I heard about this company several months ago but I could not find much information or reports about the company.

This is a company in auto technology and anciliary sector, but has a world-wide presence and supplies hi-tech products to OEMs and major auto companies in the world as well as in India.

The company is debt-free, and financials look decent until 2012. This has has not been good so far due to slowdown in the auto sector.

Any idea about the quality of management, comments on their business model, products, etc. What could be the strengths and risks that one should watch out for this company?

Its a good company as per my info & hold if you are long term investor. Some merger or takeover or buyback some news will we announced. Look for Big targets ahead.

This stock was for me as free gift due to my holdings in Sundram Clayton.

Wabco is USA based company and having good business in Air Brakes and Disc Brakes systems. In India there are likely to be major changes in safety rules regulations in small and medium sector 4 wheeler. If Disc brake is made compulsory i see good fortune for this company after 2016. Floating stock seems to be too low and many good FII and MF have collected decent qty from market.

This stock was for me as free gift due to my holdings in Sundram Clayton.

Wabco is USA based company and having good business in Air Brakes and Disc Brakes systems. In India there are likely to be major changes in safety rules regulations in small and medium sector 4 wheeler. If Disc brake is made compulsory i see good fortune for this company after 2016. Floating stock seems to be too low and many good FII and MF have collected decent qty from market.

Why is the payable days so high for wabco? when it has almost a monopoly in braking systems for cv and it is one of the preferred source for export to parent company ?

WABCO

With the change in the holdings, the overhang of delisting is gone. Happy to see that the firm will remain listed. and now with 25% floating stock, we can expect FII to get back in to this counter…

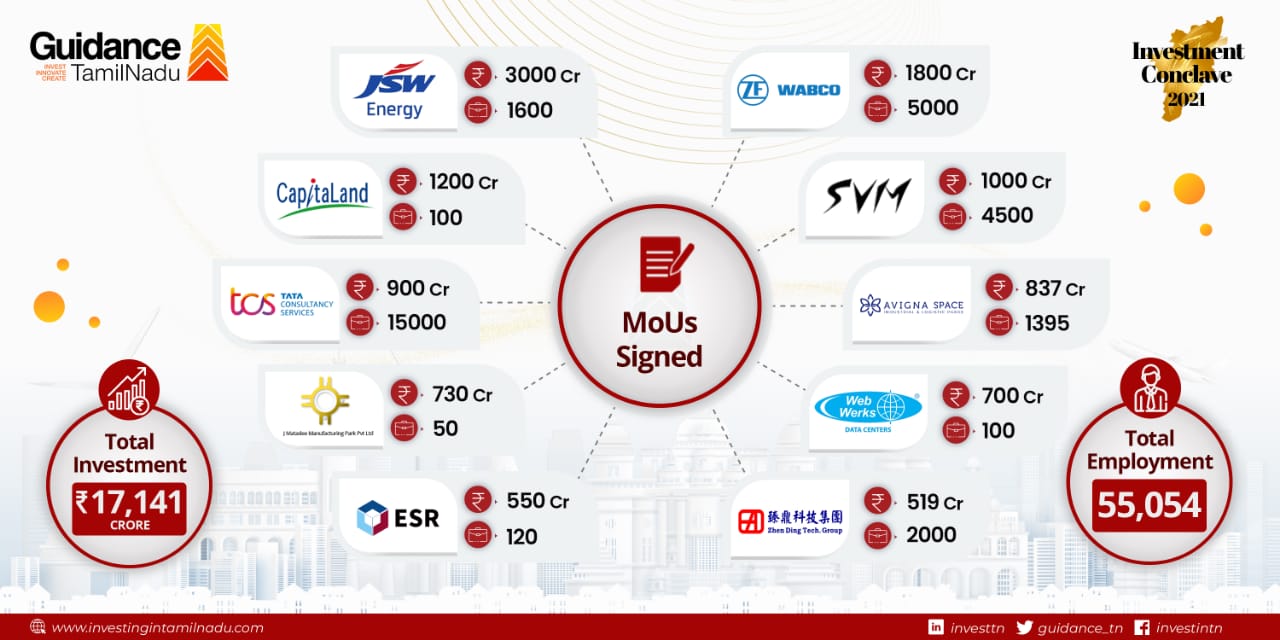

Inline with their Q4 PPT, Concall and Parent ZF interview, 1800cr Capex announced in Guidance Tamil Nadu investment summit.

Wabco India is emerging as export hub and their frugal innovation is key for good growth in topline and bottom line. Worth holding. Sip during declines. Have 7% of my portfolio.

Planned capex is Rs 1760 Cr. Company wants to make India Rs 24000 Crore hub and plans to outsource Rs 16000 Crores worth products from here by 2030. For long term investors this should be a good company to accumulate.