Visaka use to trade at 7 to 9 PE but now is at 80. Financials/Operating margins is not great…

just trying to figure out if i am missing something

I think rooftop solar play

Thanks Narayans…yes it seems company trying to change the product mix and move into value chain by replacing cement aesbestus product to green play…

I am unable to find the Q2FY24 earnings call recording or transcript.

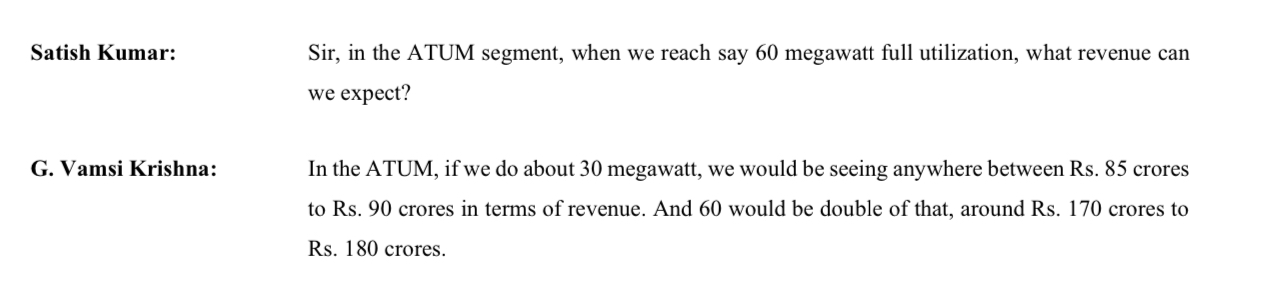

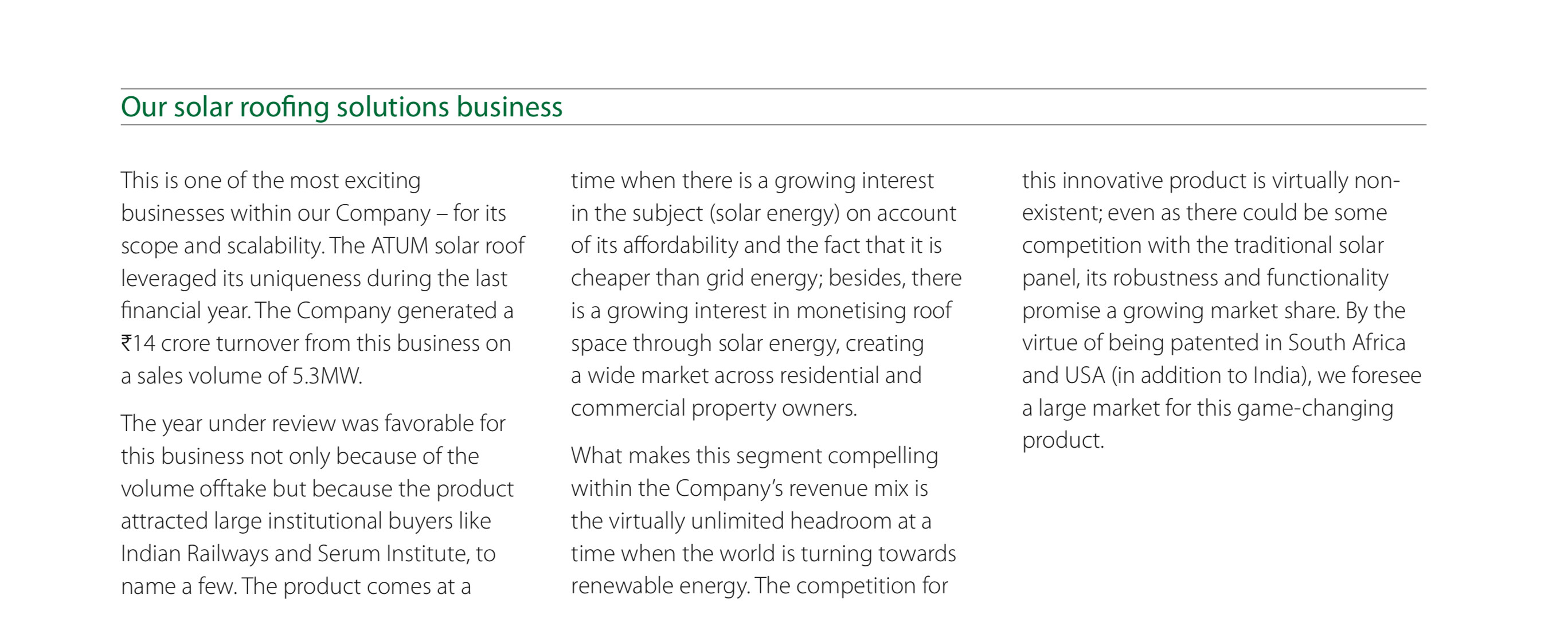

Does anyone know what the contribution of their Atum Solar Roofing business is? Their PPT doesn’t share any figures for it.

Q1FY24 on the call management guided for doubling revenue in 5-7 years and also guided for 25% annual growth, which are contradictory. Was unable to understand.

Also they stated quite low projections for Atum - strange.

They seem to be players 1-2 in each segment, basis their PPT. And all the segments are tied in to the India growth story, with roofing sheets, solar, solar roofing, solar EV charging station, and Vnext boards —- however, for some reason I am unable to notice exponential growth in their numbers.

Can someone study their financials and guide?

Found this. Unsure of publication date.

2 Likes

If you look at the outlook article on the top right hand corner it says OUTLOOK BUSINESS INITIATIVE which means its a paid article. The tone of the article is all glowing and positive about the joint md. It’s a profile building activity for him.

Just my two cents

8 Likes

Fair. Although, most PR is paid these days.

Nevertheless, the segments they are in should ideally be on a hyper-growth trajectory, given the intense infra & capex, growth in housing, focus on solar, and EVs. Yet, for some reason this doesn’t seem to be reflecting in their numbers, not yet at least. But they also claim to be 1-2 in their segments, so is it that the need for their product hasn’t kicked in as we’re early in the cycle?

This one is perplexing me at the moment.

Recent price movements and ATH volumes indicate something is brewing.

Let’s wait for quarterly results.

Just a quick read through the article and you note that the patent is for the packaging of the solar cell into a durable and weather resistant panel.

In solar roofing the more valuable patent is about the energy efficiency and the electricity generated. This patent is useful but not disruptive.

That said visaka has been in building roofing products from asbestos for a long time. They have a history of unrelated diversifications like a textile plant etc if you go far back enough.

That said, joint md seems to be next gen and maybe a generation chang e will be good like it has been in companies like borosil group.

Disc: not tracking not following not invested.

1 Like

Looking forward to results on Monday.

Have loaded heavily across the past 3 days and created a very big position.

This one is purely basis technical analysis of lifetime high volumes, two massive candles wiping out the history, non participation in the broader solar-theme move, timing of price action, potential of the solar rooftop product, potential of the building material products considering the infra theme, and participation of a few astute investors.

Not won over by recent numbers, but my gut says there is something brewing here and we may get more clarity on Monday.

Sticking my neck out with this post, and still dreaming.

I have read somewhere that the ATUM roofs constitute less than 2% of the company’s revenues. So the play is on the future growth potential as currently the contribution is minimal.

Disc: Invested

I suspect the contribution has been negligible. I also suspect there will be some very positive news & declarations by them on Monday.

I have a feeling they may have secured some government orders, namely from the army.

Created a 6% position. Measured risk. Dreaming.

@Moonrise whats your take on Q3 results?

Of course, results are not good. However, the clear technical breakout and stupendous volume buildup, the historic wipeout with two tall bars, leave me asking for more, more information, that is. The results - and - move, are on two extremes and can leave one perplexed.

I will study the line item breakdown this weekend. On quick glance I saw building materials increase but zero mention of the solar business (why!!??). I wish we had an investor presentation and management call, both of which seem to be missing.

We also have a Multi year Darvas box, looking to be broken.

Why would a big name buy 8lac shares a day before results?

Why is there no indication and guidance on the solar roofing vertical - which is the flavor of the (next 3-5?) year(s)?

Would be great if someone could do some scuttlebutt.

1 Like

Why shouldn’t they benefit from this and why are they not talking about this.

Who bought and please share the source @Moonrise

Have shared in the earlier post.

ABOUT ATUMOBILE

“Straight outta Hyderabad, we’re a company that focuses on e-mobility and strives to make green riding the present and the future. Atumobile is the genius brainchild of Vamsi Gaddam, our fine young Founder - a passionate innovator with a mission to bring green mobility to the forefront of the Indian automobile industry. Atumobile merged style with sustainability paving way for India to welcome its 1st ever cafe racer style electric bike and its two variants - the Atum 1.0 and the Atum Vader.“

Not sure of commercial availability, if it already is or when it will be.

Mystery deepens. Wonder why the company doesn’t communicate more openly.

Is anyone still tracking the company ?

Is this can be a beneficiary of PM suryoday yojana? Company has good unique patented brand in solar space.

Visaka Industries has achieved a milestone. - becoming the only company in the country to offer

integrated solar roof solution that is certified under the Approved List of Models and Manufacturers

(ALMM) by the Ministry of New and Renewable Energy (MNRE).

Visaka.pdf (332.7 KB)

2 Likes