@Donald read through your explanation of the model. It seems to me that Self Reinforcing Business Model seems to have a strong dose of Network Effect.

Pat Dorsey described Network Effect as

Businesses that benefit from network effect are very similar; that is, the value of their product or service increases with the number of users

Now, this is strikingly similar to your examples, quoting one here

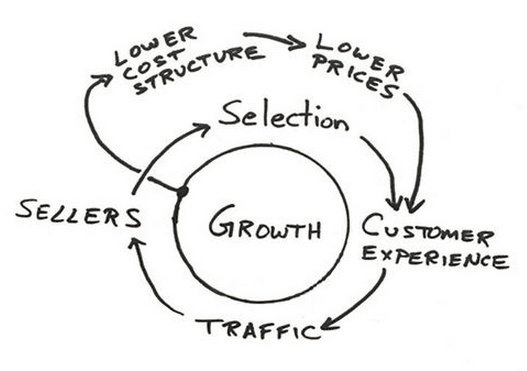

The more Business Segments you have, you bring in more adjacent customers. The more customers come into the addressable pool, the more business segments you can serve. The more business segments you can serve, the more Retail Points of Sale you can address. The more Points of Sale you have they bring in their own set of new Customers, which again addresses the customer pool …and better targeting …

Dorsey exemplified Network Effect in Card Networks (Visa, Master, Amex) due to their huge network where the cards are accepted. The more places you can use your Amex card, the more valuable that card becomes for you. The more valuable it is for you, more places would accept the card. He further explained that Network Effect is much more common among businesses based on information or knowledge as information is a “nonrival” good as called by economists.

Now these explanations are quite applicable for the BFL example. The Core competence of BFL being Analytics engine (per your note) which is clearly knowledge. BFL has done well to create a huge network of points of sale and responding to customers at “velocity”. The better network and velocity of BFL leads better value for customers and then to stronger network has been described well by you

It impacts Customer Cross Sell - Why? because it has in-built customer Sales and Risk Profile (Payments history). The more BFL Cross-Sells the Richer is the Sales/Risk Profile. The Richer the Sales/Risk Profile, the faster is the Approval Velocity. The faster is the Approval Velocity, the better is the Customer Experience. The better is the Customer Experience, the more he is pre-disposed to a Sale. The more Customers take the Loans, the more delighted is the Retail Partner. The more delightes is the Retail Partner, the more likely he is to recommend BFL.

So I’m trying understand the delta between Self Reinforcing Business Model and Network Effect. It’s just easier to add to model than getting a hang of a completely new model

Thanks!