Hi

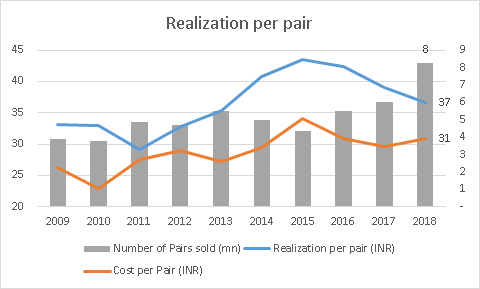

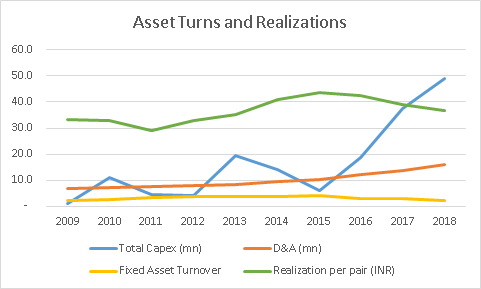

Looked to be an interesting play with domestic branded foray as well getting into into supply of niche football socks. However, their realizations per pair have not matched management commentary -

Company’s major margin drivers are fluctuations in exchange rate, export duties and changes in RM costs, all of which cannot be passed on to the customer, since Virat competes with companies from Bangladesh, China and Turkey, who all have different movements in exchange rates, RM prices and duties (eg. Turkey and Bangladesh have no import duties in EU). Its customers source socks from the lowest cost producers who meet the quality parameters.

Virat Industries is similar to BRKs initial textile business. The benefit of all the capex on technological advances eventually went to the final customer as the commodity nature of the product negated differentiation, while the business swallowed cash as the entire industry continued to upgrade to the newest equipment.

in virat’s case too -

you can read the entire thesis here -

2019 AR would be an interesting read considering the significant changes in company’s fundamentals -

| Year | 2016 | 2017 | 2018 | 2019 | Decline |

|---|---|---|---|---|---|

| Sales | 258 | 257 | 341 | 241 | -29% |

| PAT | 30.4 | 35.2 | 34.7 | 6.5 | -81% |

| Share Price | 95 | 130 | 176 | 59 | -67% |