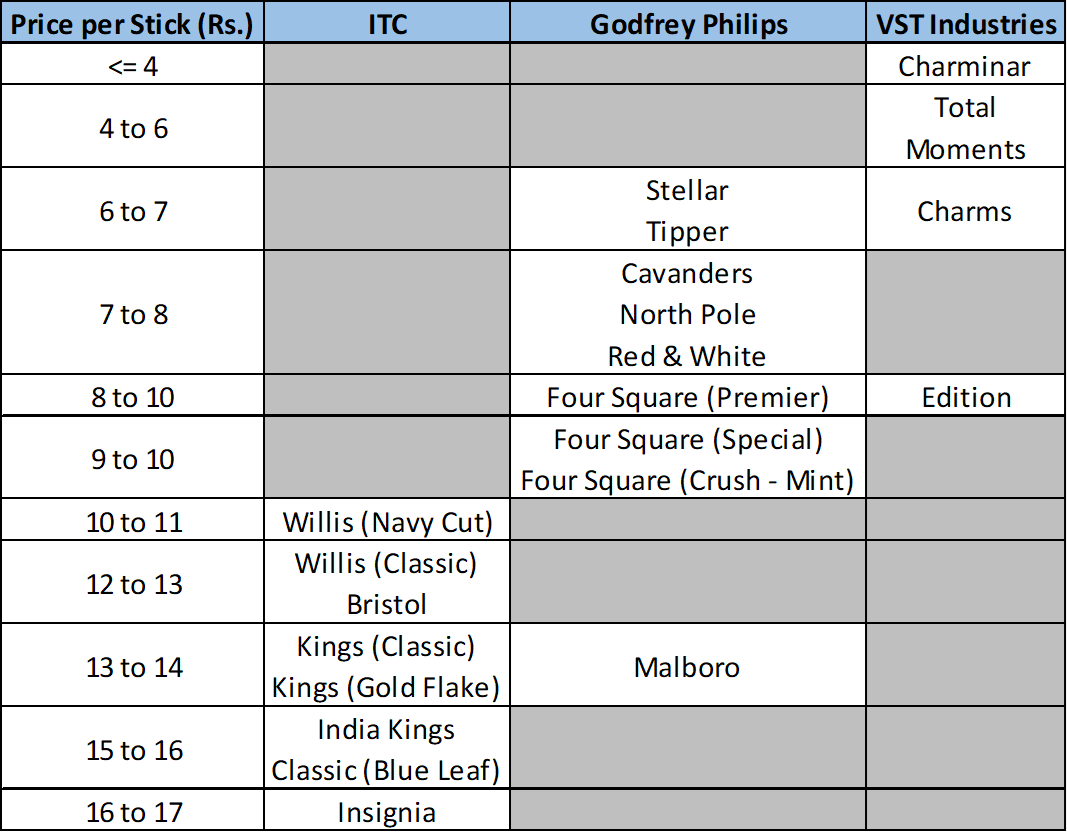

This is a little something I made for my blog. The prices may not be exact. But my aim was to show that all 3 players are more or less competing in their own territory and there’s minimal overlap.

25 Likes

Correct Dinesh and thanks for this table, best parallel would be check price of Charms (VST) and Capstan (ITC). Used to be same size 69 mm, and used a small price difference, Charms was cheaper by a Re. on a pack.

1 Like

“Cigarette volumes continued to see muted volume growth of 2-3% growth vs.~10% volume growth of VST Industries. ITC is losing market share as contribution of smaller size cigarettes is increasing and VST Industries & Godfrey are gaining volumes at expense of ITC.”

http://content.icicidirect.com/mailimages/IDirect_ITC_Q3FY20.pdf

4 Likes

VST, by their own admission, operate in the “value” end of the Cigarette market. That is why there is a difference in margins. I absolutely agree with Dinesh that there is very little overlap between their products. One of the factors could be that British American Tobacco has large stake in VST as well as ITC.

In regards to Cigarette volumes I have attempted to do a deep dive on this and have posted in ITC thread which is linked below

I used this information for a DCF model that I was making for VST Ind.

6 Likes

Nice set of results from VST . Strong Growth y-o-y

4 Likes

Can someone explain to me how excise duty has risen so much from last 2 quarters ?

Case study on VST by Professor Sanjay Bakshi -

Only for educational purposes.

4 Likes

3 Likes

7 Likes

HAS THE COMPANY LOST ITS WAY.

Management has decided in its “wisdom” to dilute 5% of the equity capital to incentivise employees , this after the company lost its KMP to ITC. One must remember this is a business where your customer is addicted to your product, you have pricing power & things don’t change much competition wise. If this was done to correct a wrong then it seems the management is on a roll doing more of what it wanted corrected in the first place.

Payout to shareholders was reduced from 78% to 52.5% sighting covid related prudence. The same prudence seems missing when shareholder interests in the company are being diluted permanently by 5%. Unlike other companies buy backs are not possible in this case to ameliorate the harm done by dilution.

As Warren Buffett rightly said “If earnings have been unwisely retained, it is likely that managers, too, have been unwisely retained”.

Disclosure- InvesTed

9 Likes

The concern about dilution of equity is valid. However, the company has competition not only from tobacco industry but also other industry to get good manpower. Given the negative perception of business, very few bright minds would like to associate with so called “SIN” companies. Hence, I do not see move to provide ESOP as extremely negative. The ESOP are valuable only if market capitalisation increase. Something similar to compensation to management as commission of net profit. I am more than happy in case management get higher remuneration due to growth in profit (assuming profit is sustainable and not one time accounting innovation driven). Similarly, if company market value does not go up, even ESOP are not going to yield much reward to management. Something crudely one can look at ESOP in ITC issued almost 5-7 years back, are still not greatly rewarding to the management.

Secondly, in case we feel, the management remuneration is very high, we may express our view on voting and try to oppose same at various forum like in AGM.

Thirdly, decline in dividend was categorically said to be one time due to COVID related issue. I would wait for one more year dividend declaration before finalising my view about unfair treatment to minority shareholder.

@mustafa Thanks for bringing out negative point of VST Industries and appreciate your efforts.

Disclosure: My view may be biased due to my holding in VST. Not a SEBI Registered advisor. Not recommending investment action in the company.

8 Likes

5% of paid up capital is huge for any company to issue ESOPs in one plan, definitely for a company in tobacco industry where there is no marketing/promotion, no threat of new entrants into the industry. Procurement, Production and Distribution are the key drivers of the Business Growth in company’s control as Companies have limited role to play in other key drivers (Regulations, Taxes, Illegal cigarettes, other forms of tobacco consumption, etc).

Any information on exercise price and vesting period for these ESOPs?

Does this resolution require simple majority only from shareholders?

Disclosure: Invested.

1 Like

I am currently not a Shareholder of VST Industries. I have just been tracking it for a while.

On the topic of this dilution, I don’t think the impact will be much. But whether it is actually used to incentivize better performance at the mid or top level should be tracked.

Maybe VST lost a KMP to ITC because ITC offered Stock Options? It could very well be, since ITC has been issuing ESOPs left and right every year.

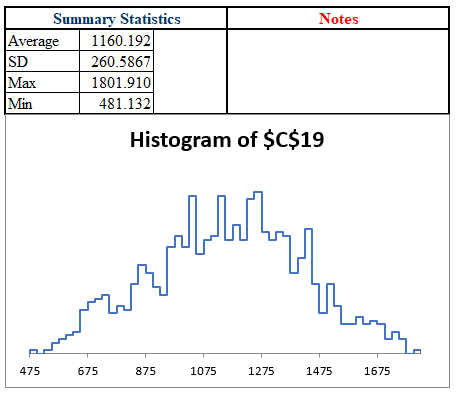

Right, on to assessing the impact of this issue. I got a Option Valuation template from here. Since we don’t know some of the inputs, I am going to use assumptions in ranges.

- Stock Price: Rs. 3,767.

- Exercise Price: Rs. 3,000 to Rs. 4,000.

- Expiry: 2 to 5 Years.

- Risk-free Rate: 4% to 7% (Current is about 5.9%)

- Standard Deviation: 20% to 30% (When I Valued VST for my blog, it was around 26% if I recall correctly)

If we run a Monte Carlo Simulation (1,000 Repetitions) with the above assumptions, we get the following results:

This means, on average, the current Shareholder is going to be diluted by Rs. 1,160. Of course, only 7,70,000 Options/Warrants are going to be issued. So, at a total level, the current Shareholder is going to be diluted by Rs. 89 Crores or so in today’s Rupees.

Even in the worst case scenario that the Options offered are very lucrative, the dilution might be closer to Rs. 1800 a Share and for 7,70,000 Options/Warrants, it will be about Rs. 140 Crores in today’s Rupees.

Rs. 89 Crores and Rs. 140 Crores are respectively 1.53% and 2.41% of the current Market Cap of the company, which isn’t much at all in my opinion.

10 Likes

VST ESOP Postal Notice.pdf (134.2 KB)

PFA the postal ballot notice for VSTs proposed ESOP. Has a lot of legal jargon , would appreciate views about the fine print.

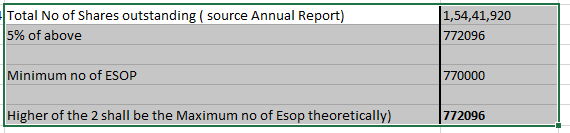

While I am not legal expert and also have limited understanding, from the reading of notice, I find this is enabling resolution for VST Ind to set up trust and allow Nomination & Remuneration Committee (NRC) to set up Criteria, Eligibility, Pricing and quantity of ESOP to employee. At respective period, NRC would decide the allocation based on performance parameter for individual employee. It restrict maximum allocation to 1% of equity and Total ESOP at 5% of Paid up capital or 7,70,000 share, whichever higher

2 Likes

As of 30-March-20 employee cost is 8.6% of sales which comes out to be ~106 crore, in this context cost of ESOPs (80-140cr) is a significant expenses. Company should also be transparent about what kind of performance targets are placed for such kind of rewards? For steady state business like VST cost savings and sustaining the existing the customers/market share is primary focus than growth . It is true that they can’t compete with other players in the industry due to singular focus and hence difficult to attract and retain the talent but they have to find a way out of it / live with it. I am not expecting any leadership to make miracles in this business irrespective of any quantum of rewards. I know companies, who have stopped such HR practices years ago as salary itself it the reason why employees should deliver the performance when industry itself is stagnant.

1 Like

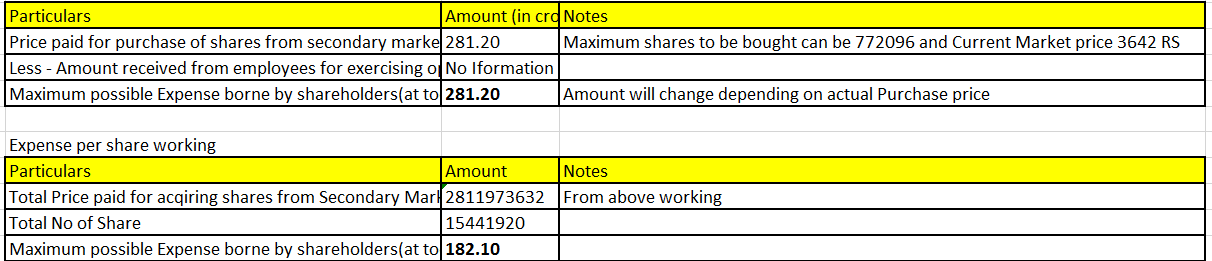

Hello All,

Below is my understanding of Employee ESOP Scheme for VST Industries (which may be imperfect or totally wrong)

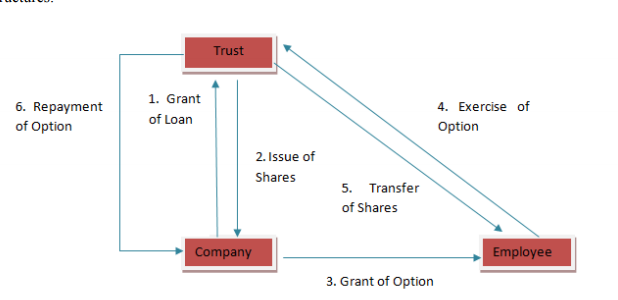

1-The ESOP scheme is going to be implemented under Trust Route and not Direct route ( Source annexure to Notice).

Hence there will be no Dilution of Share Capital Whatsoever.

2-Under Trust Route , the Company sets up Trust, then “lends” money to Trust and Trust buys shares from Secondary Market and this stocks are allotted to eligible employees

3-The Total No of Stock option is 770000 or upto 5% of Paid up share capital, Which ever is higher

4-

5-The Trust Shall buy maximum of 2% of Paid up share capital in any single year. ( hence the Purchase of stocks will be spreadout atleast over minimum of 3 years

6-Expense borne by the Current shareholders for ESOP - Accounting technacalaties apart (Esop-Accounting)

My understanding and I am highly sceptical of my working (Please make your own calculation)

7- In my opinion the maximum a shareholder will lose is Rs 182 per share and that will be spread over a period of 3 years and based on Current Market Price and assuming no money is recieved from employees on exercise as that information is not given

8 - If i have made any mistake in workings or have misunderstood any part, the please correct me.

9 - Disc - Invested in VST industries

Thanks

Harsh Shah

6 Likes

RKD has purchased another 16000 shares in VST in Q3FY21 as per the latest shareholding pattern.

1 Like

Its an incredibly opaque proposal. Its rather shocking that we are seeing this from the likes of VST which has very high standards of corporate governance amongst Indian companies. I am putting their proposal in the form of the conversation below:

VST: Hey Shareholder, wassup

Shareholder: I am good. I look forward to your amazing dividends every year but off late they are reducing.

VST: We can talk about dividends later. Right now, I need you to vote & approve our Employee Stock Option Plan called VST-ESOP 2020. I need this plan to attract & retain employees in our company.

Shareholder: You are a mature company in a mature market and had a volume CAGR growth of only 1.5% in the past decade. I thought ESOPS are more common in fast growing companies. However, I am willing to consider your ESOPS but have some questions.

VST: Sure, ask away

How many ESOPS are we talking about?

7.70 lac shares or upto 5% of paid-up capital, whichever is higher. This ceiling can be exceeded in case of bonus/splits. It can also be exceeded for other reasons such as rights issue, merger/sale, etc.

Will my shareholding be diluted because of these ESOPS?

I have good news for you buddy. Your shareholding will not be diluted because we will setup a Trust which will purchase these shares from the Stock Market. This Trust will buy shares from the market in tranches and in a year the Trust will not buy more than 2%.

That sounds great! But how will this Trust get the money to purchase these shares for the ESOP

Ah! The company will give the Trust a loan to buy these shares from the Stock Market. I assure you that the Trust will pay back the money to the company

What interest rate will the Trust pay the Company and when the money be returned back?

The loan is interest free. Also the Board/its committee will decide when the money is to be paid back to company by the Trust.

(NOTE: This would mean that your dividends may reduce atleast until the time the money is paid back by the Trust because some of that free cash will be utilized to buy these ESOPS)

How much will an employee pay the company for these ESOPS?

Oh, you mean the exercise price. It will be more than Rs 10 (which is the current face value of the shares) but I cannot tell you more as the Board/its committee will decide. I know the current stock price is Rs 3,762 but still I cannot tell you more.

On what terms will an employee get ESOPS

The Board/its committee will decide the performance metrics. The maximum ESOP to a single employee will not exceed 1% (that’s worth Rs 58 crores at today’s market cap). An ESOP will not vest earlier than 1 year and upto 3 years from the date of giving these ESOP and the Board/its committee will decide the exact details. Also, the exercise period is 4 years from the date of vesting of the ESOP but the Board/Committee may decide something else if they wish to

Shareholder: Dear VST, the key parameters in your plan are very vague. Also a large amount of discretion seems to be given to the Board.

VST: I know but I want you to be like Mowgli when Kaa looks into his eyes and says TRUST IN ME. Oh, and one more thing, the Board/its committee can change this plan without asking you.

The above, ladies and gentlemen, is the plan that VST is asking its shareholders to approve. In an ideal world, the impact of ESOPS can be estimated using Black-Scholes (just like how Dinesh has done above). However, because this ESOP plan is so vague and key inputs for the same have not been given the company the method used by Harsh1 (even though it is over-conservative) can be used as a worst case scenario. You can deduct Rs 77 lacs from the Rs 281.2 crores calculated by Harsh1 as an employee will pay atleast Rs 10/share as proposed by the company

Disclosure: I am not a shareholder in VST Industries but I always have been interested in it.

24 Likes

Appreciate your view point and also approach to bring out concerns so lucidly. Having said that, consider the situation: Your MD are poached after wonderful performance over 3 years in difficult business circumstances, after constantly gaining market share over tenure. He has got job with the largest competitor who has around 80% of market. You need to attract good talent to preserve your market share first and then to grow. While Cigarette has advantage of limited competition, still there is moderate competition among players. Also, BAT the common owner in VST and ITC (in past ITC was also marketing arrangement with VST Industries as per my memory) despite that this shift is happening.

At this stage, I have no view on ESOP. Per se not against ESOP, subject to interest of shareholder and management are properly aligned. The real issue would be what term, whom and what performance targets are set. If the committee set easy target with low price, the shareholder would suffer. The key would be set proper performance parameter and ESOP scheme. Unfortunately, we would know that only after 3-5 years.

Hence, in my limited understanding, I would approve ESOP scheme as enabler. However, cautiously watch development and term of ESOP scheme. If I find same are very favourable to employees, then I would consider to express my desire by voting against appointment of directors being first step to exit from company as investor being final.

Post Q3 decline in Sales and Net profits (over Q2 as well as Q1), waiting for other players results to understand whether there was industry issue or company specific issue about change in top management during quarter. Also, I would really appreciate if management provide some release to provide way forward on business.

Discl: Among my Top 10 holding. No trade in last 90 days. My view may be biased. Not recommending any investment action

4 Likes