Company Overview

Viviana Power Tech is an integrated EPC player in the power infrastructure space. Founded in 2014 and listed on NSE Emerge in 2022. It operates within the capital goods universe, with a focus on power T&D EPC projects.

Business Model

Two key segments:

- Power EPC (Core Segment): Turnkey services for power T&D. Viviana handles everything from design and supply to erection and commissioning of transmission lines and substations up to 400KV. Clients include both government utilities and large private developers, particularly in renewable energy.

- Transformers (Newer Segment):

Through its 75% acquisition of Aarsh Transformers Pvt Ltd, Viviana has entered into transformer manufacturing. The product mix spans power and distribution transformers, compact substations, RMUs, electrical panels, and related components. They are planning to use transformers for captive needs and also as a standalone revenue stream.

Financials

-

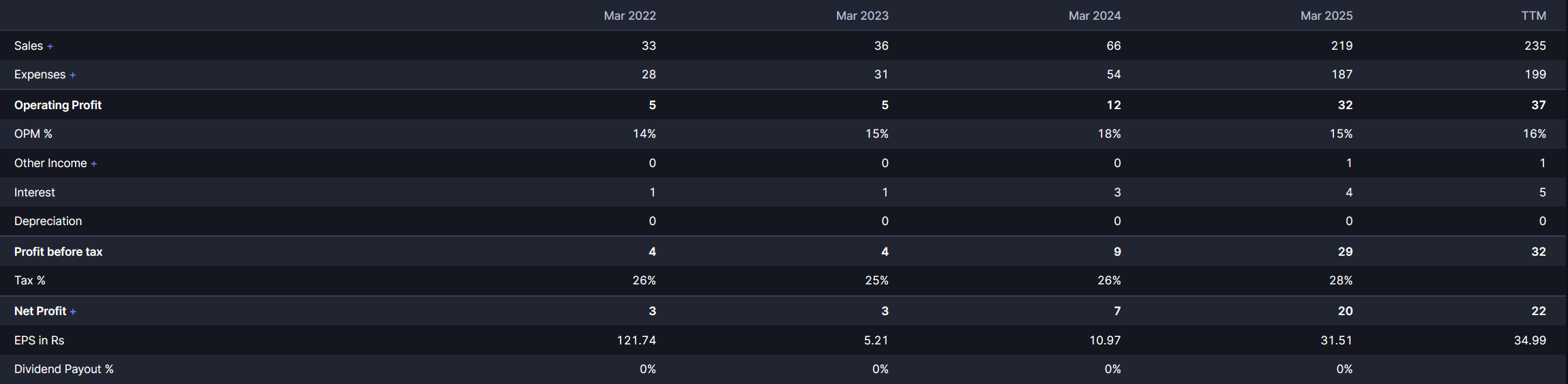

Income Statement:

Source -

Balance Sheet:

Source -

Cash Flows:

-

Working Capital:

Source -

Shareholding:

Source -

Efficiency Metrics:

Investment Rationale

Viviana looks well positioned at the intersection of sector tailwinds and its own expansion strategy.

-

Industry Tailwinds: India is targeting 500 GW of renewable capacity by 2030. Add to that grid upgrades under the Revamped Distribution Sector Scheme (RDSS), and you get a multi trillion rupee opportunity. As a power EPC player, Viviana is directly aligned to benefit. The government’s infrastructure focus provides a long-term, structural growth driver for the entire sector.

-

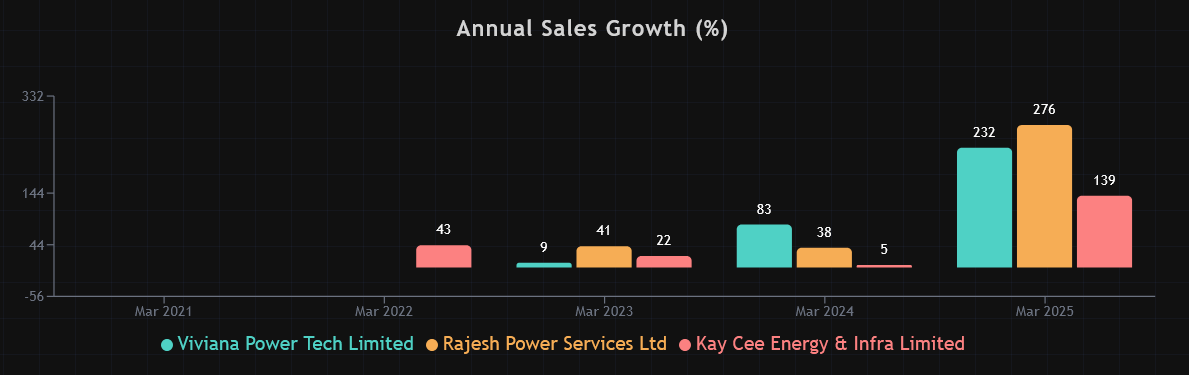

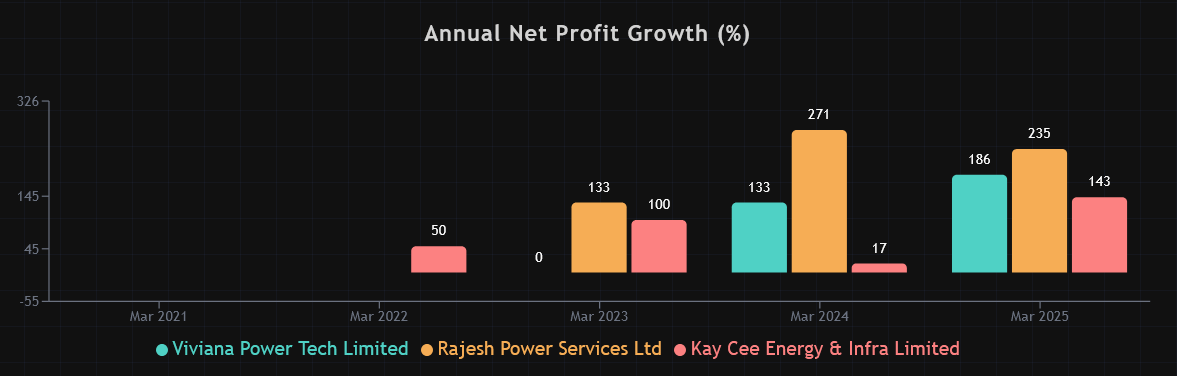

Explosive Growth: The company has demonstrated explosive growth, with revenues surging 232% and profits growing 186% in FY25. Company achieved it while maintaining a strong ROCE (42%) and ROE (33.33%).

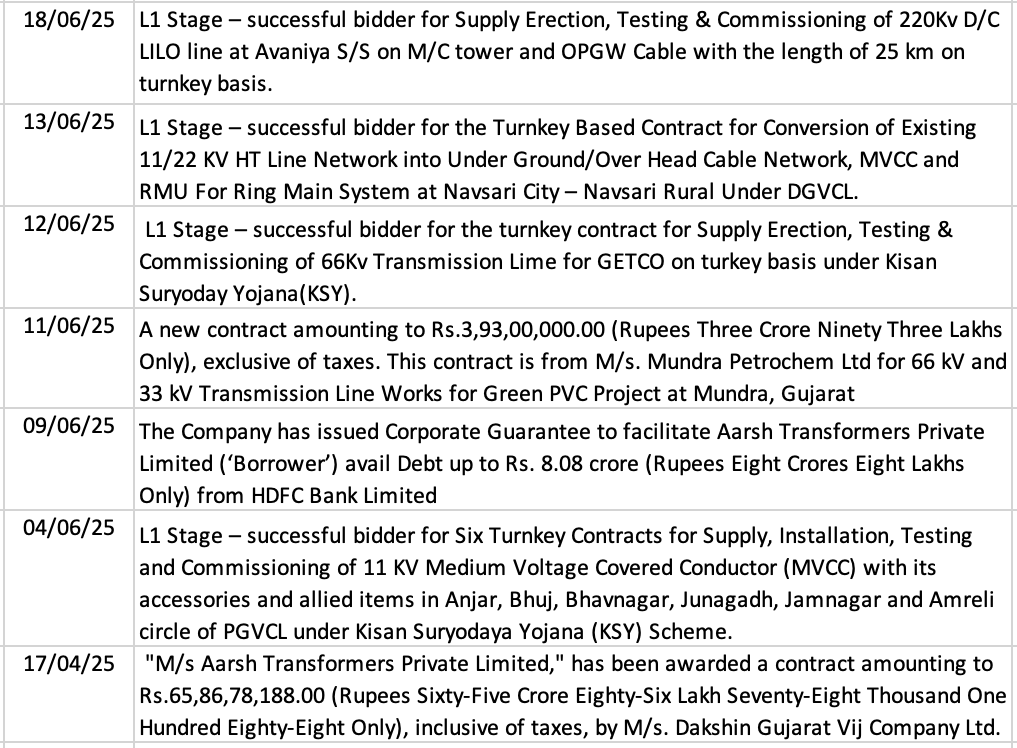

The unexecuted order book stands at ₹1,000 Cr. Source: Link

Recent Order Wins:

Source: Link -

Expansion into Transformer Manufacturing: This backward integration strategy provides them with a captive market for their transformers while also opening up new revenue streams. Revenue potential >50cr.

-

Proven Execution & Marquee Clients: In the EPC business, execution is everything. Viviana has built a strong reputation by working with marquee clients like Adani Green Energy and Gujarat’s state power utilities.

-

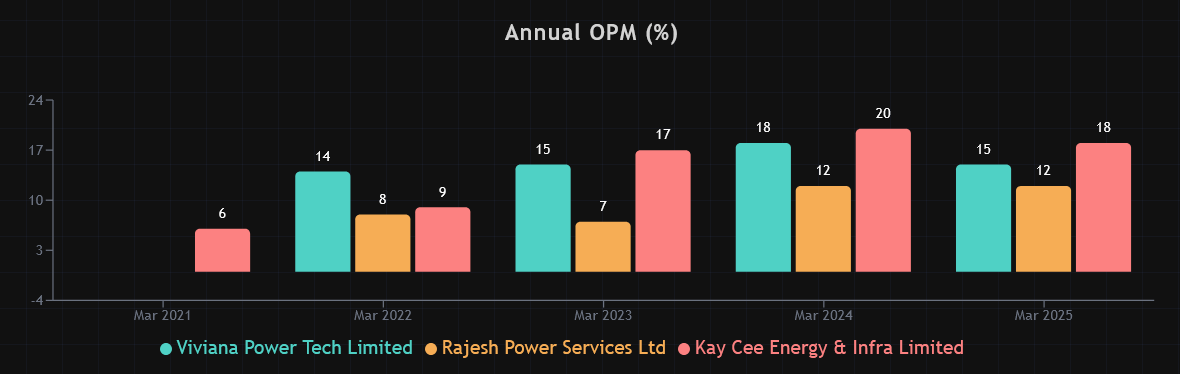

Shift Towards Larger, Higher-Margin Projects: The company is strategically moving away from smaller projects and subcontracting roles to focus on larger turnkey projects, where they supply all materials and have greater control over margins. This shift is evident in the changing composition of their cost structure, with material costs now accounting for 75-80% of project costs.

-

Main Board Listing: Company’s plan to shift from SME platform to the main board (NSE) could unlock greater liquidity and attract institutional investors.

Industry & Macro Tailwinds

- Policy Support: The Revamped Distribution Sector Scheme (RDSS) , with an outlay of over ₹3 lakh crore, aims to improve the operational efficiency and financial sustainability of DISCOMS. Viviana has already won significant projects under this scheme, highlighting its ability to capitalize on these government programs.

- Sectoral Cycles: India’s per capita electricity consumption is still well below the global average. With a rising population, increasing urbanization, and the adoption of electric vehicles, the national power demand is projected to double in the next decade, ensuring a sustained, long-term demand for power infrastructure.

- Size Of Opportunity: Hyperscale data centers are energy hungry. Unlike traditional IT workloads, AI servers run hotter and around the clock. Utilities worldwide are already flagging capacity constraints. For India, where data centers are accelerating, this represents a structural demand driver for T&D infrastructure.

Jensen Huang (Nvidia CEO): “Every single data center in the future will be power limited…We are now a power limited industry.” Source: Link

Sam Altman (OpenAI CEO): “Eventually, the cost of AI will converge to the cost of energy.”. Source: Link

Competitive Advantage

-

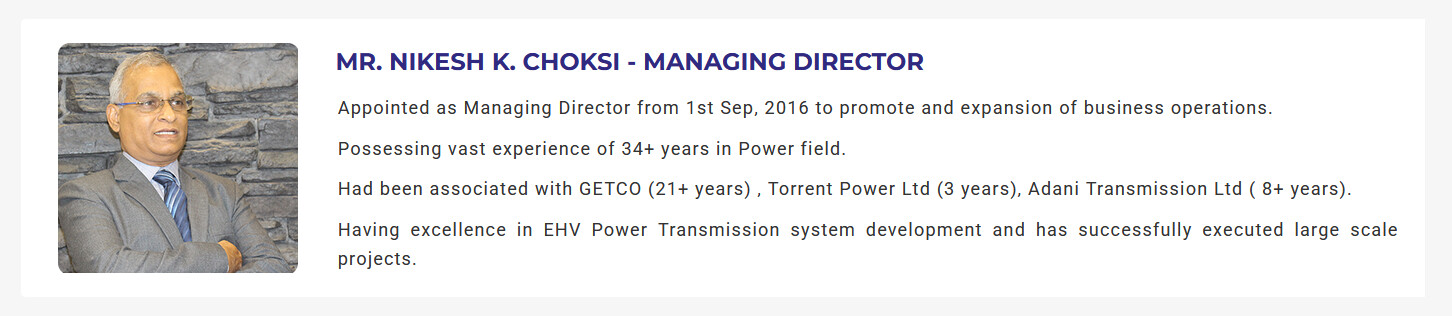

Management Expertise: The promoters bring deep domain knowledge to the table. Chairman & MD Mr. Nikesh Choksi has 39 years of experience, while his son, Whole-Time Director Mr. Richi Choksi, has 13 years in the power infrastructure industry.

-

GETCO is set to invest Rs 1 lakh crore over the next eight to 10 years to build additional transmission infrastructure Source. Viviana is a prominent player in Gujarat and promoter Mr. Nikesh Choksi is ex-Getco with 21+ years of association with them. The dots are there to be connected.

Governance

-

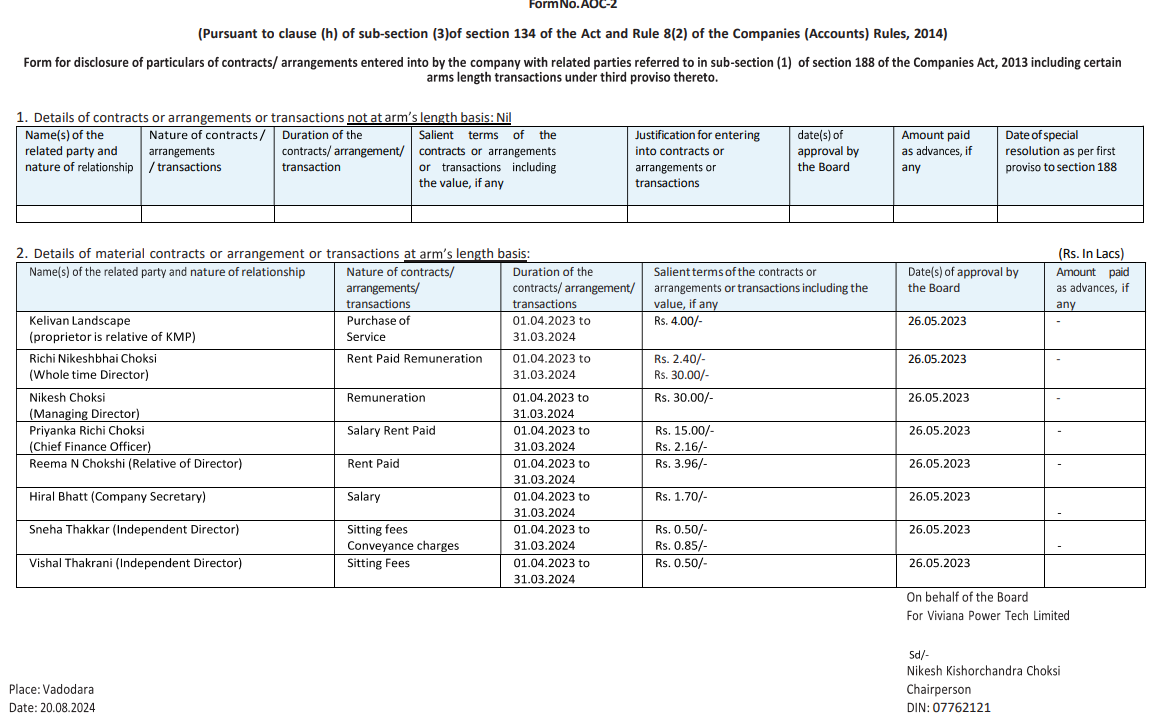

Related Party Transactions: Limited to rent and some service arrangements with promoter linked entities.

-

[Minor] The Secretarial Audit for FY24 noted delays in certain regulatory filings, such as XBRL format submissions and insider trading disclosures.

Risks

- Lack of Moat: EPC is largely commoditized. Projects are awarded via L1 bidding (lowest cost wins), so differentiation is mostly in execution. Margins remain thin and customer loyalty is low.

- Client Concentration: A significant portion of revenue comes from a few large clients (Getco, Adani). Any delay or cancellation of projects from a key client could have a material impact.

- Transformers Oversupply: According to concalls of multiple transformer players in India, the industry is likely to enter an oversupply phase by FY28, suggesting that new entrants may be late to the transformer party.

- Risk of Project Delays: The company learned valuable lessons from past experiences with project delays in transmission line projects, particularly those involving right-of-way issues. They are now focusing on projects where right of way is the client’s responsibility, minimising the risk of delays and cost overruns.

- Dependence on Government Spending: Much of Viviana’s growth is tied to government backed spending in T&D. Any slowdown in funding or policy shifts would hurt visibility.

Disclaimer: Invested