Hi

I did not know which thread to put my thought process down around core principles to stick to during these times (and even before). I have been a core believer in return on capital coupled with sales growth as that is what leads to value creation.

The hypothesis for me was to stick around those buckets of companies (in the non finance space) which have low debt and high ROCE and sales growth. If these companies were ‘really’ good they would be getting the least impacted in this turmoil relatively speaking.

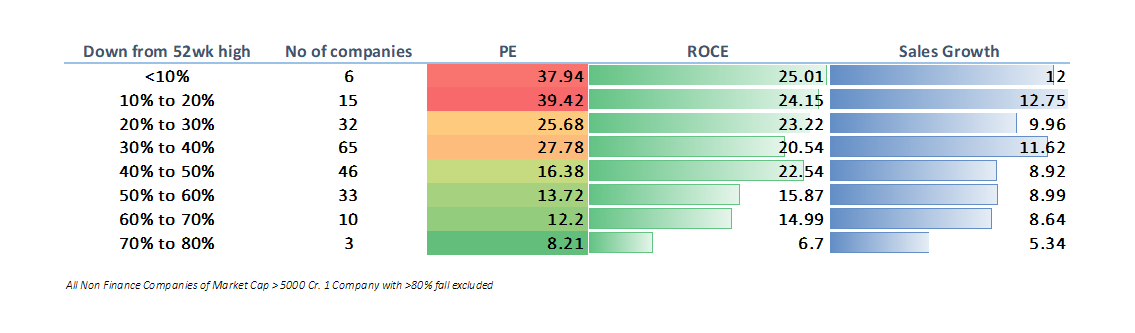

So I looked at all non finance companies with market cap greater than 5000 Crs. There were 211 companies (I omitted one loss making company as it was an outlier with >80% fall in price).

Here are the results.

The most resilient companies are perfectly correlated directly to their returns on capital and sales growth.

For me personally it clears the clutter in my mind as to which companies to focus on always.

Regards

Deepak