Brief introduction about the company

Incorporated in 2015, Virtuoso Optoelectronics Limited manufactures consumer durable goods, assembles a wide array of products, and provides end-to-end product solutions. The company’s current product portfolio of consumer goods includes (1) Split Air Conditioners; (2) Water Heaters; (3) LED Lighting products; (4) cross flow fans; (5) other miscellaneous products such as injection molding components for air conditioners.

In a nutshell it’s a simple plain vanilla small EMS player.

About the promotor : In his own words “Experienced Individual with a demonstrated history of working in the electrical and electronic manufacturing industry. Skilled in AutoCAD, Negotiation, Business Planning, Analytical Skills, and Operations Management. Strong business development professional with a Master of Science (MSc) focused in Engineering Technology from Birla Institute of Technology and Science. “

His previous stint: Worked as a director for Solarcopyer Limited. Not sure if it was a paper company or solar related product manufacturing company.

Promotor is 1st generation entrepreneur and very young.

https://www.linkedin.com/in/sukritbharati/?originalSubdomain=in

Let’s talk business:

-

Virtuoso Optoelectronics Pvt. Ltd office and facility located in Nasik (Maharashtra).

-

VOL has started as small EMS player for local (unorganized) companies. Like any other EMS player they have got head start with LED’s ( commodity) that gave them around 70cr topline company in a 3-year span.

-

In LED’s, the company is offering both ODM and OEM. It designs and manufactures the product and offers to the customer.

-

Problems with LED’s business: Orders were very erratic, customer retention rate is very low, to many players with way too much competitive pricing, growth visibility in terms of repeat orders is not there, no loyalty b/n brand owner and EMS player.

-

Above are the problems that the company had faced and hence they diversified the product offerings to where there will be some kind of stickiness and dependence as well as some kind of specialty (not a very hyper competitive market like LED’s) that made them to open new product line called Split Air Conditioners both Indoor and Outdoor.

-

Localization of Indoor AC’s was a recent phenomenon ( just 6years old) there is lot of demand at this time for local players who can manufacture some components (may be all) and provide services. (Demand and supply gap is there)

-

Whereas Outdoor AC’s boom was happened some what around 12 years back and that’s how Amber was born, and market is matured now.

-

VOL started IDU AC’s in 2018, just assembling from 300 AC’s a day to manufacturing 3000 AC’s a day with complete backward integration in plastic injection molding, sheet metal forming, manufacturing heat exchangers and coper tubing, powder coating, wire and harness manufacturing and fans.

-

Quite a journey in short span from pure assembling to a complete end to end solution provider including product design as well. Which is what made them somewhat competitive and differentiated form lot others.

-

In AC’s segment the company is currently transitioning into ODM as well (still very small product design offerings, not a complete product provider).

-

Electronic manufacturing business mainly happens in two ways one is you showcase your capabilities (Initial capital is very high and don’t know capacity utilization) and get the orders from different brands and no fixed contract for recurring topline, and second one is you develop a relation with a brand and be a trusted partner (Like how Mold-Tek Packaging Ltd is to Asian paints is !) and start encroach into other products verticals which the brand offers. (don’t have to create upfront capacity and look for utilization!).

-

Advantages for being the second type model are recurring revenue, customization of product lines, a bit of future revenue estimation, better asset turnovers, no extra overhead costs, no inventory storage, no seasonality effect, you plan your capacities and WC requirements in accordance with the order visibility and you set up new product verticals based on offerings of the brand. Of course, there is no fixed written contract here but more like a “take my word” type and mutual trust. Again, you are not bounded for any one customer, you can offer services to other players as well.

-

Disadvantages are your scope and scale is limited, product customization may not suite for other brands, if brand is not doing well obviously you don’t.

-

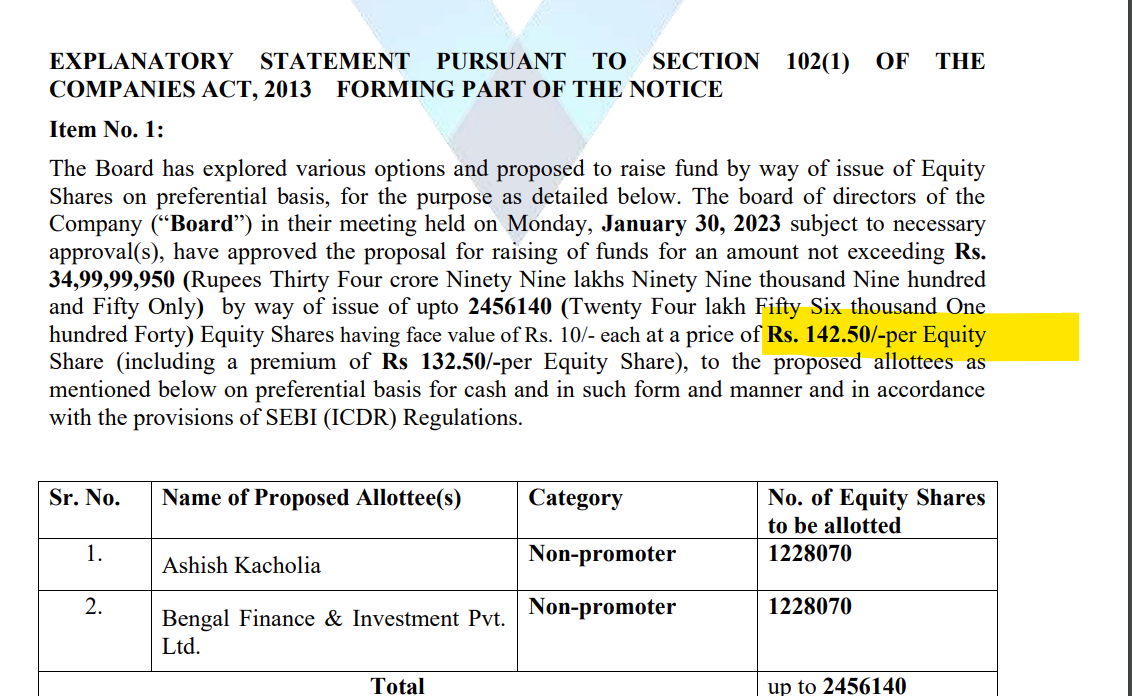

Present growth rates are very high that the internal accruals alone are not sufficient to fund the growth, so company took debt around 70cr (8 to 9% int) in 2022 and did a preferential allotment to Kacholia sir (37cr) in the same year.

-

Did around 200Cr topline and expected to do 330 to 350Cr topline in FY23 (close to current Mcap).

-

AC’s contributing around 75% revenue and 25% LED’s and others.

-

30% raw material is imported from China and 70% locally sourced.

-

70% backward integrated in IDU’s and 40% backward integrated in ODU’s.

-

Hold on!! Backward integrated doesn’t mean it manufactures everything! including the plastic granules also. It buys plastic granules locally and do the plastic molding for IDU’s.

Capacities:

-

First facility LED’s no idea about capacity ( assuming very less)

-

Second facility 6lakh IDU (utilizing at peak levels) adding additional 2lakh capacity next year.

-

Third facility 2.5 lakh ODU (utilization is around 25% this year (started in Dec 2022 and adding additional 2 lakh capacity next year with a target of 75% utilization)

-

Added fourth manufacturing facility for cross flow fans in March 2023 (~45,000)

-

40Cr spent for both third and fourth facilities.

-

Planning to come up with large facility (fifth) for two more new electric appliances, details will be revealed in first Qtr FY24 for existing and new customers (Another 40 Cr will be spending on this facility)

-

Overall capacity utilization is around 50% this year (350 Cr revenue), at full capacity utilization

company can do 700Cr revenue. Targeting around 600 cr for FY 24 and 1000 Cr for FY 25 ( might need small additional funding for this, as current capacity peaks out at 800 Cr)

Margin profile:

-

LED margins ~ 13% , IDU ~ 9%, ODU ~ 7% combined ~ 9%

-

Going forward company is guiding for 9% overall (Including the two-value added new product lines margins ~13%) just 200 bps more than the industry number no MOAT or bargaining power (that’s totally fine as co is not manufacturing rockets!!

)

)

Valuations ![]()

-

At current valuations it’s trading at TPE ~ 48X (335 Cr topline FY23, 8 % margin, interest 11cr, depreciation 7 cr, tax 25%)

-

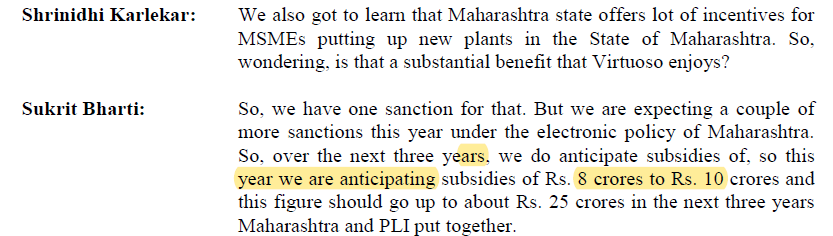

Company has applied for PLI scheme to both central and state (MH) 35 Cr for 5 years (7Cr/year cash back) and 60 Cr for 10 years (6Cr/year) respectively.

-

Also received ~35 Cr for preferential allotment to Mr. kacholia sir.

-

Company may use this money to reduce the debt or increase the capacity depends on business outlook.

-

but looking at the business momentum MD is looking to expand and grow further. So don’t expect total debt reduction any time soon (makes sense 8-9% interest Vs ROE of ~20)

-

Company has long term debt ~40cr against a fixed block ~100Cr

-

Like another EMS player company needs short term debt to meet WC requirements ( 90 days receivables time)

-

Asset turns for FY 23 was ~ 4times will increase to ~5.5 times for FFY24

-

Can’t take a close valuation call this point of time as there are many moving and critical parts ( debt, PLI, new product lines etc) but conservatively I’m thinking a doubler in 2 to 3 years or 3 to 3.5 times in 5 years.

TAM:

Current market share is ~ 5% ( 4lakh AC’s), total production in India currently is ~80 lakh units.

- China is exporting ~80lakhs units every year and a production around 120 lakhs for domestic consumption.

Further Growth:

-

In FY24 company is planning to introduce two more new product verticals (other than AC’s) that might have the same potential as AC’s in terms of topline in the coming three years.

-

Export opportunities

.

Risks:

-

Client concentration, 70% revenue is coming from a single client “VOLTAS” in finished AC’s and in LED’s single major client is Panasonic. ( Not surprised, that’s how any micro cap player grows!!)

-

Make in India theme proves to be a fad !!

-

Promotor failed to walk the talk.

Disclaimer: Invested and biased.