Note: There is very little information about this company available in public sources. AR is not very informative; there are no credit rating reports as it is debt free; no presentations or concalls; website is very elementary.

Vistar Amar (earlier known as Shubhra Leasing Finance and Investment Company) is into manufacturing of fishmeal. Fishmeal is a commercial product made from wild-caught fish, bycatch and fish by-products, to feed farm animals like pigs and farmed fish. Hence, fishmeal is an input into the aquaculture industry.

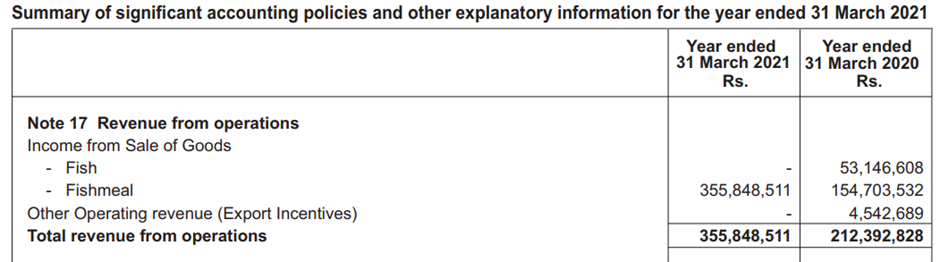

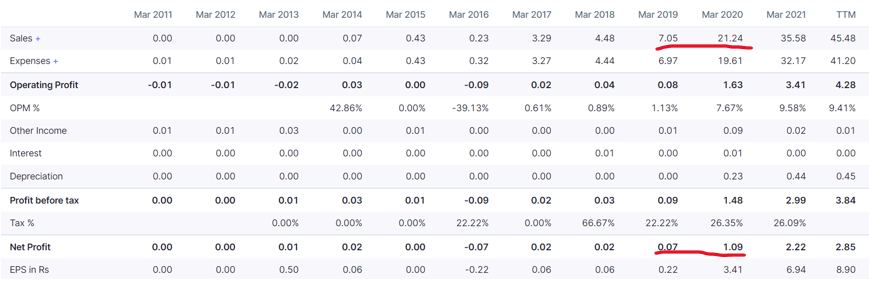

For a long time, the business was stagnant but there was a sudden change in FY20 (sales tripled and PAT grew 10x) without significant other income which has sustained.

There seems to be a renewed management focus and the reason was that earlier they were only doing trading of fishmeal. In FY20, they began processing/production of fishmeal.

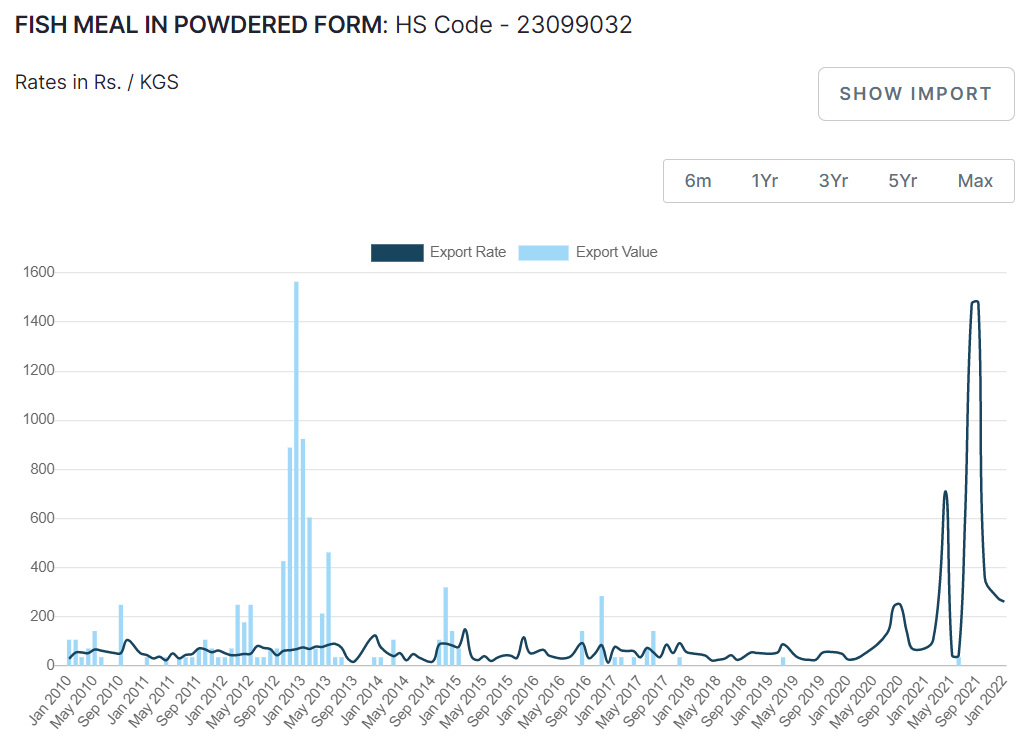

Aquaculture industry is expected to grow at a fast pace and this will lead to strong demand for fishmeal.

In FY21, they changed equipment to increase capacity by 50% to 30-35 TPD.

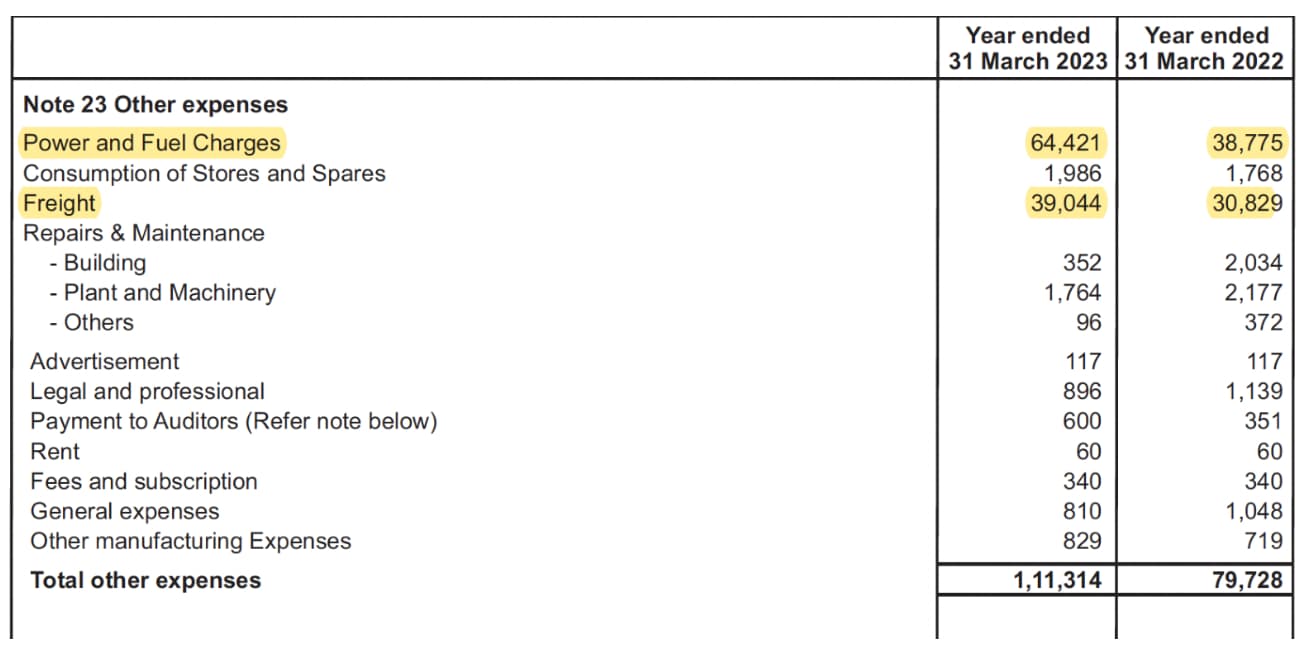

They are also taking steps for cost cutting.

They have announced expansion of capacity.

The current promoters entered the business and old promoters resigned in 2016.

The company was supposed to be renamed as Vishva Amar, but perhaps due to unavailability of the name, it was kept Vistar Amar.

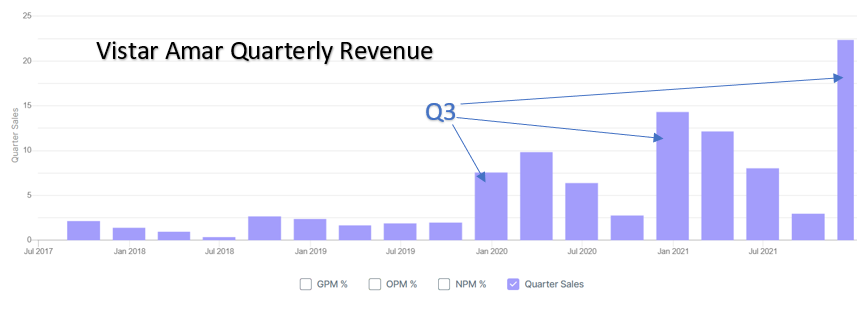

Q3 FY22 was a great quarter

The promoters (Rajesh B Panjri and family) have large experience in industry and have private limited entities (Hiravati Exports) in the similar business.

Hiravati Exports’ address is in Veraval, Gujarat

This is the same as the factory location of the listed entity

Disc- no holdings as of now. Will update disclosure as and when required.