Have you also considered epack durable in your analysis?

1 Like

the whole EMS space should do well. Voepl looked favourable vs others quoting above 100 PE

E pack sadly has a poor Q2 earnings wise. Top down the whole sector has been a great wealth creator. Most players are 150-200 + multiples. So Voepl and others below 100 PE look much favourable to me. But thats just my opinion. U can model the business via guidance. I assume e pack would have also given a good guidance.

60% of the stock Px appreciation is coz the sector does well. And stocks move in tandem to each other. So any pick should do.

3 Likes

Freezer space - refrigeration growth engine can sustain after this and could command a better valuation multiple

3 Likes

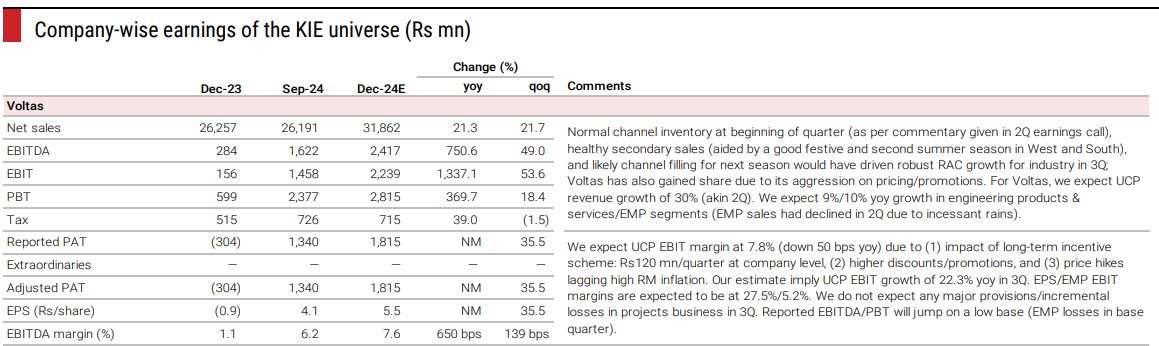

- Voltas channel inventoy is healthy

Sounds right for VOEPL too. Good summer season which got elongated plus recent annoucements to diversify a bit into refrigeration

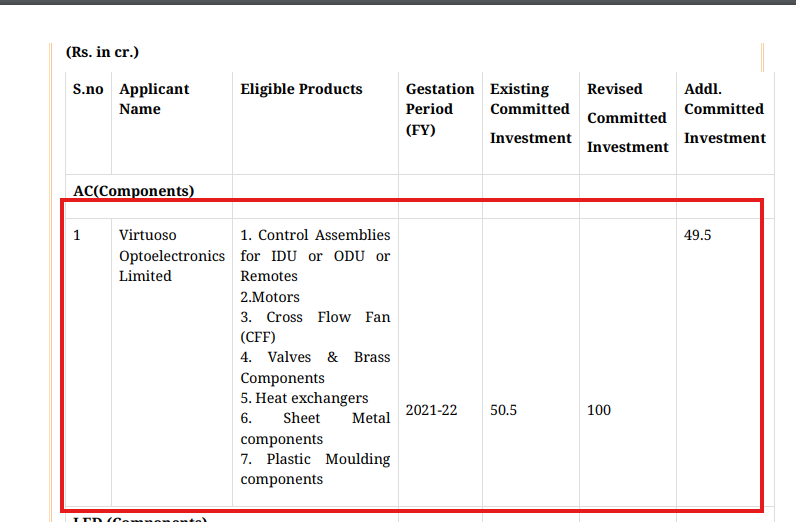

Virtuoso ( Chota PGEL) - Additional PLI

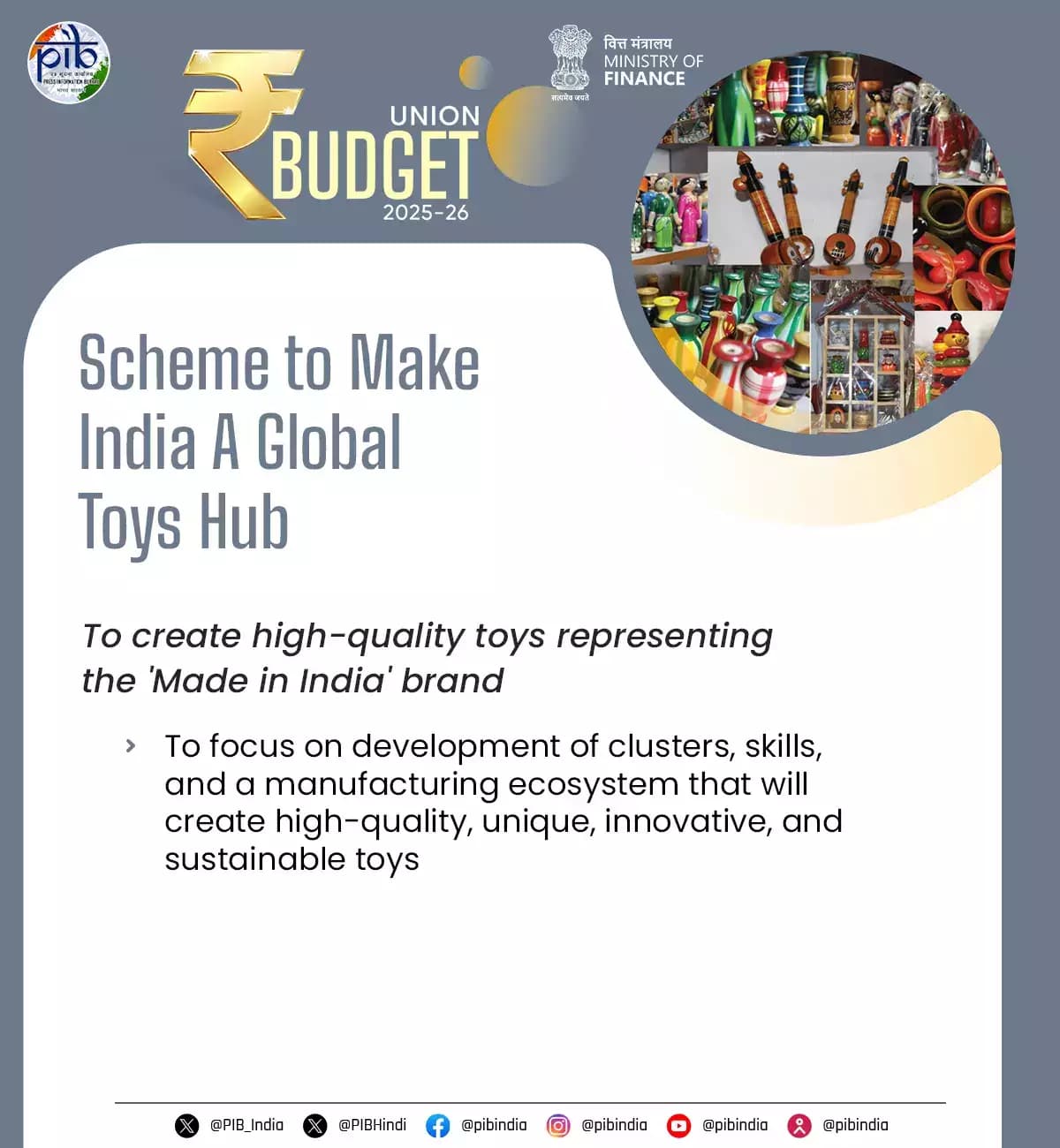

Budget does mention around Toy Sector - Lot of measures announced to make India a hub of Toy manufacturing

As per Virtuoso concall they also do revenues from Toys

Budget - PLI - EMS

6 Likes

Virtuoso Optoelectronics Q3 ; Co. says Company is on track to achieve the projected revenue of Rs ~700 Cr in FY25 and is looking forward to a growth of 45-55% YoY in the coming financial year, with the help of increased capacities.

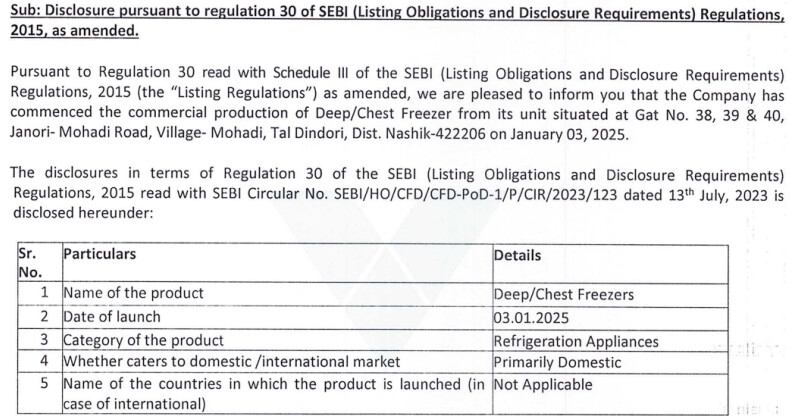

The company has successfully begun commercial operations of its Commercial Refrigeration (starting with Chest/Deep Freezer) manufacturing facility at Nasik, this unit has an annual capacity of 1.5 lac units and this will be ramped up to 4 lac units in the next FY.

The company has successfully begun commercial operations of its component manufacturing unit at Chennai that will be run under its wholly owned subsidiary Virtuoso Polymers Private Limited (VPPL), this unit has capacity of 4000 sets per day

6 Likes

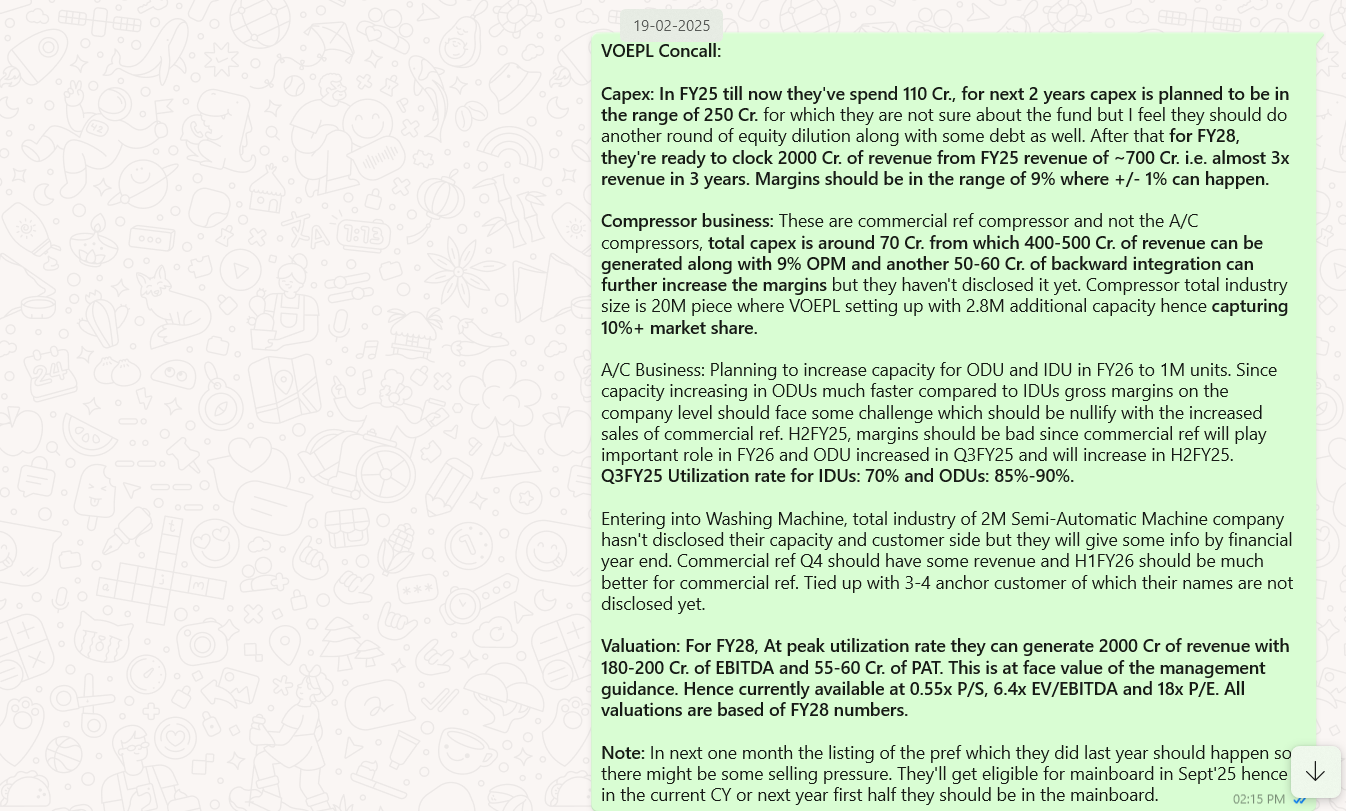

19th feb Meeting with MGMT Highlights:

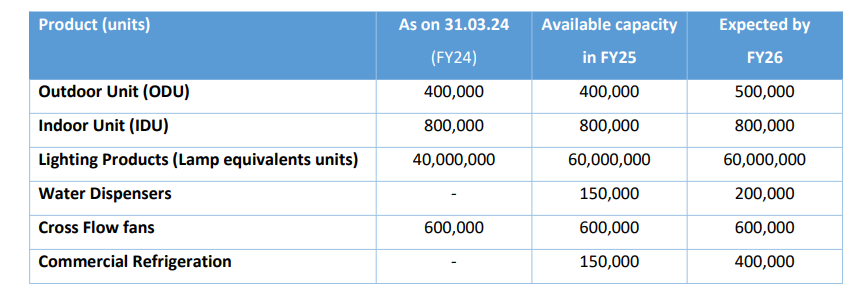

Capacity Expansion and Product Development

Compressor Segment

-

VOEPL has partnered with two Chinese compressor manufacturers, Huayi and Jiaxipera, with a total capacity of 70-75 million units per annum for reciprocating compressors.

-

Two types of compressors exist:

- Rotary compressors : Used for air conditioning.

- Reciprocating compressors : Used for refrigeration (both commercial and domestic).

-

Machinery for compressor production is expected to arrive by the end of March, with production commencement planned in the first two quarters following setup.

-

A semi-automatic washing machine production line is being established, expected to be operational by Q3 FY26.

-

The air conditioning (AC) segment is currently facing capacity constraints, prompting capital expenditure (capex) to enhance production capabilities. Existing customers will continue to be served.

-

Commercial dispatch of freezers has commenced, with an anchor customer onboard along with several smaller clients.

-

The company plans to introduce 100L freezers and a new glass-top series. Additionally, 600-700L freezers are expected to be launched in the upcoming quarter.

Virtuoso Polymers Expansion

- Operations have commenced in Chennai, with production beginning from Unit 1.

- Unit 2 is planned, with commercial production expected by Q3 FY26.

Financial Projections and Revenue Guidance

- The company aims for a topline of ₹2,000 crore by FY27, comprising a mix of all product segments.

- Refrigeration demand is expected to be strong, though compressors production will have a gestation of a 6-9 months period before contributing significantly.

- The company plans to renew its ₹1,200 crore revenue guidance for FY26, assuming 60-70% capacity utilization, which is considered a reasonable estimate. FY25 Revenue guidance remains at 700 Crore.

- Compressors alone are expected to generate ₹400-₹500 crore in revenue, with an estimated 9% margin.

Margins and Profitability

- EBITDA margins: 9% ± 1%.

- PAT margins: 2-3%.

- Newer segments, such as commercial refrigeration, are expected to yield higher margins:

- Commercial refrigeration: 10%

- Compressors: 8-10%

- Given that AC and refrigeration compressors share similar supply chains, the company expects operational efficiencies.

Capital Expenditure Plans

- FY25 Capex: ₹110 crore.

- Projected FY26 Capex: ₹110 crore.

- Total Capex for FY26-27: ₹250 crore.

- The company will prioritize debt financing for capex requirements.

- Phase 1: Compressor capacity expansion (₹70 crore investment for 2.8 million units).

- Phase 2 & 3: Backward integration (₹50-60 crore additional investment for sub-assemblies from China).

PLI Incentives

- Production Linked Incentives (PLI) benefits will commence from next year, contributing an additional ₹20 crore in FY26 and FY27.

Industry

- The overall AC market size is 12 million units, while the refrigeration compressor market stands at 20 million units.

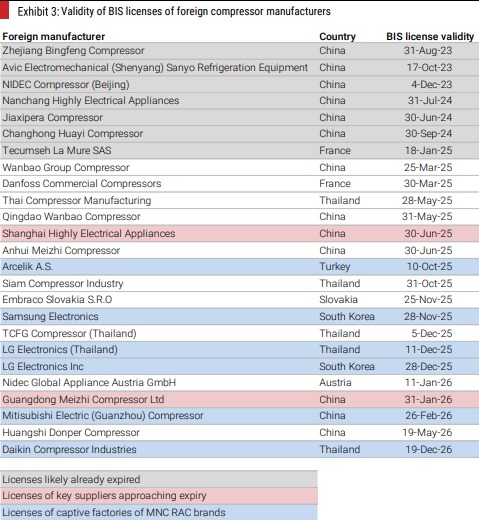

- The expiry of BIS certifications in China for reciprocating compressors (January 2026) is expected to create a supply gap in the Indian market.

- Out of four BIS licenses, three will lapse in June 2025, and the last one in January 2026, potentially leading to a 15 million unit shortfall in the Indian market.

- This anticipated shortage is likely to drive stockpiling of compressors in Q4 FY26 and Q1 FY27, with the company expecting full booking of its production capacity.

- The Indian market currently produces 4-5 million compressors (by Godrej and others), while the remaining demand is met through imports and smaller manufacturers. There exists a gap to be filled by a properly organised company like VOEPL.

- Compressors are priced between ₹1,500-₹1,800 per unit.

- Current refrigerator compressor capacity is 2.8 million units, with plans to double this to 5.6 million units by the beginning of FY27.

- The company aims to match or slightly undercut Chinese pricing (3-5% lower).

- In commercial refrigeration, all clients are new, with significant brands in the pipeline.

- Only 2-3 major brands (such as Blue Star, Voltas) have in-house compressor production capacity, while others rely on imports and smaller manufacturers.

Washing Machine Segment Strategy

- The semi-automatic washing machine market in India sees annual sales of 2-2.5 million units.

- Most manufacturing is concentrated in North India, while VOEPL aims to serve the West and South markets.

- Regionality plays a critical role in washing machine production because of high transport costs.

Utilization Rates and Seasonal Trends

- Indoor Unit (IDU) utilization: 75%.

- Outdoor Unit (ODU) utilization: 100%.

- Q3FY25 performance expectations: Typically lower margins due to an increased ODU share; however, new additions are expected to compensate for this.

- Washing machines perform well in Q2 and Q3, while AC sales peak in Q3 and Q4.

Corporate Developments and Fundraising

- The company will file for NSE listing post-September 2025.

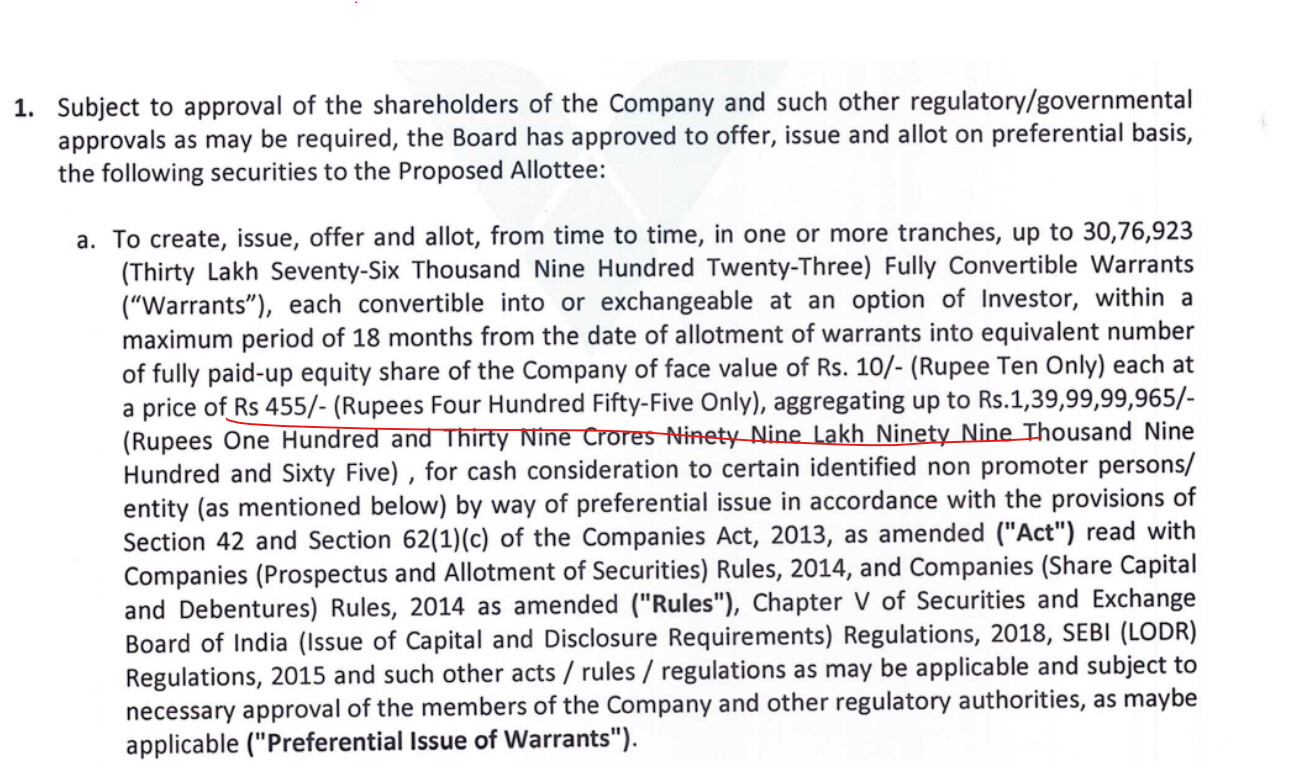

- SEBI approval is pending regarding warrant issue; the latest update from the December 16 meeting suggests progress.

- SMEs with over ₹25 crore of paid up capital can raise funds exceeding under the revised guidelines.

- The company is set to receive ₹60 crore from warrants, adding to ₹40 crore+ in existing funds for future plans.

15 Likes

Hey Sagnik,

I think the 2000cr figure for FY27 was for capacity and not revenue guidance.

With 1200cr FY26 Guidance and 35-40% growth the number should be 1600-1700cr on higher side.

Can you confirm the guidance numbers?

Thanks

1 Like

Hi, the guidance is as follows:

FY25: 700

FY26: 1200 (mgmt says that this figure will be revised upwards soon)

FY27: 2000

figures in INR Cr.

7 Likes

Hi, I am not able to find the recording of the 19th Feb, 2025 investor meeting that happened.

Can you share the same here if it available with you

1 Like

Hi, the meeting was private. No recording available

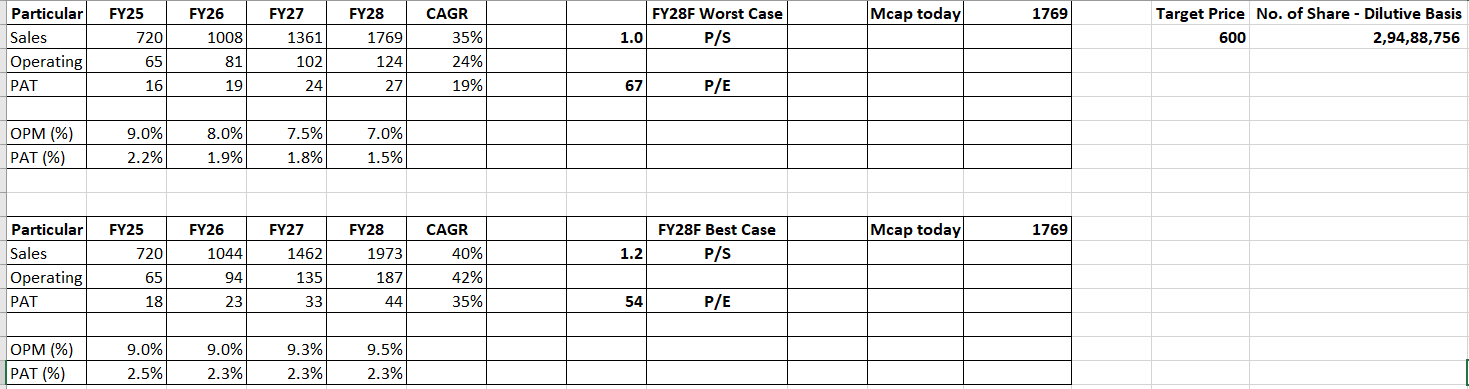

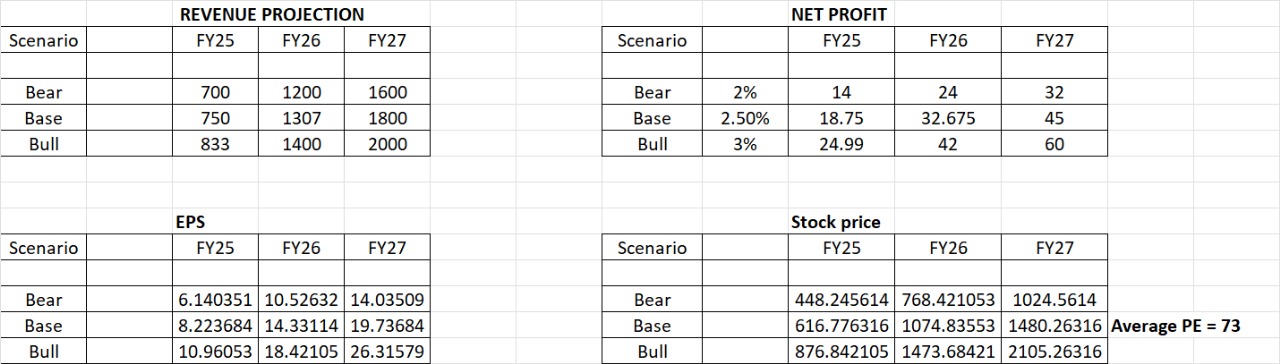

But here we’ll have to consider at least 2 rounds of dilution along with dilution in PAT margins as well. I expect PAT margins to be in the range of 1.5%-1.75%, and EPS growth will be lower. Sharing my forward calculation, which I think will help you understand better.

If you get exit at 600, even if we don’t consider any dilution from here onwards which is impossible, Stock is available at ~50x P/E best case scenario.

1 Like

As per the management meeting held on 19th February, key highlights include EBITDA margin guidance of 9% ± 1% and PAT margins in the range of 2–3%. Newer product segments such as commercial refrigeration and compressors are expected to yield higher margins—10% and 8–10%, respectively.

The company has laid out a clear capital expenditure roadmap, with ₹110 crore allocated for FY25, another ₹110 crore projected for FY26, and a total capex of ₹250 crore for FY26–27, primarily funded through debt so they are not going to Dilute the share. Revenue guidance stands at ₹1,200 crore for FY26 and ₹2,000 crore by FY27. Compressors alone are expected to contribute ₹400–₹500 crore in revenue at approximately 9% margin.

Product diversification into semi-automatic washing machines, freezers, toys, and ACs is helping the company transition from a cyclical business to a more stable, low-cyclicality consumer durable model. With washing machines peaking in Q2–Q3 and ACs in Q3–Q4, the business is increasingly well-balanced across quarters.

Given this strategic shift toward higher-margin segments and the company’s clear growth roadmap, the FY27 revenue target with a 3% net margin appears highly achievable, subject to execution. From this perspective, the stock currently appears significantly undervalued.

Also sharing the Bull base Bare scenario of the stock from the above assumptions

Note - I am Not a SEBI Registered advisor this is just for a study purpose share your Thoughts

- Both IDU and ODU capacity are expected to reach 1M by FY27, ODU have lower gross margins but value growth will be there and in terms of margins, Water Dispensers and Commercial Ref will offset lower margin done by ODUs. Hence, blended basis OPM should be 8%-9%.

- If they’re doing 2000 Cr. by FY28 then company is expected to grow at 35%+ CAGR and their ROEs are much lower hence, external funding is required, now given they’re already at 2x Debt/EBIDTA, in FY26 end or FY27 dilution is coming.

- You have not considered pref shares which will be available for trading in next few months, probably hence at 60 CR. PAT, EPS should be 20.35 and not 26.31579.

- They’ve guided 2000 Cr. sales by FY28, not by FY27.

- Other points you’ve correctly mentioned about Compressors which will be for captive and commercial purpose both and if they do another round of backward integration which is ~40 Cr. - 50 Cr. capex, more than 9% OPM can also gets generated from there. While putting all these into consideration, I’ll be shocked if they’re doing more than 2.7% PAT.

- Management is really strong and has built a solid business but it’s not undervalued in my opinion.

Disclosure: Invested.

2 Likes

-

In your post, you have referenced the business update shared by the company in February. However, they doesn’t disclosed for their washing machine segment in that business update which may be shared lately.

-

As per the management meeting held on February 19th, the ₹2,000 crore revenue guidance is for FY27, not FY28 as mentioned in your note. This is a significant error and needs to be corrected. Currently, the company has guided for ₹1,200 crore in FY26, and the management has indicated that this number is likely to be revised upward soon, so you may consider adjusting your assumptions accordingly.

-

The company has already achieved a 3% net profit margin and is now focused on maintaining it, rather than reaching it. There is also a high probability of expanding this to 4% as they shift towards higher-margin products. The September quarter results, which were among the weakest, reflected an unfavorable product mix (notably higher ODU contribution), as explained by the management in the concall. However, the company is now focusing more on compressors, refrigerators, and washing machines, which command 9–11% margins. Therefore, achieving and sustaining higher margins appears well within reach.

-

While it’s true that preference shares were not considered in my earlier calculation—a valid point—you also did not factor in the benefits from the PLI scheme, where the company is eligible to receive ₹20 crore each in FY26 and FY27. This support, coupled with a manageable debt level (currently at 2x Debt/EBITDA), should ease financing needs. Additionally, the company has guided a requirement of ₹70 crore in H1FY26, which seems manageable. With expected repo rate cuts, the effective interest rate is likely to be lower than before.

-

Despite the equity dilution, the company is projected to maintain a 3–4% PAT margin, supported by a favorable product mix and a strong management track record. An EPS of ₹26.3 appears achievable under these conditions. Even assuming a conservative EPS of ₹20, applying the company’s median PE of 73 results in a fair value of ₹1,460—more than 1.5x the current level. Thus, even under your more conservative assumptions, a forward PE of 50 implies a reasonable 1.5x return, given that both the growth trajectory and management execution remain intact.

So you doesn’t want to be shocked if they’re doing more than 2.7% PAT as you doesn’t Included the PLI Benefits may be Deprecation will be a factor but 3% PAT is already achieved it is a matter of time whether they are doing for 4% PAT growth.

Market is always forward Looking so PE = Perception upon Earnings.

Thanks for the Reply Good Conv

Disclosure: Invested.

5 Likes

- I was in the call you’re referring to sharing the notes for the same, Now if you adjust the depreciation method to earlier level, this result was lowest in terms of gross margins, EBITDA and PAT as well, now given they have weak H1, H2 will be better but if you look at pro forma basis on a yearly basis it should be on the lower end which was my primary concern and when i asked, management indicated that this will be the new normal although water dispenser and commercial ref will take care from H2 onwards but real benefit will come in H1FY26. So as per my understanding 2000 Cr. guidance is for FY28 but maybe I’ll have to confirm that in this concall.

- If 4% PAT is there then stock is suppose to re-rate from here due to as you said Change in Perception. Commercial ref earlier management indicated 12%-15% range which has now come to 10%-12% range and on a blended basis they said they’ll maintain 9% range.

- Yes, you’re correct PLI benefit will come but even after that dilution is on the books. At least my numbers are telling me that. Washing machine business plan they should disclose in this concall let’s see !! Hoping for good guidance from that segment.

Thank you to you too.. Good discussion on a Sunday evening.. haha

4 Likes

Hi can any one confirm the revenue guidance which have been gave at 19 th feb meeting once again

1 Like

CM Devendra Fadnavis presided over the signing and exchange, witnessed by delegates from Virtuoso Optoelectronics Pvt. Ltd.

CMOMaharashtra

MoU 4 Strengthening Maharashtra’s Electronics Manufacturing! Signed between:

The Government of Maharashtra and Virtuoso Optoelectronics Pvt. Ltd. Objective:

- To invest ₹800 Cr at Dindori, Nashik for: Electronics, Controllers, Motors for Compressors, AC and Washing Machines.

- 500 employment opportunities (Direct & Indirect)

6 Likes