If you do basic checks around cashflows and jugglery with subsidiary, you will understand the story. Subsidiary financials can be obtained from RoC and that will give you full picture. All the best.

Virnchi offering first UPI based credit card.for this they have tie up with RBL Bank and product name is vcard.they are promoting this product online below is the link. Dont understand why IT company diversified to Hospital.

Virinchi has raised 525cr capital through convertible warrants to strategic investors at an issue price of 150. This, when the current market cap is 537cr and CMP is 142.

Management has so far not released any capex plans but my guess is that they might expand the hospital business to outside Hyderabad.

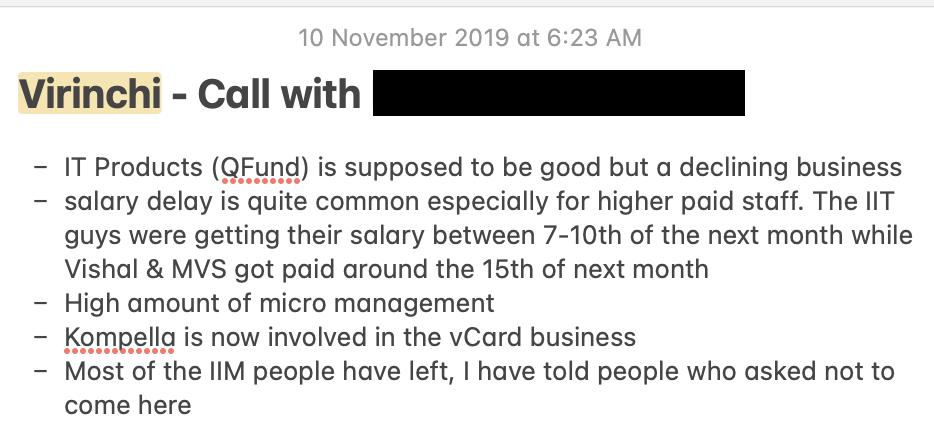

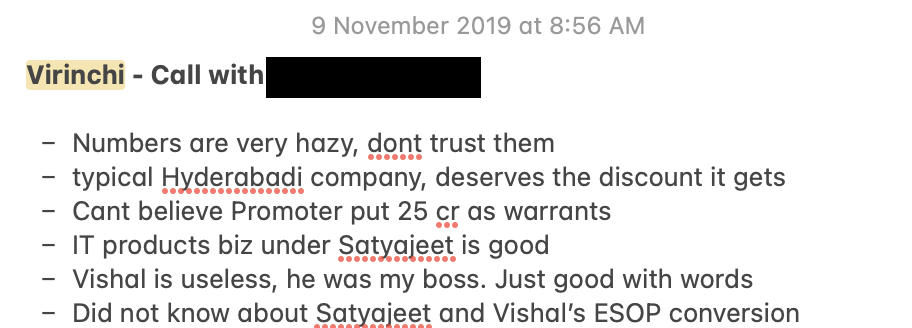

Just noticed Virinchi is on the radar again and want to warn new investors about this stock. As a novice, I’d invested heavily based on the hospitals story and ended up burning my fingers badly. This is an extremely shady/fraudulent company with continuous promoter dilution, dressed up numbers and weak management. I exited at a loss a while back and wouldn’t touch it with a barge pole - sharing some notes from calls I had with their ex employees who are IIM grads - these helped me make up my mind to book my losses.

The recent announcement of 525 cr warrant issuance to unknown entities is exactly what Virinchi and other junk caps did in the 2017 small cap bubble… Spin a story and announce warrants at significant premium to current price, Retail jumps in, money never really comes in, and insiders exit at the top. Look at the equity history of Virinchi and you will see that promoters have issued warrants to themselves every year with no clear use of funds, never bought a single share from the market even when it fell to sub 20 levels, and sold in the market when it suited them.

Re their hospitals business, it has been banned multiple times from treating Covid patients for medical negligence, surplus billing etc.

As a young value investor, I have been examining the company from this thread and its annual reports of past 10 years. Here are my thoughts, along with some corrections:

Red Flags

Mr. Vishal Khandelwal once said, “Annual reports are supposed to be black and white and boring, with no pictures in them. The more colors there are, the more the company wants to fake their report and do more marketing.” Interestingly, the company’s annual reports were very simple until 2016 and had that old black-and-white look. However, starting in 2017, they transformed into marketing ads, featuring almost a picture on every second page. Feel free to correct me.

Just have a look-

this is not what we call an annual report its more like a Television Ad. No relavant info written in the reports

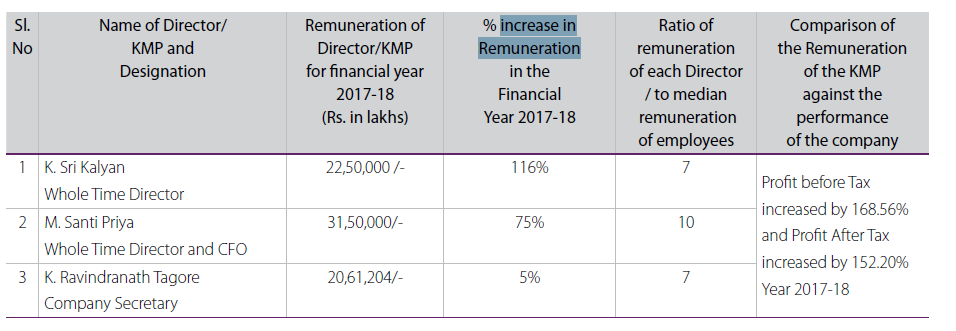

Second red flag i think is the remunerations of the Directors

The company has been mostly making negative free cash flows in the past, but still it is increasing there salaries by 116%

this is from 2020 annual report

see the sudden increase here

They kept increasing it in 2019 too…!

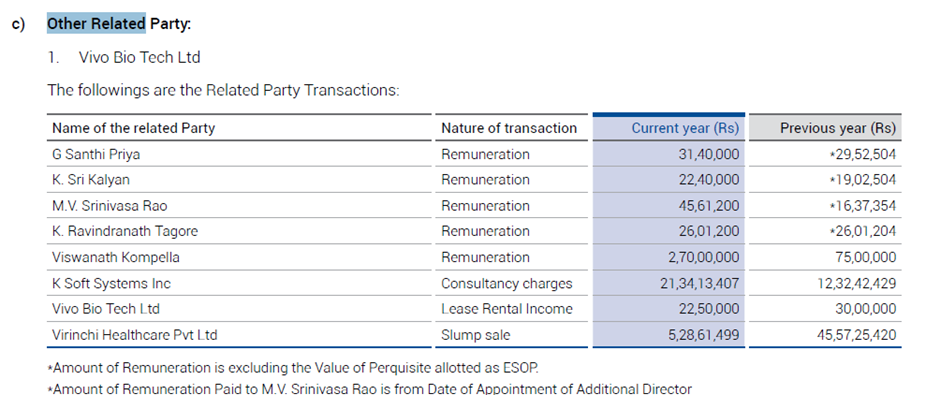

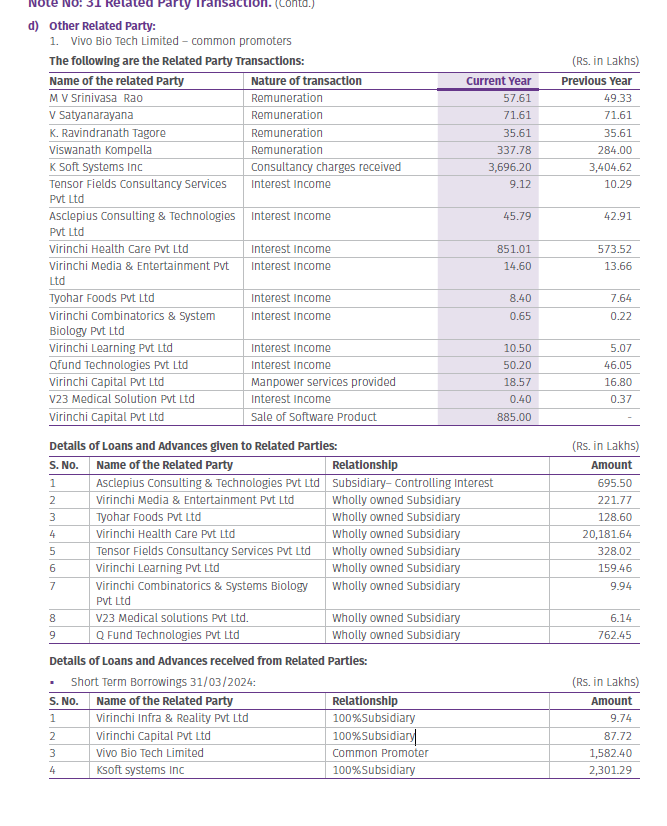

Now comes the most important party “THE RELATRED PARTY TRANSACTIONS”

I usually try to stay away from companies with high number of related party transactions.

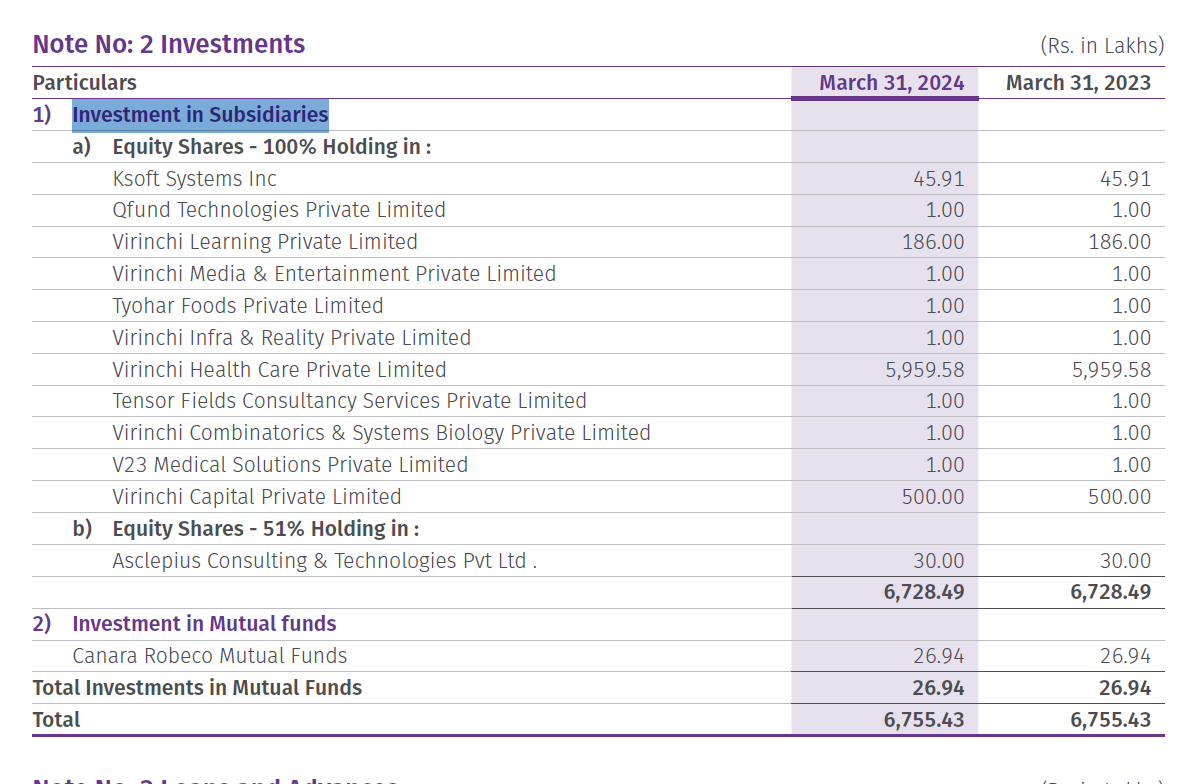

most of there investments ( which came from huge borrowings) are into there own subsidiaries.

also they are paying this huge amount of consultancy fees to there own subsidiary (called as K Soft systems ltd)

Why the hell would someone start a Healthcare business if they are totally into the IT sector? To be honest, the IT sector is beyond my circle of competence, but this company combining healthcare and IT software throws me off.

So just think…what do you really expect from any annual report of a company, clean direct communication, honest reporting, simplicity, focus on the future opportunities… all this seems missing from there reports.

Also they did an ESOP in 2019 at just face value of rs.10 (not good for minority share holders)

at the end i would advice you to stay away from such companies, there are thousands of other opportunities waiting for you in this world of investing