This is Vishagan, working as a senior consultant with 11 years of experience in IT. I have been reading investment related books since 2017 & managed to find a cashflow model that helps me to maintain the healthy financial position to my advantage.

To talk about my investment journey, as an individual chasing financial freedom in early 30’s.

[Investment books I read to arm myself with knowledge. ]

I’ll start sharing my rational decision behind the investments in upcoming days. To start with

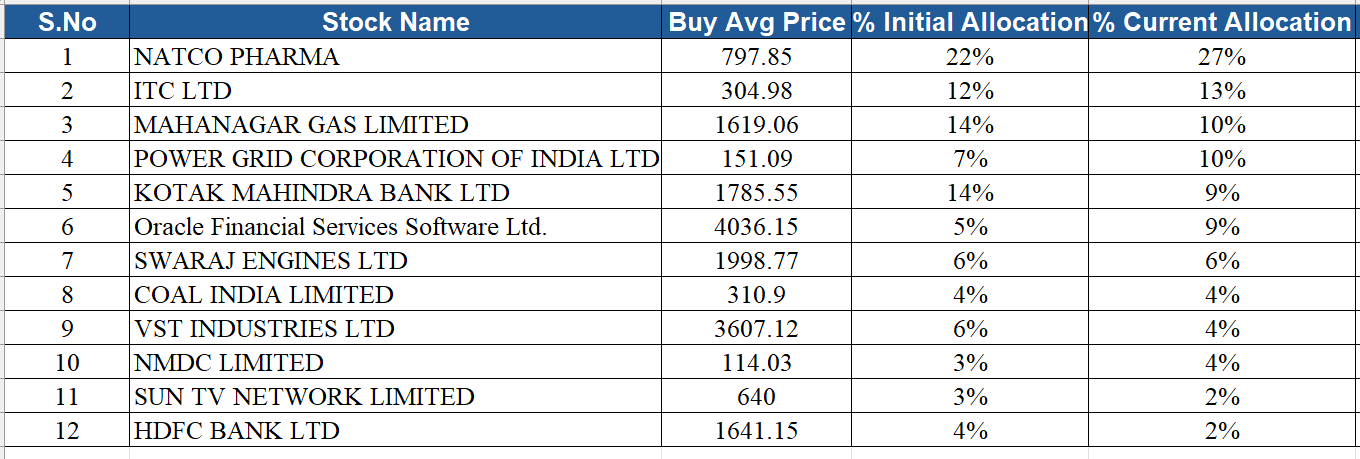

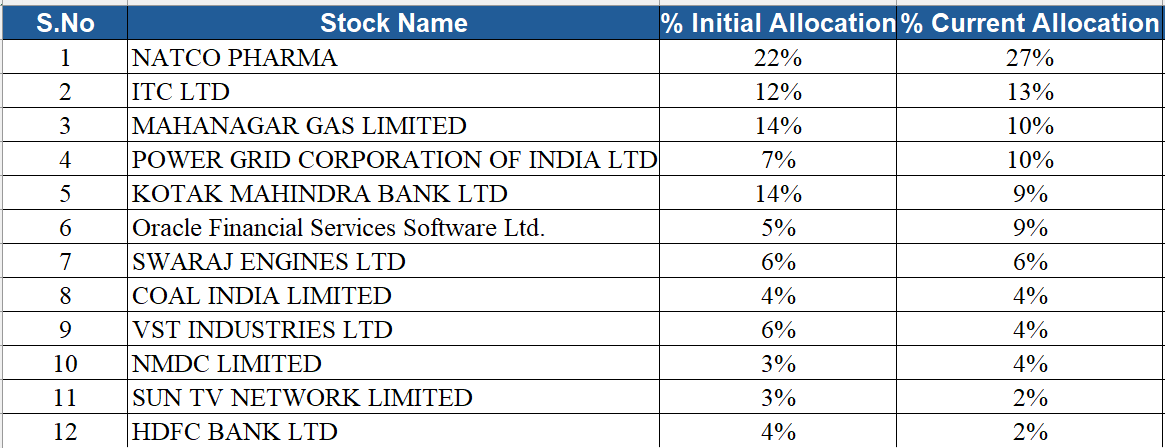

NATCO is the biggest holding in my portfolio: when i started accumulating this stock, The operating profit margins (OPM) contracted to 13.5% in FY2022 from 29.5% in FY2021, primarily due to write-downof large Covid-19 inventory and provisioning of credit losses amounting to Rs. 282 crore. Adjusting for the write offs, the OPM remained healthy at 28.0% in FY2022.

I thought this was an One-Time write off and accumlated it.

Please feel free to share your views on my holdings, as an amateur investor i’m open for constructive feedbacks.

Welcome to VP.Please refer to the other portfolio threads and check how can you make your better. You need to mention thesis, %of your holding and buy average( If possible).

H Vishagan,

You are currently in your early 30s or are you chasing financial freedom in early 30s, with this portfolio …

As an investor, understanding sectoral tailwinds and headwinds is very important and can be a determinant of pf returns. Currently renewables, recycling, agri, Oil & gas to some extent (and also healthcare) are sectors which seem to be having tailwinds - so ideally one must analyse these sectors and find companies doing well

Thanks for checking, i’m currently in early 30’s. This is my direct portfolio investments, which is just around 15% of my overall networth. So this is my passion to invest in direct stocks.

Yes, like you rightly pointed out about the sectoral tailwinds & headwinds. I have trimmed my positions by booking profits recently on NMDC, COAL India, NATCO, POWER GRID, ORACLE. not all booking on same day or month over the months.

so basically i do monthly SIP’s on stocks.

Currently accumulating HDFC Bank, Kotak Bank & Mahanagar Gas.

I decided to exit my holdings in Oracle financial services today.

Even though I initially started accumulating this stock for an attractive dividend yield & knowing the company has its competitive advantage.

But now the PE has short up from approx. 10 PE to 40 PE within short span of my purchase, couldn’t accumulate much when it was available at 10 PE and not sure the rating will be maintained for the long run, that’s my limitation.

During the unexpected times like war conflicts, the nifty 50 has a drawdown of 12% approx. from its ATH. I wanted to check the drawdown for my direct portfolio, basic draw down formula may work out for a static portfolio.

Hence spent some time to check the TWR (Time Weighted Return) portfolio draw down for Q4FY26, ensuring the cash inflow & outflow is considered in the calc.

here is the portfolio drawdown numbers vs nifty 50

All these years, the amount of time invested in reading the investing books have always been a strong foundation to navigate through the volatile scenarios. People like me who started the fundamental based investing during covid, would have seen only the upside potential of the market.

Trust me, when the market was ATH 18 months ago. I believe I was reading these book “Mastering the Market Cycle” & followed “The Most Important thing” both are authored by Howard Marks. The books always made me grounded in picking the stocks and ensured that I don’t get lured in to the quick profits due to the bottom made by COVID crash.

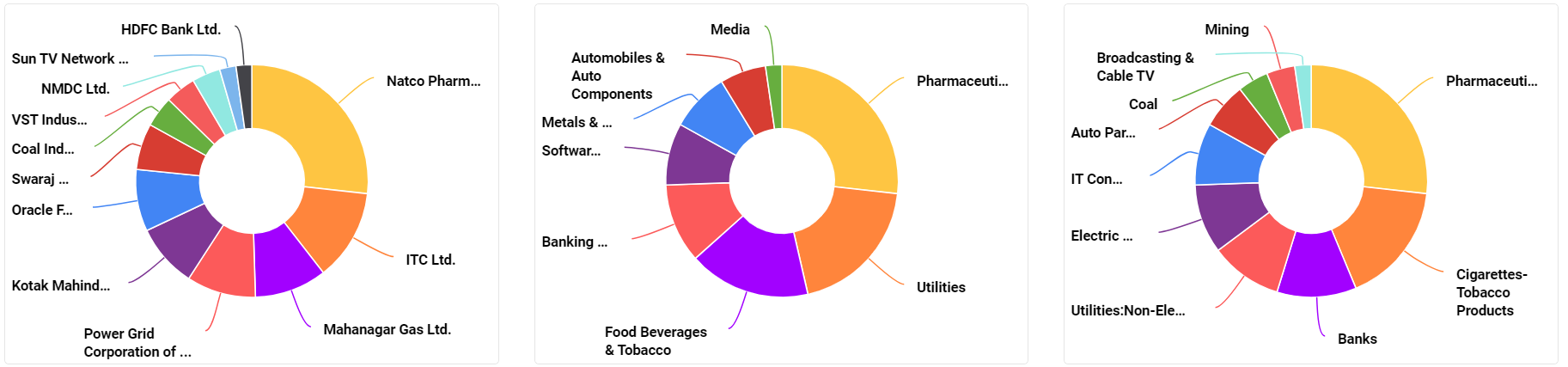

Currently, the portfolio stocks I’m holding have changed but not complete revamp. Sold couple of stocks that gave decent profits & some stock I felt the fundamental reasoning is not convincing to hold for longer duration.

#

Company

ISIN

TTM P/E

TTM P/B

10-Yr Avg P/E

vs. Avg

Notes

1

Mahanagar Gas

INE002S01010

~10.9x

~1.7x

~15.6x

−30% below

Undervalued — Trading well below its 10-yr mean P/E of 15.6x and median of 14.4x; P/B of 1.7x is also below historical avg of 2.35x; earnings pressure from CNG competition & volume softness

2

Coal India

INE522F01014

~8.4–9.3x

~2.8x

~10.2x

−10% below

Fair/Mildly Undervalued — Current P/E is near the 10-yr median of 7.1–7.5x but below the mean of 10.2x; P/B of 2.8x is slightly above historical avg of 2.5x; high dividend yield (6%) supports value

3

TCS

INE467B01029

~18.1–19.4x

~8.8–9.7x

~26.4x

−31% below

Undervalued — TTM P/E of ~18–19x is sharply below the 10-yr avg of 26.4x and 5-yr avg of 28.5x; P/B of ~8.8x vs. historical norm of 13x+; global IT slowdown and revenue miss driving the de-rating

4

Kotak Mahindra Bank

INE237A01036

~19.0x

~2.1x

~29.1x

−35% below

Undervalued — P/E at ~19x vs. 10-yr avg of ~29x is a significant discount; P/B of 2.1x is well below historical norms; leadership transition concerns partly responsible for the discount

5

VST Industries

INE710A01016

~15.7–16.1x

~3.6x

~18.8x

−16% below

Mildly Undervalued — Current P/E below the 10-yr mean of 18.75x and median of 16.8x; P/B of 3.6x vs. historical avg of 4.4–4.8x; cigarette volume pressure and ESG concerns weigh on sentiment

6

Manappuram Finance

INE522D01027

~52–54x

~1.7–1.8x

~9.5x

+450%+ above

Distorted / Overvalued on P/E — High P/E is due to EPS collapse (not price re-rating); P/B of 1.7x is still modest; monitor Q4FY26 — if earnings normalize, P/E reverts sharply; RBI regulatory headwinds on MFI subsidiary remain a risk

7

Power Grid

INE752E01010

~16.8–18.9x

~2.8–3.1x

~12.5x*

+35–50% above

Overvalued vs. history — Current P/E of ~17–19x is above the 13-yr median of ~10.4x; however, this re-rating reflects faster earnings growth (EPS CAGR ~13.5%) and capex-driven value; P/B has expanded from 1.6x (2021) to ~2.9x (2025)

8

HDFC Bank

INE040A01034

~17.2x

~2.2x

~22.4x

−23% below

Undervalued — P/E well below the 10-yr avg; P/B of 2.2x is at multi-year lows vs. historical median of ~3.1x; post-merger NIM compression is resolving, making this an attractive long-term entry

9

Swaraj Engines

INE277A01016

~22.6–23.6x

~10.2x

~21.0x

+7–12% above

Fair/Mildly Overvalued — P/E slightly above the 10-yr mean of 21x; 5-yr avg is 18.9x; P/B of ~10.2x is elevated but reflects the asset-light, high-ROE nature of the business; FY25 peak P/E of 28.5x shows market exuberance has partially corrected

10

ITC

INE154A01025

~18.4–18.6x

~5.4x

~22.5x

−17% below

Undervalued — TTM P/E of ~18.6x below 10-yr mean of 22.5x and 13-yr median of 23.3x; P/B of 5.4x vs. historical avg of 6.2–7x; near 10-yr P/E low; FMCG diversification drag, but dividend yield of ~4.9% provides cushion

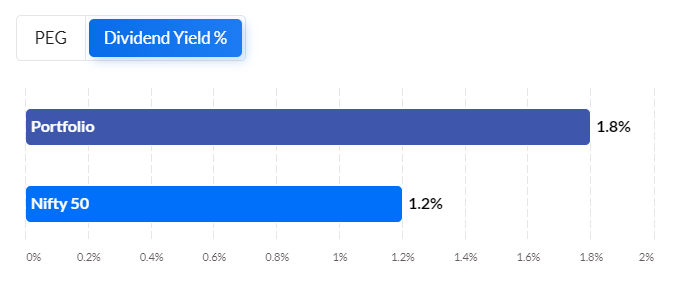

Notes: the valuations of my holding stocks are my assumptions based on my understanding about the individual companies.

Over the last 18 months, people say it is time correction or the volatility due to war conflicts may affect the earnings growth as well as a draw down in the corporate earnings as well. But then i have been a buyer on some of my holdings.

What is your stance on the current situation? do you use the portfolio drawdown to accumulate more or buy some of the new stocks of your Wishlist?