

i am unable to understand websol don’t deserves this kind of valuations, inclusive of all concerns on overcapacity or say high public holding, DCR data is updating on time 80MW till date, but stock is not reacting at all, it is available at far below in terms of valuation in compression with modules manufacturer. This is what happens when we invest in sun set industry where no one cares about its growth or future expansion, really disappointed with this script

solar cell demand was high in nov-dec 2025 quarter due to almm-II guidelines to be implemented from june 1, 2026.

whereas websol management mentioned in concall that in the same quarter off take was slow due to softening of prices.

both statements don’t match.

one is fact and other we have to trust management which is decreasing with every quarter.

what i sense is, is there decreasing of demand for mono-perc cells? which looks like it becoz demand for cells doesn’t seems to be a problem, however company is not able to sell their production.

1 Like

mono-perc made modules date is counting.

industry is shifting towards g12r topcon fast.

main concern is even if websol transition existing capacity to topcon, how much time it has to stop production? and they have to as mono-perc demand will decrease increasingly with every passing quarter.

Only saving grace, will be if they transition when there new topcon cell line comes only, which is very far away july 2027, who knows by then what mono-perc demand will be there?

1 Like

Their sales for modules on DCR portal seem to have got better for month of March

Yes, no drastic increase but seems better overall. This is taken from DCR portal 2 days ago, comparing 2025 and 2026 YTD.

Module and cell output is much higher. But cell sales are flat, maybe used in house for module manufacturing (which is not counted towards sales?). Module sales are little higher. There is still time left for the current quarter.

Disc: invested

1 Like

Websol is forced to forey into G12R cells finally.

ALMM List-III for Ingots and Wafers effective from June 2028.

3 Likes

Looking at the DCR portal figures, there seems to be a large enough mismatch between production and sales. Typically, websol has not shown large inventory figures. So, does this mean that products are being sold as non-DCR? This is something that management always denies.

Also, if anyone knows whether the new cell line is already listed under the ALMM? I recall the management saying in the Q3 results con call that it’s going to happen soon. DCR portal seems to show the expanded capacity is working.

EDIT: It seems expanded cell capacity is already in ALCM list since November 2025

Taken from here:

ALCM or ALMM-2 rules only start from June so inventory build up is a possibility.

Disc: invested

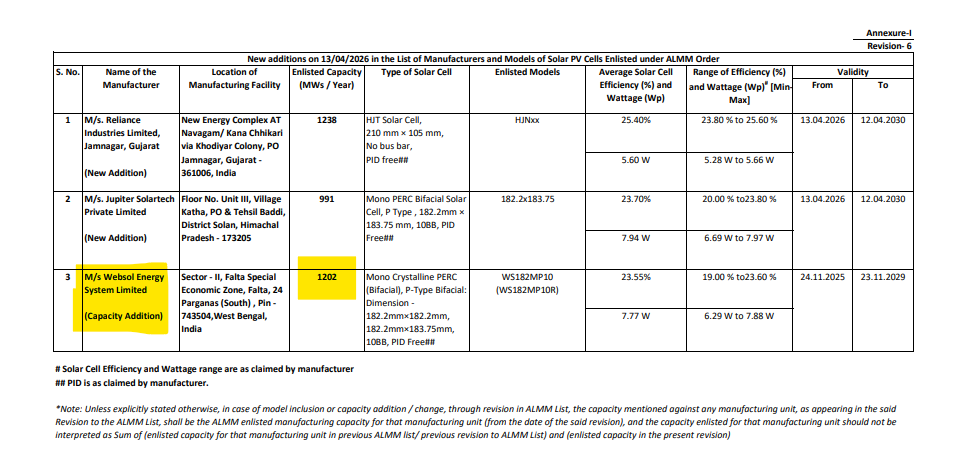

Another 600 MW added to ALMM List-II effective from 13th April. So, the full Cell capacity can be sold to DCR market. Reliance entry is also to be noted.

4 Likes

More than 100 Acres of land was alloted to Websol Renewable Pvt. Ltd at Naidupeta SEZ, AP on 06th April 2026. Sale agreement (lease deed is pending).